<p>The Medrano family sits outside their RV on October 7, 2020, in Phoenix, Arizona. They had narrowly avoided eviction from the RV park earlier in the day. Even for families who have remained healthy from the coronavirus, the indirect effects of the pandemic have been especially tough on America's poor, who often deal with simultaneous crises, even in normal times. In the Medrano family's case, inconsistent work, a string of tragedies, and family separation have combined to push them to the brink of homelessness. For families like the Medranos, new federal pandemic assistance, yet to be authorized by Congress, cannot come soon enough. (Photo by John Moore/Getty Images)</p>

Recent data show 5.3 million renter households have lost a job since the pandemic’s onset, and many more have experienced cuts to hours, pay, or to gig and contracting work. These losses have hit Black and Latinx families and families with low incomes especially hard because of systemic inequities in the labor market.

Despite the sobering statistics, the little data that exist on housing payments show a relatively stable picture. The US Census Bureau’s most recent Household Pulse Survey data indicate about 80 percent of renters paid rent in July. But these data may mask the painful reality for many families, especially families with low incomes, who are dipping into savings, using credit cards, and skipping utility bills to ensure their rent is paid.

“They are paying with their futures,” Emily Benfer, chair of the American Bar Association’s eviction work, told the Washington Post in early September. “They are using credit cards and taking on financial risk.… They know without it they cannot keep their families safe.”

The Centers for Disease Control and Prevention’s (CDC’s) nationwide eviction moratorium (PDF) provides temporary protections until the end of the year, but without rent relief, families are at risk of eviction as soon as the moratorium lifts. Renters unable to continue paying monthly rent will accrue a mounting, potentially insurmountable, debt. The picture for many homeowners is not much better.

