Social Security cuts, shrinking employer-sponsored pensions, low savings rates, and longer life spans have raised fears of a looming retirement crisis. But other trends point to better retirement outcomes, such as women’s increased employment and earnings, longer working lives, and economic growth that raises wages.

How will these conflicting trends play out? How will the next generations of older Americans fare in retirement relative to those who came before? And what will happen to retirees if Congress cuts Social Security benefits to address the program’s long-term financing gap?

These nine charts, based on projections from the Urban Institute’s Dynamic Simulation of Income Model 4 (DYNASIM4), provide some answers. Using the best and most recent data available, DYNASIM4 helps sort out how the profound social, economic, and demographic shifts that are transforming retirement will shape older adults’ future financial security.

1. Retirement incomes will continue to rise

Despite widespread concern that workers are not saving enough for retirement, we project that retirement incomes will continue to increase over the next four decades as long as policymakers do not cut Social Security benefits.

Our data are broken down into 10-year birth cohorts that roughly translate into generations. Baby boomers fall into two categories: early boomers and late boomers. Our youngest cohort captures late Gen Xers and early millennials, a group that some consider a “microgeneration” known as Xennials. We use that term here to describe people born from 1976 to 1985.

Our projections show that median per capita after-tax family income at age 70 will be 17 percent higher for people born from 1966 to 1975 (Gen Xers) than for people born from 1936 to 1945 (pre-boomers), in inflation-adjusted dollars. Median retirement income for Xennials will be 24 percent higher than the median for pre-boomers.

2. Women’s increased earnings will power retirement income growth

Retirement incomes depend on how much people worked and earned when they were younger. Higher lifetime earnings mean more Social Security and—for those with coverage—larger pensions and retirement account balances. They also mean the ability to save more outside of retirement accounts.

As women work more and earn more per hour, their lifetime earnings are increasing rapidly. We project that, compared with pre-boomer women, median lifetime earnings will be 88 percent higher for Gen X women and 129 percent higher for Xennial women in inflation-adjusted dollars. These gains will raise retirement incomes for women as well as for married men.

Men’s lifetime earnings, by contrast, are not keeping pace with inflation. Projected median lifetime earnings are 3 percent lower, in inflation-adjusted dollars, for Xennial men than for pre-boomer men.

Despite women’s gains, the gender gap in earnings persists. We project that Xennial median lifetime earnings will be 40 percent higher for men than for women.

3. Despite growth in retirement incomes, retirement resources will fall short for more Gen Xers and Xennials

A common goal of retirement planning is to maintain preretirement living standards. Having enough income to replace 75 percent of preretirement earnings is often used as an adequacy rule of thumb because spending typically declines in retirement. Retirees do not pay payroll taxes or save for retirement, and their children have usually already left home.

Only about 26 percent of late, early, and pre-boomers will be unable to replace 75 percent of their preretirement earnings at age 70 according to our projections. However, that share jumps to 30 percent for Gen Xers and 32 percent for Xennials.

Nonetheless, we project that almost 70 percent of Gen Xers and Xennials will have adequate resources to maintain their living standards in retirement as long as policymakers do not cut Social Security benefits.

4. Social Security’s financing problems threaten retirement security

With Social Security payments now exceeding payroll tax revenues, the system’s trustees project that the Social Security trust funds will run out in 2035 unless federal policymakers raise revenues or cut benefits to close the financing gap. If policymakers do nothing, the system will be able to pay only about 75 percent of scheduled monthly benefits.

If benefits are cut across the board beginning in 2035, 38 percent of Gen Xers and 40 percent of Xennials will be unable to replace at least 75 percent of their preretirement earnings at age 70, leaving them worse off than when they were working. Pre-boomers and early boomers would feel these cuts at older ages because they will turn 70 before the Social Security trust funds are projected to run out.

Even if policymakers address Social Security’s financial problems, benefit cuts included in the solvency package could leave some future retirees with inadequate retirement resources.

5. Social Security cuts would disproportionately harm low-income retirees

Social Security is the most important component of income for families with low and moderate incomes. Among 70-year-old pre-boomer beneficiaries, it accounts for 86 percent of income for those in the bottom fifth of the income distribution and 72 percent for those in the next fifth. Consequently, future Social Security cuts could hit low-income retirees especially hard.

Social Security is crucial for retirees with low incomes because they generally lack other types of retirement savings. We project that fewer than 33 percent of Xennials in the bottom fifth of the income distribution will have an employer-sponsored pension or retirement account when they retire, compared with about 70 percent of Xennials overall. Social Security replaces a larger share of lifetime earnings for retirees with limited lifetime earnings than for those who earned more. Nonetheless, Social Security is often insufficient to lift out of poverty many retirees who worked in low-wage jobs or stopped working because of poor health or caretaking responsibilities.

