<p>Tequandra Rozier spends time looking at a family video after being laid off from her job at Starbucks on March 26, 2020 in Miami, Florida. Rozier said that she has applied for unemployment benefits as she joins roughly 3.3 million Americans nationwide who are looking for unemployment benefits as restaurants, hotels, universities, stores, and more shut down in an effort to slow the spread of COVID-19. (Photo by Joe Raedle/Getty Images)</p>

America’s 44 million renter households, particularly the 21 million who devote at least 30 percent of their income to rent, need immediate relief for rent payments amid the COVID-19 crisis. They have lower incomes and savings, lower access to credit, less job stability, and historically greater difficulty in paying for their housing costs, which makes them more vulnerable than homeowners during this unstable time.

To help policymakers understand how their interventions can best support renters most affected by the coronavirus, we examined data on renters’ financial capabilities before the virus and on their occupation and industry groups to understand the likely impact of the virus. We find that economic volatility affects young renters more than older renters, and Black and Hispanic renters will likely face more challenges than white and Asian renters.

Following the Great Recession, the wealth gap and the homeownership gap by age and race or ethnicity widened considerably. Policymakers designing interventions to address the coronavirus need to ensure vulnerable young renters and communities of color are not further left behind.

A look at the financial stability of American renters

Renters, in general, have lower incomes than homeowners, and low-income renters often struggle to pay their monthly housing costs. But income alone does not tell the whole story. Some low-income older renters, for example, have significant assets or receive subsidized rental housing assistance and aren’t as financially vulnerable. At the same time, some renters who struggle to pay their rent have high incomes and simply live beyond their means. Income and ability to pay are both important considerations.

For this blog post, we reviewed the 2019 US Financial Health Pulse Data, which show spending, savings, and debt to give a more complete picture of financial stability among different groups. We also use 2018 American Community Survey data for information about occupation and industry groups to capture employment stability.

Young adults are disproportionately renters and face greater difficulty paying rent

Young adults rent in higher proportion than older adults. In 2018, 66 percent of households headed by someone age 35 or younger were renters, compared with 22 percent of households headed by someone older than 65. Since 2005, the share of young renters has increased by more than 10 percentage points, as many young households have found it harder to access homeownership after the 2007 housing market crisis.

Young households are also more likely to face challenges paying their rent. In 2019, one-third of young renters had trouble paying rent, compared with 8.7 percent of renters ages 65 and older. This is partly because young renters have fewer liquid assets (including cash and savings). In 2019, renters ages 35 and younger had income and employment rates similar to renters ages 35 to 45 but had half the the median liquid assets ($5,200 versus $10,200).

COVID-19 will make this situation worse for young renters because young renter household heads are disproportionately more likely to work in the four industries expected to be hardest hit during the pandemic: food and accommodation, entertainment, retail, and transportation (PDF). In 2018, about 30 percent of young renter household heads (or 4.1 million) worked in these four sectors, compared with about 25 percent of renter household heads older than 35. Young renters face a greater risk of losing their job during the pandemic, and their earnings will be jeopardized as restaurants, bars, and other retail industries close.

