<p>(MoMo Productions/Getty Images)<br />

</p>

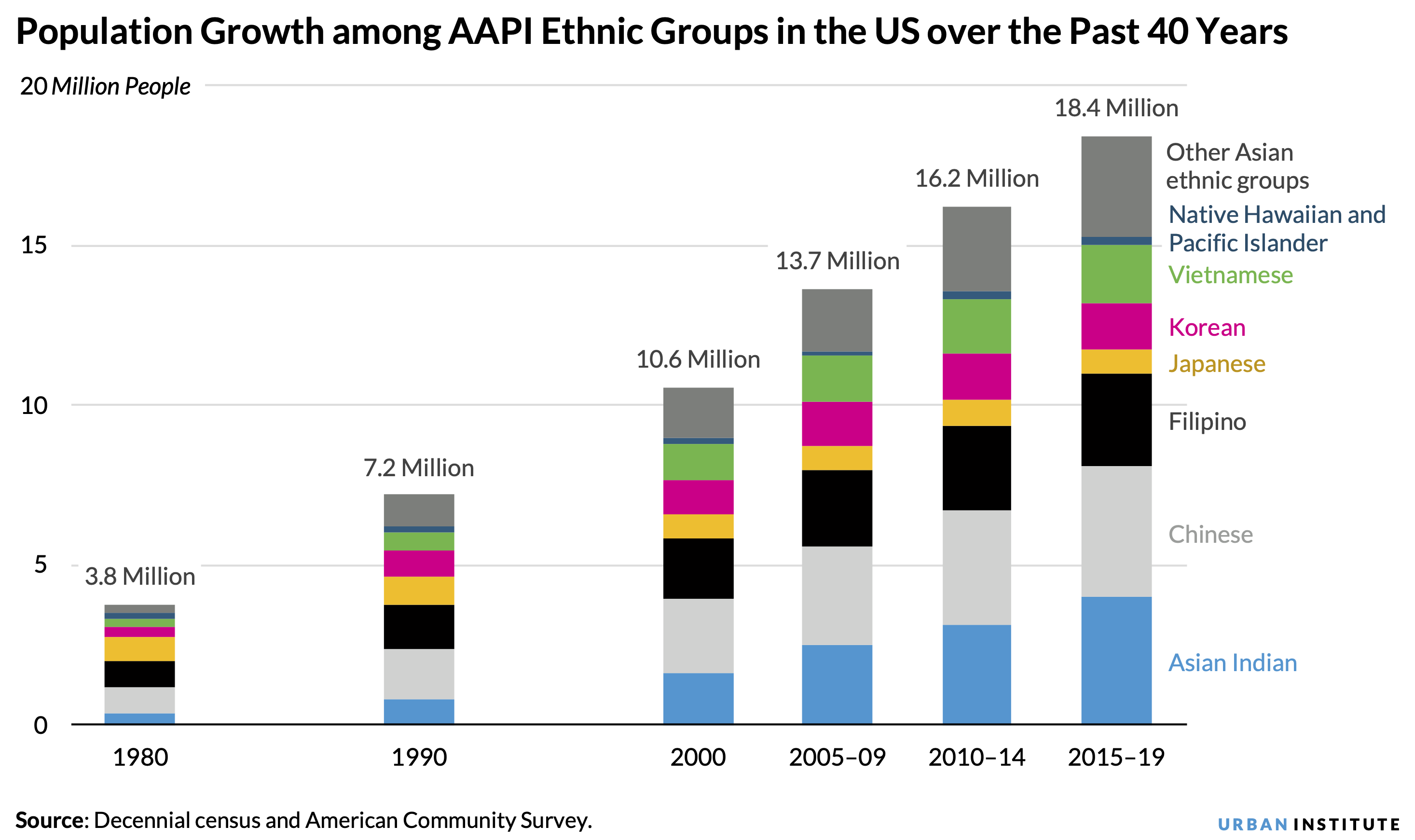

The Asian American and Pacific Islander (AAPI) population in the United States has increased significantly in the last 40 years, from 3.6 million in 1980 to 18.8 million in 2019. And since 2000, the AAPI population has experienced the fastest growth of any racial or ethnic group in the nation.