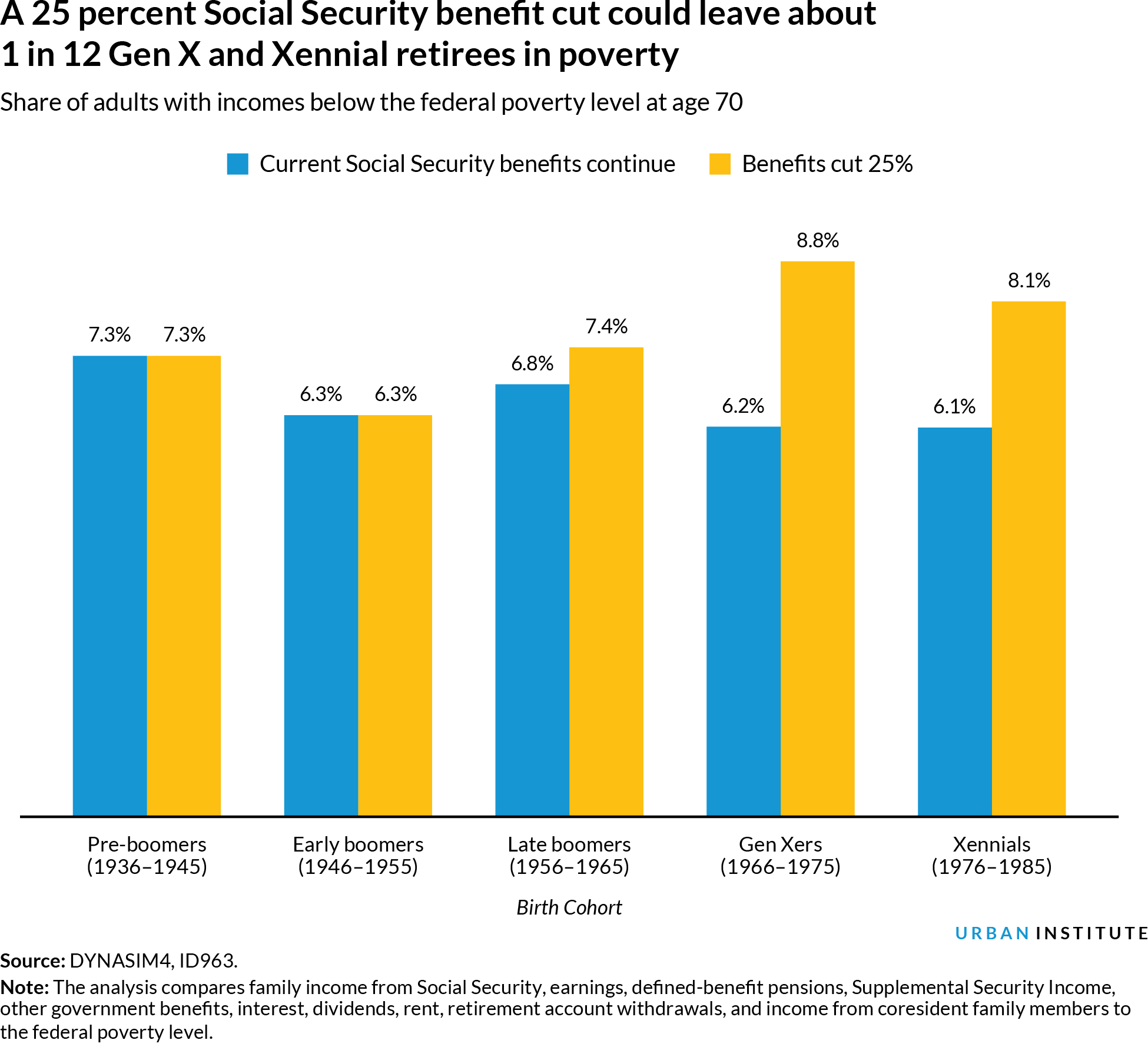

6. Old-age poverty rates could rise if policymakers ignore Social Security’s financial problems

If policymakers resolve Social Security’s long-term financing problems by raising system revenues and maintaining existing benefit rules, old-age poverty rates are projected to fall slowly over time. We project that the share of 70-year-olds with family income below the federal poverty level will fall from 7.3 percent for pre-boomers to 6.1 percent for the Xennials as earnings growth raises average Social Security benefit payments.