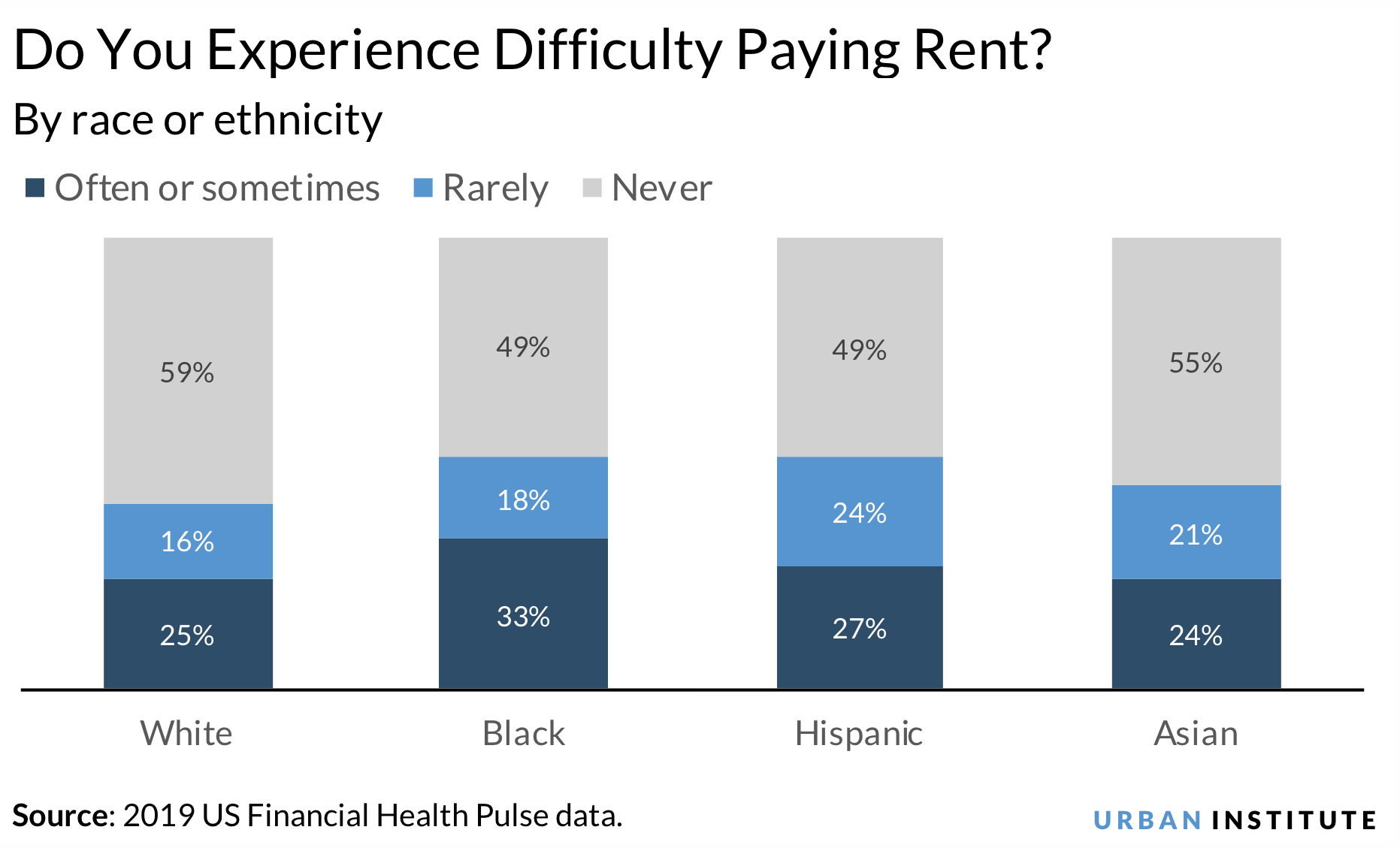

People of color are disproportionately renters and have more difficulty paying rent