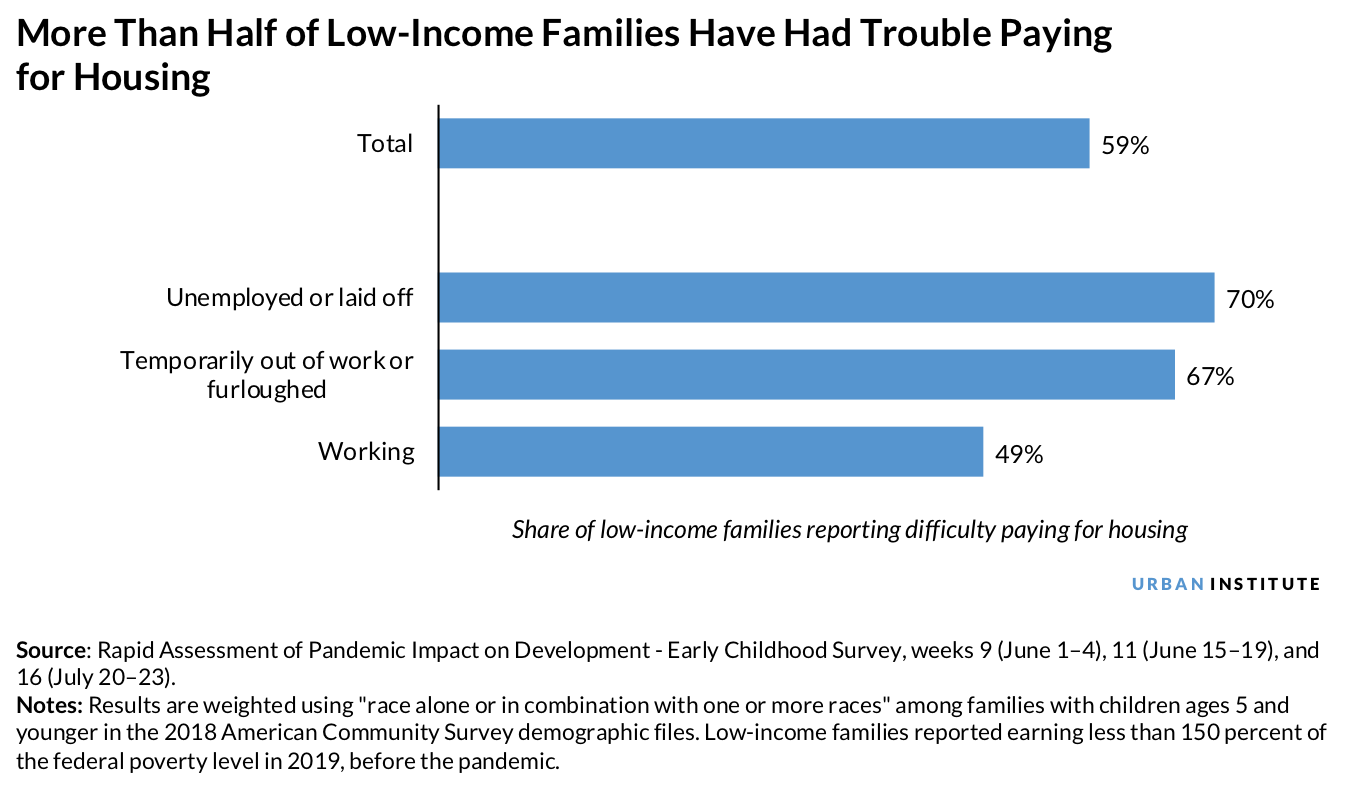

New data show nearly 60 percent of low-income families with young children who report challenges paying for basic needs had trouble paying for housing in June and July. Seventy percent of unemployed or laid-off families report the same. Even for working low-income families, nearly half report challenges paying for housing.

These findings come from a new survey from the University of Oregon’s Center for Translational Neuroscience. The Rapid Assessment of Pandemic Impact on Development (RAPID) - Early Childhood Survey is designed to gather essential information regarding the needs, health promoting behaviors, and well-being of families with children ages 5 and younger during the COVID-19 outbreak in the United States. To help put the RAPID data in context for policy, Urban Institute researchers Kathryn Reynolds and Aaron Shroyer shared expert insights and resources documenting the housing needs of low-income families and policy solutions that could help meet them.

Housing is a pressing material concern for low-income families

The expiration of the supplemental $600 in weekly unemployment insurance authorized by the Coronavirus Aid, Relief, and Economic Security Act at the end of the July left families financially vulnerable. Most states have offered an additional six weeks of $300 in supplemental unemployment insurance, but this relief has started to expire, leaving many families with greater difficulty paying their housing costs. Before the CDC issued its nationwide eviction moratorium on September 2, eviction filings flooded courts, and estimates predicted between 28 million and 40 million people could face eviction.

Although the new moratorium put evictions back on hold, that’s only half the battle. One study estimates that the total amount of back rent owed could reach $40 billion by the time the CDC’s moratorium expires.

But rent is not the only housing-related expense owed. RAPID data show about 70 percent of low-income families struggling to pay for basic needs found it hard to pay utilities, the highest rate of any basic need. Without the risk of eviction, some families could decide to hold off paying rent or utilities, prioritizing other essentials. Others may do their best to cover housing payments, leading to food insecurity, insufficient health insurance coverage, and strains in affording other basic needs. In either case, utility debts are piling up, with electric and gas debts estimated to reach $24.3 billion by the year’s end. Until seasonal protections kick in, families in most states are not covered by moratoriums on utility disconnections.

