<p>Doug Armand/Getty Images</p>

If passed, the Take Responsibility for Workers and Families Act (PDF) would provide emergency economic stimulus to address the consequences of the COVID-19 pandemic. One component of the bill would significantly and permanently enhance the generosity of the premium tax credits currently available through the Affordable Care Act’s (ACA’s) Marketplaces.

Our research suggests the ACA’s Marketplace financial assistance has made private nongroup health insurance coverage more affordable for many people with low and modest incomes and helped substantially increase insurance coverage starting in 2014. However, premiums remain a significant barrier to coverage for many: Some people earn incomes too high to qualify for assistance, and yet full premiums would constitute a high percentage of their income. For others, the available subsidies are not enough to make coverage affordable. And still others accept the Marketplace coverage offered, but they do so facing steep financial burdens that affect their abilities to meet other non–health care needs.

Increasing the generosity of premium tax credits can both increase the number of people with insurance coverage (because lower premiums attract more enrollees) and lower the health care–related financial burdens for many people already enrolled in Marketplace coverage.

The ACA’s Marketplace premium subsidies are advanceable tax credits that limit households’ premium contributions to a specified percentage of income, which increases as income increases. Premium tax credits are tied to the premium of the second-lowest silver-level (70 percent actuarial value) premium where the enrollee lives. People who choose a more expensive plan pay the additional premium cost themselves, and people who choose a less expensive plan pay less than the percentage-of-income cap.

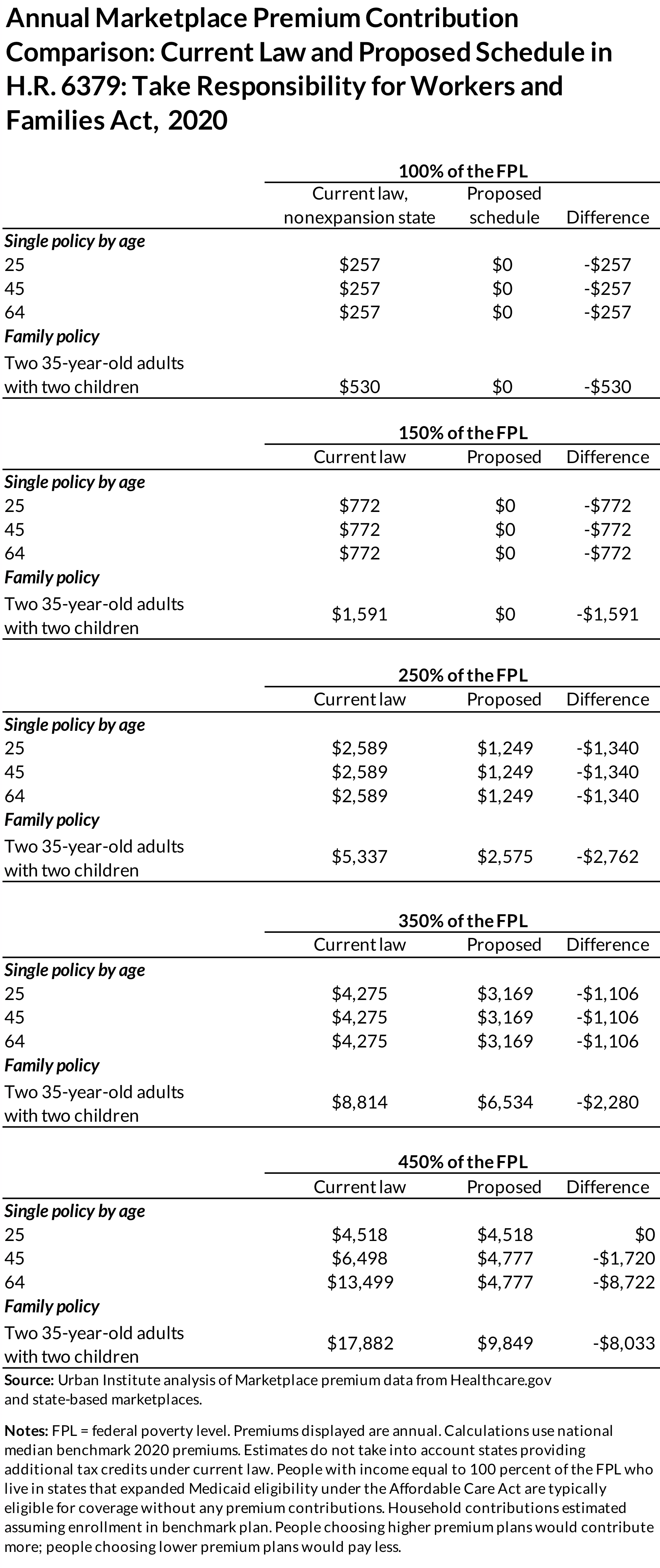

The table below shows the percentage-of-income caps provided today and the lower percentage-of-income limits under the Take Responsibility for Workers and Families Act:

The bill’s percentage-of-income contributions for households are lower than those under current law at every income level (e.g., they start at no contribution for eligible enrollees with incomes up to 150 percent of the federal poverty level, or FPL), but they also extend to people with incomes above 400 percent of FPL (a population currently ineligible for any assistance). As incomes increase beyond 400 percent of FPL, enrollees’ premium tax credits would naturally decrease to zero (as the full premium cost falls below 8.5 percent of income), eliminating the current cliff in assistance whereby one extra dollar of income drops a person’s subsidy to zero. People provided the most assistance under this extension would have incomes between 400 and 600 percent of FPL, be older adults, or have families.

In the table below, we compare the premium contributions required under current law with those required under the schedule proposed in the Take Responsibility for Workers and Families Act. These examples assume enrollees face the national median marketplace benchmark premium in 2020 and are eligible for premium tax credits under both schedules (i.e., they are legal residents of the US, ineligible for coverage through Medicare or Medicaid, and do not have an affordable offer of employer-sponsored health insurance in the family).

Though the bill’s schedule would reduce premium contributions the most for people with incomes above 400 percent of FPL, older adults, and families, it would also help younger adults and people with lower incomes accrue significant savings:

- Single adult enrollees of all ages with incomes at 150 percent of the FPL would save nearly $800 annually under the proposed schedule.

- An example family of four with two 35- year-old parents and income at 150 percent of FPL would save about $1,600 per year.

- Older adults currently ineligible for marketplace subsidies would see the biggest savings from the new schedule, because full (unsubsidized) premiums for older adults are significantly higher than those for younger adults (because of age rating). For example, a 64-year-old single adult with income of 450 percent of FPL would save more than $8,700 in premiums each year.

- The youngest single adults with incomes at 450 percent of FPL would not receive a subsidy, even though they would technically be eligible for one, because the full premium is less than 8.5 percent of their income.

- The example family of four at 450 percent of FPL would save more than $8,000 per year.

Our analysis shows the changes to the Marketplace premium tax credit schedule proposed in the Take Responsibility for Workers and Families Act would lower premiums significantly for individuals and families across a broad swath of incomes and who are enrolled in nongroup health insurance or would choose to be in the future. The schedule would reduce health care–related financial burdens for millions already enrolled in nongroup coverage, freeing up funds for other needs. And, if adopted, the approach should reduce the number of uninsured people, because more people would find postsubsidy coverage affordable.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.