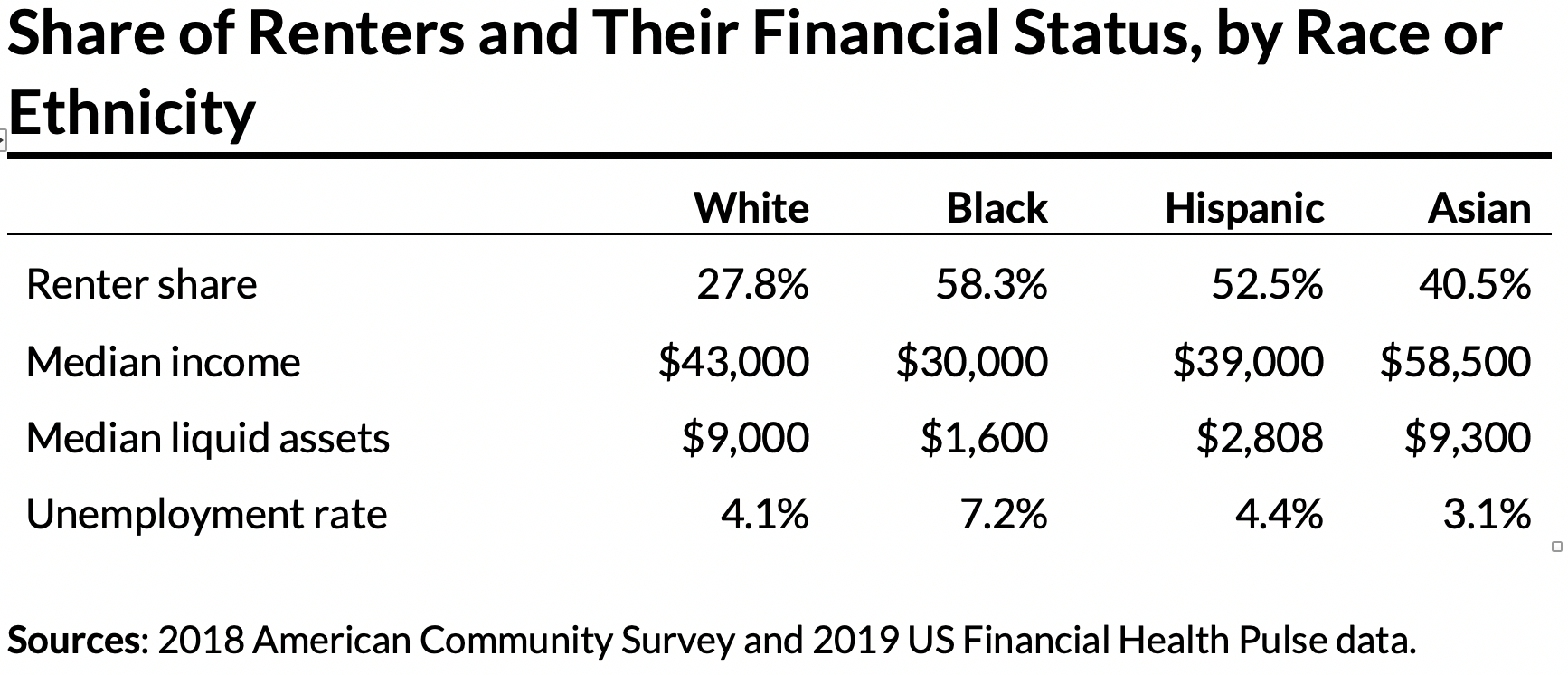

People of color are more likely to be renters than non-Hispanic white households. In 2018, 58.3 percent of Black households, 52.5 percent of Hispanic households, 40.5 percent of Asian households, and 27.8 percent of white households were renters. In addition, Black households were hit harder than other groups by the 2007 housing market crisis and have experienced the greatest drop in homeownership since then.

A larger share of Black and Hispanic households reported difficulty paying rent in 2019 than white households. One-third of Black households often or sometimes had trouble paying rent, which was 9 percentage points higher than for white households. The share of Hispanic households that reported the same difficulty was only 2 percentage points higher than for white households, but a smaller share reported never having trouble paying rent.

Black renter households are already the most vulnerable to economic instability. They have the lowest median income, the lowest median liquid assets, and the highest unemployment rate among all racial and ethnic groups. Hispanic households are also significantly more vulnerable than white or Asian households.

Except for Asian renters, the share of renter household heads working in the four industries most vulnerable to the COVID-19 shock is similar by race or ethnicity. Nearly 30 percent of white, Black, and Hispanic renter household heads work in the four sectors, but only 22 percent of Asian household heads do. A higher share of Black and Hispanic renters, however, are service workers, even within the same industry. In 2018, 27 percent of Black and 25 percent of Hispanic renter household heads were in service occupations, compared with 19 percent of white and 11 percent of Asian renter household heads. Black and Hispanic renters face a higher risk of losing their jobs as COVID-19 disrupts the economy.

Policy responses to COVID-19 must consider these hardest-hit groups

Renters are more vulnerable to the economic shocks of COVID-19 than homeowners, young renters are more vulnerable than older renters, and Black and Hispanic renters are more vulnerable than white and Asian renters. These groups of renters were already disproportionately hurt by the 2007 housing market crisis and were slower to recover from the aftermath. COVID-19 is likely to disproportionately weaken their financial health again and further widen inequalities absent appropriate and effective policies and programs.

Policymakers need to consider the impact on these hard-hit groups when designing and implementing new policies to respond to COVID-19. Many renters have received temporary eviction relief through the Coronavirus Aid, Relief, and Economic Security Act, but most have not. Moreover, eviction moratoriums do not pay the rent. Rental assistance could help many young renters and renters of color, who are likely to face great difficulty making their next housing payment.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.