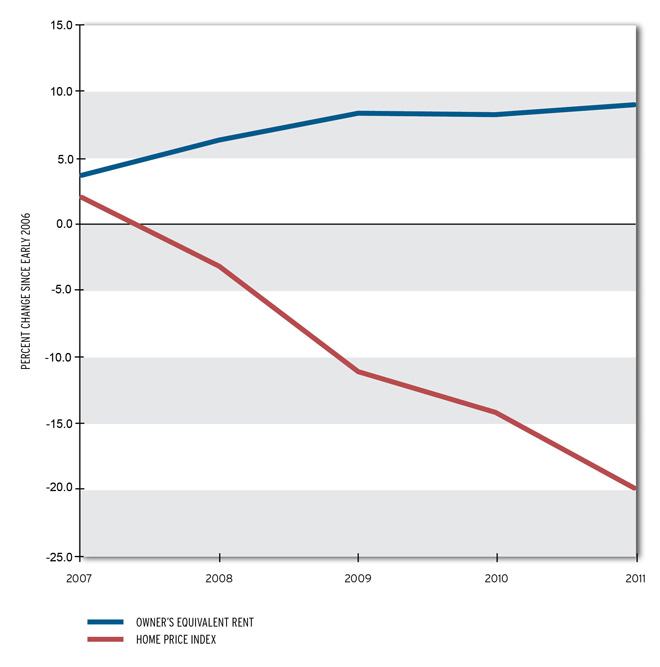

Home prices in US metros are falling to new lows, threatening the economic recovery but –here’s the silver lining—also making homes increasingly affordable. The share of homes affordable for a family earning the median income has doubled since 2006—from 40 percent to 80 percent today. Normally, when prices fall, the Consumer Price Index (CPI), the nation’s main cost-of-living indicator, declines too. Yet, the Bureau of Labor Statistics (BLS) reports, housing costs for owner-occupied dwellings have risen by 9 percent since 2006 even though home prices dropped by 20 percent. What’s happening here? Is the CPI exaggerating the actual rise in living costs? And are more than housing costs affected by this apparent fluke?

Change Since 2006 in Owner's Equivalent Rent Versus Average Home Price

First, housing. Since homes are durable goods, they have two prices: the price a home can command if it’s sold on the market and the price of the services provided by the home (comparable to rent). In a way, homeowners are both tenant and landlord. As tenants, they pay the monthly costs for the housing services they consume. As landlords, they receive the rent they pay as consumers. That said, homeowners don’t set the rent they charge themselves so BLS tries to estimate how much rent the dwelling would command on the open market. With the focus on the costs homeowners pay as consumers instead of the property’s market value, capital gains and losses don’t get conflated into living costs.

If this sounds relatively simple, here’s the hitch: the data government needs on the rents homeowners could get for their property is hard to find. In some cases, there just isn’t any because there aren’t any equivalent rentals. Further complicating this statistical stretch, many homes probably couldn’t command rents equal to similar rental units because they are like the many vacant places kept off the market and thus buoying up for-sale homes a bit. In short, then, current rents may overstate actual housing costs for owner-occupied homes.

Equivalent rents don’t tell the whole story either. Even if the BLS accurately estimates owners’ equivalent rent, the CPI doesn’t reflect the costs homeowners see. Most people buying homes with fixed rate mortgages lock in their monthly housing costs (or rent equivalent) for years. When interest rates fall, many (millions in recent years) refinance to cut their housing costs. So changes in housing costs for recent buyers and refinancers reflect changes in home prices and interest rates—not rents.

Now a word on the official cost of living more generally. Social Security and Food Stamps tie benefits to the CPI. Even federal payments on inflation-linked bonds go up and down with the official cost of living. And if the CPI overstates upticks in the cost of living, then real wages are rising faster than the government reports. Some math in the service of this point: since owners’ housing costs make up nearly 25 percent of total living costs, a 29- percent in the CPI’s housing component (from a 20 percent decline to a 9 percent increase) could overstate inflation by over 7 percent—more than two-thirds of overall CPI growth. Factoring in inflation changes measures of real income growth, from near stagnancy using the standard CPI to a moderate 2- percent growth between early 2006 and early 2011.

Like many economics statistics, the CPI’s measured rise in housing costs looks odd since it diverges so much from what we expect-- sharp declines in home prices and interest rates driving down total housing costs. And what’s at stake in interpreting the numbers is not just theoretical. The figures raise important questions about why today’s rents and home prices are moving in opposite directions. The short answer is that more people lack access to mortgage credit and many expect further declines in home prices. (I’ll give you more detail in a blog coming soon.)

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.