<p>MedstockPhotos/Shutterstock</p>

Last spring, Democrats in the House of Representatives introduced two bills that would significantly increase the generosity of the premium tax credits currently available through the Affordable Care Act’s (ACA’s) Marketplaces. Neither bill was passed, but now that Democrats control the House, Senate, and the White House, these types of bills are more likely to get serious consideration. One such bill, H.R. 369, has already been introduced.

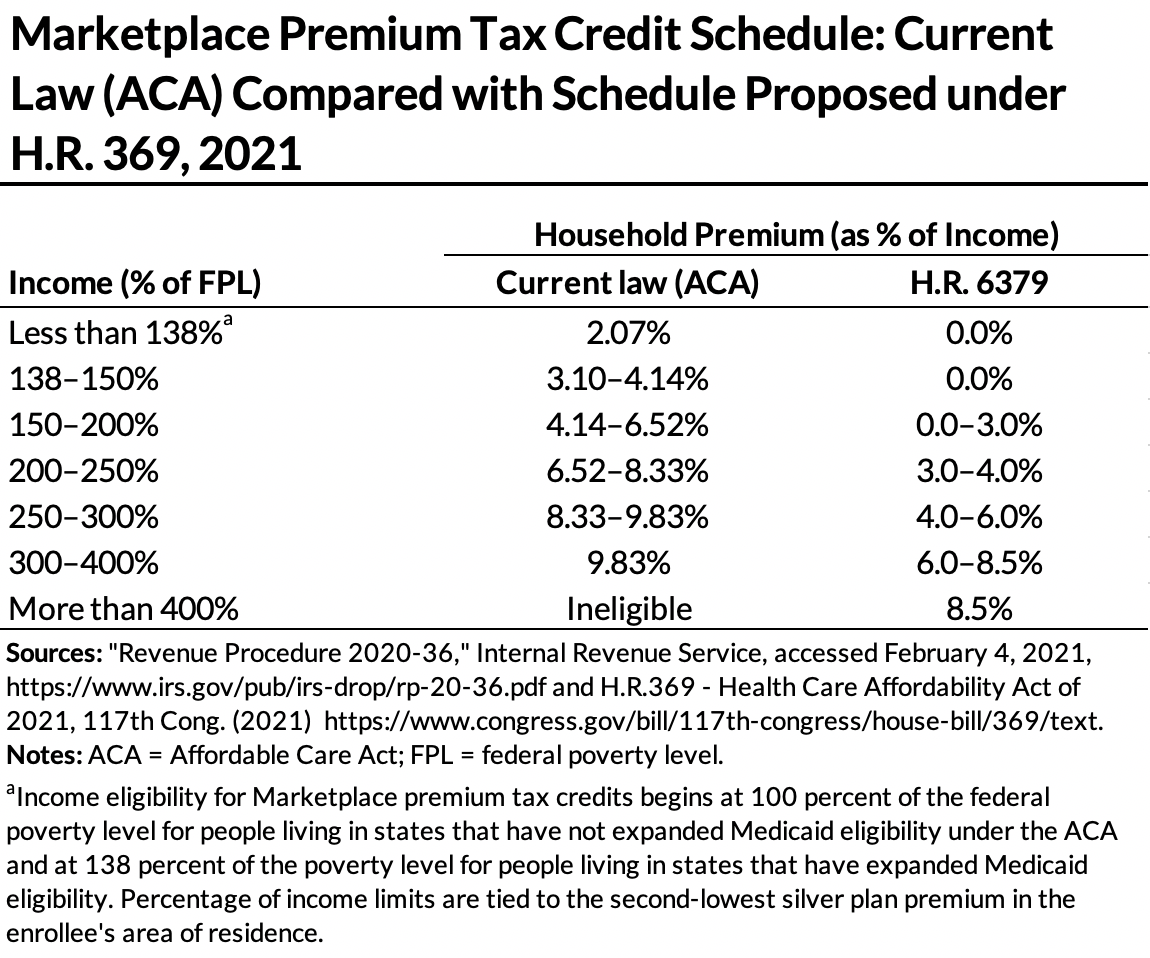

In June 2020, we analyzed the effect of the premium tax credit schedule in the two proposed bills. We found that increasing the generosity of the premium tax credits could increase the number of people with health insurance and would reduce health care–related financial burdens for those already enrolled. Given that the new bill uses the same premium tax credit schedule, we have updated the tables from the earlier analysis here. In the updated tables, we take into account changes in the current law marketplace premium tax credit schedule, in the federal poverty guidelines, and in median Marketplace benchmark premiums.

The ACA’s Marketplace premium subsidies are advanceable tax credits that limit households’ premium contributions to a specified percentage of income, which increases as income increases. Premium tax credits are tied to the “benchmark” premium, or the second-lowest silver-level (70 percent actuarial value) premium where the enrollee lives. People who choose a more expensive plan pay the additional premium cost themselves, and people who choose a less expensive plan pay less than the percentage-of-income cap.

The new bill would lower the percentage-of-income caps for people currently eligible for assistance and would extend assistance to people with an income above 400 percent of the federal poverty level (FPL), who are currently ineligible.

For many, premium savings from the new bill would exceed our 2020 estimates because annual indexing has meant current law subsidies are less generous in 2021. But the median benchmark premium actually decreased this year, which means the typical premium people pay for benchmark coverage if they are ineligible for Marketplace subsidies is lower in 2021 than in 2020.

As such, the new bill would still lead to considerable savings for enrollees with incomes above 400 percent of the federal poverty level but less than what we previously estimated. For example, a 64-year-old single adult with an income of 450 percent of the federal poverty level would save a bit more than $8,000 in premiums this year, down from our estimate of about $8,700 in 2020. And a family of four with two 35-year-old parents and an income of 450 percent of the federal poverty level would save close to $7,100 in 2021, down from the previously estimated $8,000 in 2020.

For other enrollees, our updated findings showed similar savings to our previous estimates:

- Single adult enrollees of all ages with incomes of 150 percent of the FPL would save nearly $800 annually under the proposed schedule.

- A family of four with two 35- year-old parents and an income of 150 percent of the FPL would save more than $1,600 in 2021.

- Older adults currently ineligible for Marketplace subsidies would see the biggest savings from the new schedule, because full (unsubsidized) premiums for older adults are significantly higher than those for younger adults (because of age rating).

- The youngest single adults with incomes at 450 percent of the FPL would not receive a subsidy, even though they would technically be eligible for one because the full benchmark premium in 2021 is less than 8.5 percent of income.

Although these savings would vary each year, the new bill would reduce the premium contributions significantly for most nongroup insurance enrollees, allowing more people to find affordable health insurance and reducing the financial burden health insurance currently poses for others.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.