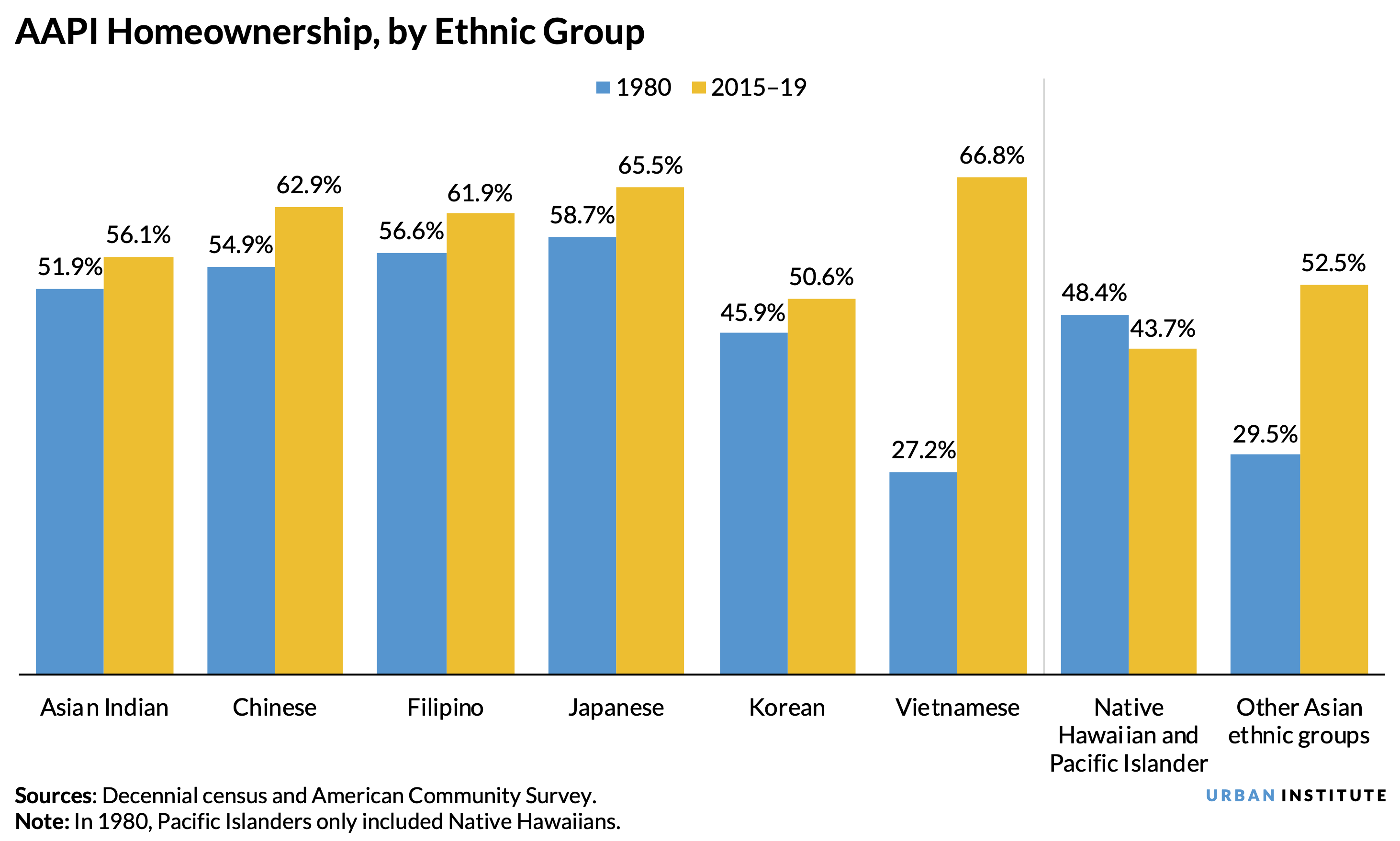

Despite structural barriers to homeownership, AAPI homeownership rates have also collectively increased since 1980. But people often overlook the substantial homeownership differences among AAPIs. These disparities reflect diverse experiences within the AAPI community, which encompasses people from more than 40 countries.

By 2060, the AAPI population is expected to surpass 38 million. Before then, policymakers and researchers will need to better understand the homeownership disparities among this diverse community if they want to eliminate unique barriers each subgroup faces to accessing homeownership and building wealth.

Population, homeownership, and income gaps within the AAPI community

We chose to focus our analysis on the six Asian ethnic groups by country of origin with the largest populations in the United States: Asian Indian, Chinese, Filipino, Japanese, Filipino, Korean, and Vietnamese.