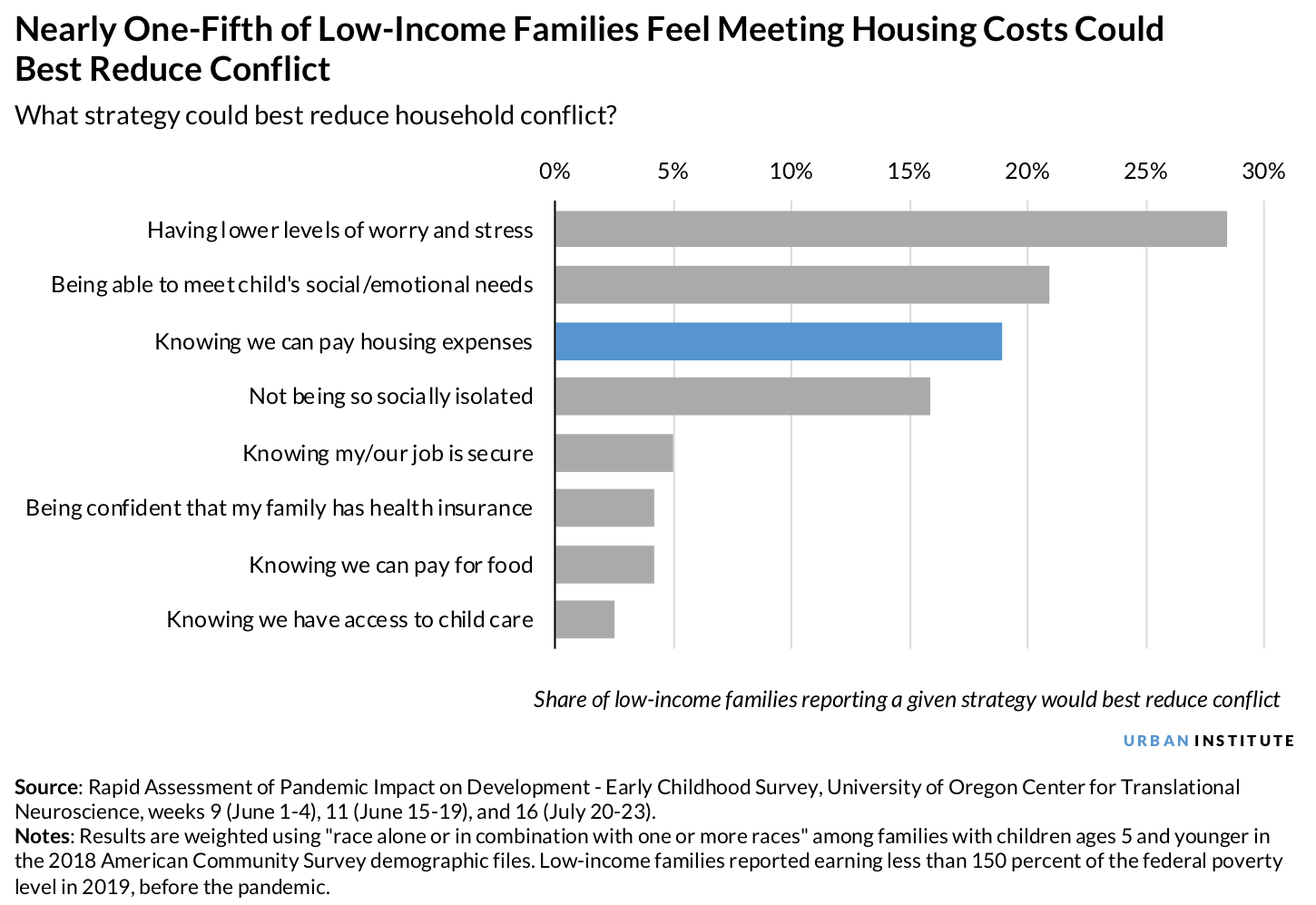

These large housing and housing-related debts represent a major source of stress for low-income families. Nearly 20 percent of families reported that knowing they could pay for housing expenses would reduce household conflict, making it the most cited material strategy. Only lower levels of stress and being able to meet their child’s social and emotional needs were cited more frequently than housing expenses.

Without housing support, family conflict could lead to other hardships and traumas. Research shows that when long-term housing assistance helps families sustain stable housing, families’ lives improve. In the same study, housing vouchers were shown to reduce drug and alcohol dependence and halve intimate partner violence in both the long and short term. Housing policy is family policy.

States and localities cannot meet full housing need, so federal relief is necessary

In early October, Urban Institute researchers estimated that returning renter households with job losses to their prepandemic rent burden would require between $1.1 and $2.1 billion in monthly assistance. States and localities can issue moratoriums on evictions and utility payments, but with budgets retracting at an unprecedented pace, housing assistance must come from the federal government.

Resuming additional federal unemployment insurance could help but would not reduce the full rent burden in households that have experienced job loss. This strategy would also leave out the lowest-income adults and the nearly 50 percent of low-income working families who are struggling with housing payments.

For both renters and landlords, federal rental relief is necessary, whether through expanding Section 8 vouchers, Emergency Solutions Grants, or other programs. Not only would this relief help counteract the looming housing crisis, but, as the RAPID-EC data show, it could also help stem intimate partner violence, reduce climbing utility debts and utility shutoffs, and prevent widening racial and economic disparities.

With COVID-19 cases increasing nationwide and all 50 states’ GDPs having dropped year-over-year, it is unlikely that low-income families will recover any stability before the CDC’s eviction moratorium ends. The longer the federal government waits to provide rental assistance at scale, the larger these families’ debts will grow, and the more limited their resources will become. As Benfer told the Washington Post, these families are already paying with their futures. Federal intervention can help them avoid paying with their children’s futures too.

Philip Fisher, Philip H. Knight chair and professor of psychology at the University of Oregon, contributed to this post.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.