More than 1.2 million homeowners that defaulted during the recession are receiving a five-year reduction in mortgage interest rates through the HAMP (Home Affordable Modification Program) introduced in 2009. But when the first set of modifications begins to experience interest rate increases later this year, will increased payments put recipients at risk of a second default?

How the modifications work

HAMP modifications provide borrowers with payments tied to a 31 percent debt-to-income ratio through a reduced interest rate as low as 2 percent. But after five years, the rate increases by one percent each year until it reaches the prevailing interest rate in effect at the time of the modification. When the interest rate resets, a borrower’s monthly payment increases—as does their risk of re-default.

Given some improvement in borrower incomes and more in home prices, most borrowers will be able to handle the first two payment jumps. But the third increase could be a problem.

As discussed in our new commentary, in 2016, the first small 2009 cohort of borrowers experiencing modifications will experience its third payment increase, at which time we think the effect of HAMP resets will first manifest itself. But in 2017, a large 2010 cohort will experience its third payment increase, raising the risk even more. These third resets will increase interest rates from 4 to 5 percent and monthly payments by an average of 42 percent from the initial post modification level. The problem will ease considerably in 2018 because the large 2010 cohort will have mostly reset. And by 2019, the reset issue will be quite small.

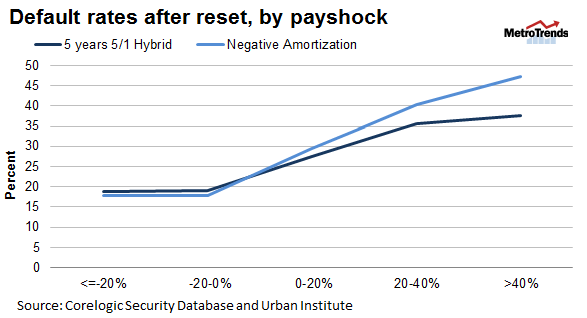

How much will defaults increase?

To date, two mid-2000s products—5-year 5/1 hybrid and negative amortization (Negam) loans—provide the best examples of significant payment shock’s effects.

These loans saw a 14 to 15 percent increase in default risk, but these numbers should be seen as upper bounds for the impact of HAMP resets. HAMP resets are occurring in a healthier housing market and these HAMP characteristics mean re-default risk is likely even lower because:

- HAMP loans reset gradually rather than all at once,

- House prices have appreciated rather than severely depreciated in the period since HAMP modifications,

- HAMP resets are totally predictable rather than tied to unpredictable current interest rates, and

- HAMP loans are national rather than concentrated in the sand states (AZ, CA, FL, and NV) that were hurt most during the housing crisis.

A realistic look at HAMP reset risk

A more reasonable assessment of the defaults that HAMP resets will generate might be a 10 percent additional default rate—likely further mitigated by additional modification actions. With proprietary and other modifications still available, a possible 40 to 50 percent of these borrowers will roll into an alternative modification, lowering the additional defaults at reset to between 5 and 6 percent.

For many borrowers, particularly those who needed the most help and received the steepest discount in interest rates, HAMP resets will be a challenge. But the reset issue is very manageable.

We are likely years away from a significant impact—an impact that will likely be lessened by economic improvements in the interim.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.