We also created two separate groups, “Native Hawaiian and Pacific Islanders” and “other Asian ethnic groups,” to categorize the remaining Asian ethnic groups. We did this because of limited data on these two groups, but we recognize that lumping groups into categories like “other” can erase the experiences of certain communities. Much research excludes smaller and marginalized AAPI groups, and we believe it’s critical that future research and policy conversations address the often-overlooked challenges these underrepresented communities face. We hope this post can serve as encouragement.

The six largest groups accounted for about 82 percent of all AAPIs in 2019. Over the past 40 years, each group’s population increased, but the growth rates varied. Similarly, although the overall AAPI homeownership rate has substantially increased since 1980, this growth has not been equal across groups.

With the exception of Vietnamese and Asian Indian groups, lower income is associated with lower homeownership rates. The median income for all AAPI households from 2015 to 2019 was $88,204, and all ethnic groups had median incomes above the poverty level. Historical and social contexts influence homeownership trends among the AAPI community.

Why homeownership gaps exist among the AAPI community

Disparities in AAPI homeownership rates vary depending on each ethnic group’s economic status, history in the US, citizenship status, and much more. The following facts about each group we studied provide a glimpse into the reasons behind these homeownership differences. But again, they are not comprehensive, and much more research is needed to understand their causes and effects and to paint a full picture of AAPI homeownership in the US.

Vietnamese people have had the highest share (88 percent) of US citizens and the largest share of people (65 percent) who have lived in the United States for more than 20 years among the AAPI subgroups studied. Higher citizenship rates and longer residency in the United States create more permanency and thus increase the likelihood of obtaining homeownership.

Most Vietnamese people came to the US following the Vietnam War, which ended in 1975. Unlike other AAPI groups, many of whom return to their country of origin, nearly all Vietnamese people came to the US intending to stay permanently.

Although a greater share of Vietnamese households is citizens and homeowners compared with other AAPI groups, their mortgage denial rates were the highest and their median home values were the lowest between 2015 and 2019. These higher denial rates and lower home values may reflect their lower income levels relative to other AAPI households, which stem from their relatively lower educational attainment, and the struggles they face in purchasing higher-cost homes.

Despite Korean households having one of the highest citizenship rates and shares of people living in the US for 20 years among AAPI households, they had the second-lowest homeownership rate and one of the highest shares of people earning less than $50,000 in income between 2015 and 2019.

Because Korea rapidly transitioned from a low-income to high-income country, a greater share of Koreans who emigrated to the United States before the 1990s had relatively lower incomes—though many were high skilled--compared with Koreans who arrived more recently.

Today, only 55 percent of Korean households with household heads over age 65 are currently homeowners, a rate about 15 percentage points lower than that for all AAPI households in the same age group. Korean households with younger household heads between ages 35 and 44 had a similar homeownership rate compared with all AAPI households at 52 percent.

Many Japanese Americans entered the US in the earlier waves of immigration to the US, and new entrance has slowed over time. With relatively higher income levels and a significantly older population than other AAPI groups, Japanese households have the second-highest homeownership rate at 66 percent between 2015 and 2019. Older populations are more likely to become homeowners, and more than 57 percent of Japanese households were over age 55, compared with the 32 percent average across all AAPI groups.

The three groups with the next highest homeownership rates—Chinese Americans (63 percent), Filipinos (62 percent), and Asian Indians (56 percent)—all have relatively high incomes, and their employment is concentrated among the highest-paying sectors. Fifty-one percent of Asian Indians and 44 percent of Chinese Americans work in computer service and management positions, and 37 percent of Filipinos work in health care and management positions.

Although Asian Indians have by far the highest median income levels ($118,733) of all the ethnic groups, their homeownership rate (56.1 percent) actually falls below the overall average for all AAPI households (59.6 percent) between 2015 and 2019. This may reflect fewer Asian Indians obtaining US citizenship compared with other groups, as many of them have arrived in the US more recently. By contrast, relatively higher homeownership rates among Chinese and Filipino households may reflect their greater citizenship rates, longer time spent in the US, and higher income levels.

More research is needed to increase awareness of the diversity within the AAPI community

Though AAPIs are often treated as a single population, the group consists of many different communities with large differences in homeownership by country of origin, similar to their differences in history, culture, food, and language. But the average variables that reflect the socioeconomic status of the AAPI community, which suggest that the group fares relatively well, tend to overlook these differences.

We’ve touched on the unique homeownership trajectories that some AAPI groups have experienced, but additional research that further explores these trends and reasons for disparities is needed. When equipped with that information, policymakers and housing stakeholders can better prepare for this growing community’s future housing needs.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.