Stereotypes abound when it comes to explaining how men and women use money differently, and more than one comic has found material for a stand-up routine in those perceptions. But are differences in how men and women view and manage their finances real or imagined?

Our new brief, coauthored with Emma Kalish and Signe-Mary McKernan, uses data from the recently released FINRA Investor Education Foundation’s 2012 National Financial Capability Survey to examine differences between men and women in financial knowledge, financial behavior, and financial well-being, isolating the influence of gender by controlling for other observable characteristics.

Are women less financially knowledgeable than men?

Researchers administered a five-question financial literacy quiz to a representative sample of American adults. According to the results, the answer is yes. (See how you do by taking the quiz yourself.)

- Financial knowledge, while generally low, is worse among women. Women answered fewer questions correctly than men—on average, 3.1 correct answers for women versus 3.6 for men.

- Unmarried women are no less confident about their financial skills than unmarried men. But married women rate their financial skills lower than married men do, which may result from men and women adopting different financial tasks in the family.

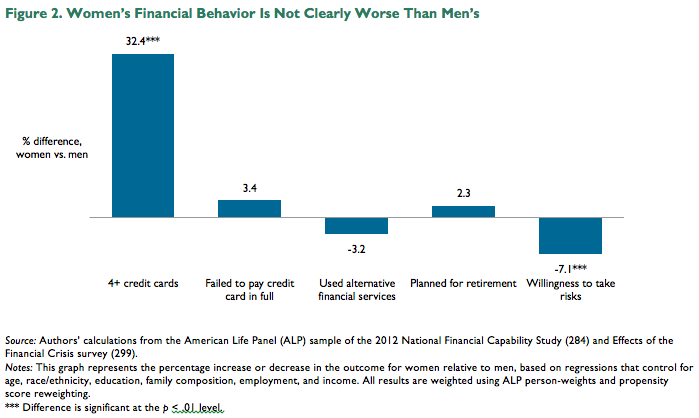

Do women and men have different financial behaviors?

In some cases, yes; in others, no.

- Women are 32 percent more likely than men to have four or more credit cards (see figure below)—true for both married and unmarried women. Greater holding of store-branded credit cards may help explain this difference.

- Looking at all women, we find they are equally likely as men to pay their credit cards in full. But this isn’t the case for unmarried women with children, who are less likely to pay off their credit card bills each month.

- We see no differences in the rate at which women and men use alternative financial services, like pawn shops and payday lenders, or plan for retirement.

- Women—whether married or unmarried, whether mothers or not—are more financially cautious than men. Across the board, we find that women are less willing than men to take financial risks.

Does financial well-being differ by gender?

Unmarried mothers struggle to make ends meet, but there are no major differences in outcomes for married men and women, or unmarried men and women without kids.

- Women report more difficulty covering their expenses than men, a difference driven by unmarried mothers. We find no differences between married men and women or unmarried childless men and women.

- Regardless of marital status, women are just as satisfied—or dissatisfied—as men with their personal financial condition (assets, debts, and savings).

- What about the likelihood of having emergency and retirement savings? Men and women don’t differ.

What do these findings mean? Most financial surveys capture household-level data, blurring gender differences. Individual-level data afford a valuable look at gender differences in financial knowledge, behavior, and well-being. This analysis suggests that women are less financially knowledgeable than men, but that doesn’t necessarily translate to worse financial behaviors or lower financial well-being than men. Unmarried mothers, however, emerge as a vulnerable group.

This post's graphic has been updated with a correction.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.