However, if policymakers fail to act and Social Security benefits are cut about 25 percent across the board beginning in 2035, old-age poverty rates will rise significantly. Such a benefit cut would increase the number of retirees living in poverty about 42 percent for Gen Xers and 33 percent for Xennials.

7. Racial and ethnic disparities in retirement income will persist

Retirement security is not shared equally across racial and ethnic groups. Compared with pre-boomer non-Hispanic white people, median per capita after-tax income at age 70 was 32 percent less for pre-boomer black people and 58 percent less for pre-boomer Hispanic people.

Although our projections show that these disparities will narrow somewhat, they will likely remain substantial for decades. We project that among 70-year-old Xennials, median after-tax income will be 26 percent lower for black people than for white people and 49 percent lower for Hispanic people.

Racial and ethnic disparities in retirement persist because people of color generally earn less than white people, even though Social Security’s progressive formula redistributes benefits toward retirees with low lifetime earnings. Black and Hispanic people are also less likely than white people to have a retirement plan at work or to inherit wealth from earlier generations.

8. The gender gap in Social Security benefits will narrow

As women’s employment and earnings grow, their Social Security benefits will increase. If policymakers do not cut Social Security benefits, we project that median Social Security benefits at age 70 will be 68 percent higher for Xennial women than for pre-boomer women (after correcting for inflation). Men’s Social Security benefits will grow only 25 percent. The gender gap in Social Security benefits will fall from 37 percent for pre-boomers to 15 percent for Xennials.

Social Security bases retirement benefits on beneficiaries’ lifetime earnings. However, if doing so would make them better off, retirees can instead receive a payment equal to 50 percent of their spouse’s benefit (and 100 percent of their spouse’s benefit after his or her death). We project that as women’s lifetime earnings grow over time, the share of women collecting a Social Security benefit at age 70 at least partly based on a spouse’s earnings will fall to 23 percent for Xennials, down from 47 percent for pre-boomers.

9. Gen Xers and Xennials will pay more taxes in retirement

At age 70, Gen Xers and Xennials are projected to allot 18 percent of their income to taxes, compared with 14 percent for pre-boomers. These payments include federal and state income taxes, Medicare surtaxes, and payroll taxes for those still working. Effective tax rates will increase over time because the income thresholds for taxing Social Security and Medicare surtaxes are not indexed for inflation and the Tax Cuts and Jobs Act of 2017 slowed the indexing of income tax thresholds, pushing tax payers into higher income tax brackets.

Promising policies to promote retirement security

These projections can help policymakers identify and tackle the challenges ahead. Reforming Social Security and other policies could help ensure retirement security for all generations.

- Many retirees will continue to rely on Social Security for the bulk of their incomes. This data tool explores several policy scenarios that could help close Social Security’s long-term financing gap before trust funds are depleted within the next 15 years. Users can examine the distributional impact of pension and Social Security reforms on future retirement income.

- A significant share of baby boomers, Gen Xers, and Xennials will reach old age with little retirement income. Policy remedies such as modernizing the Supplemental Security Income program and boosting minimum Social Security benefits could help the most vulnerable retirees for little cost.

- Working longer improves retirees’ long-term security while boosting worker productivity, generating additional payroll and income tax, and reducing Social Security’s deficit. Policymakers and employers need to recognize the importance of jobs for older adults, promote retraining and flexible work schedules that can accommodate their needs, and eliminate work disincentives at older ages.

- Converting our current regressive and inefficient tax breaks for retirement savings into more targeted incentives could help boost savings for low-income groups. Replacing tax deductions, which disproportionately benefit high-income families, with tax credits would reach those most in need and help reduce the retirement preparedness gap.

- Expanding options to annuitize retirement accounts and savings at retirement could raise retirement incomes and provide more older adults with the security of a guaranteed income stream until death, a growing concern as employer pensions fade away.

ABOUT THE DATA

The Urban Institute’s DYNASIM projects the size and characteristics—such as financial, health, and disability status—of the US population for the next 75 years. Using the best and most recent data available, it helps sort out how the profound social, economic, and demographic shifts that are transforming retirement will likely affect older adults, taxpayers, business, and government. DYNASIM addresses some of the most pressing policy questions affecting our aging nation and evaluates the adequacy and fairness of our retirement system.

PROJECT CREDITS

This feature was funded by the Alfred P. Sloan Foundation. We are grateful to them and to all our funders, who make it possible for Urban to advance its mission.

RESEARCH Damir Cosic, Richard W. Johnson, Karen E. Smith, and Aaron R. Williams

DEVELOPMENT Aaron Williams and Alice Feng

EDITING Serena Lei, Michael Marazzi, and Casey Simmons