<p>People walk past the Marriner S. Eccles Federal Reserve Board Building in Washington, DC on June 19, 2015. Photo by Andrew Harnik/AP.</p>

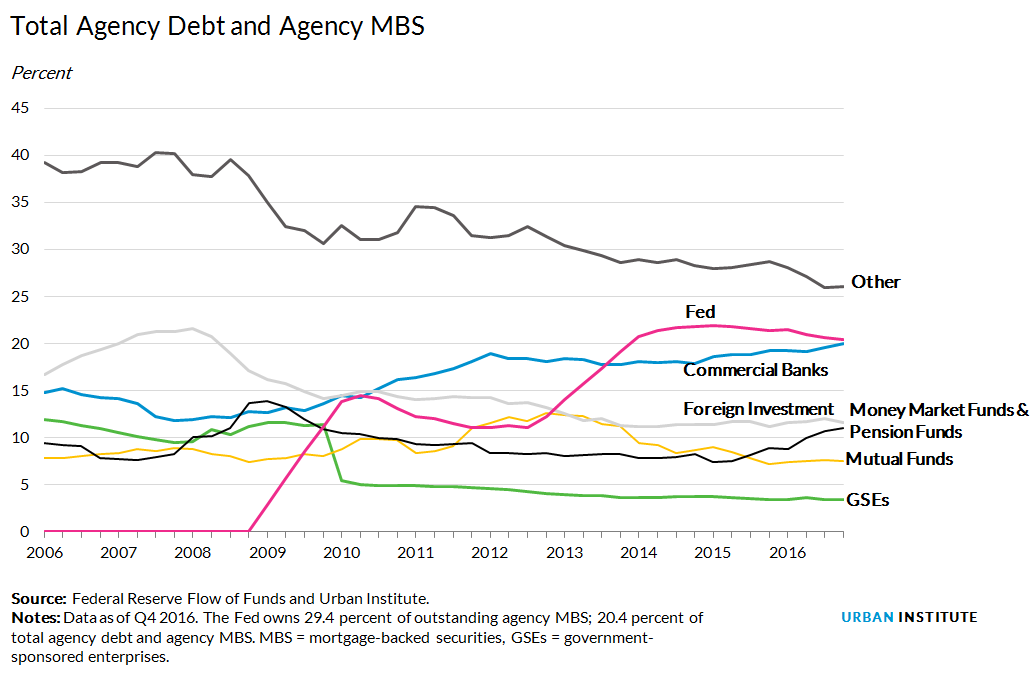

The Federal Reserve currently owns nearly 30 percent of the market that allows global capital to fund US mortgages: the agency mortgage-backed securities (MBS) market. The Fed began buying MBS in 2009 to support what was then a fragile housing market. With the economy now improving, the Fed may start unwinding its MBS holdings later this year or early next year.

The Fed is the single largest holder of MBS today, so there is no question that its pullback will have important implications for the mortgage market. But how the Fed approaches this exercise will matter almost as much, with consequences for housing affordability and beyond.

What are agency mortgage-backed securities?

The government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, along with Ginnie Mae, a government agency, aggregate mortgages from lenders and pool them into mortgage-backed securities. Investors then purchase these securities for cash, which lenders use to originate mortgages. A decrease in investor demand for these securities would reduce the supply of funds, putting upward pressure on mortgage rates.

How can the Fed unwind its MBS portfolio?

The Federal Reserve has long maintained that it will not start winding down its MBS holdings until it begins increasing interest rates. After keeping the target interest rate in the 0.0 to 0.25 percent range for seven years from 2008 to 2015, the Fed announced three hikes between December 2015 and March 2017. As such, questions surrounding the unwinding of its MBS portfolio are beginning to surface.

The Fed has a range of options. A minimally disruptive strategy would be to gradually phase out reinvestments of principal pay-downs (prepayments, for example). A more aggressive option would be to cease reinvestments entirely. Once the Fed has ceased reinvestments, it could let the securities run off over time (because of prepayments, the average life of these securities is far shorter than their maturity) or sell them in the open market – the most aggressive option and something the Fed has said it is not considering. In line with this statement, a recent Fed survey of market participants showed that a large majority expect the Fed to start by phasing out reinvestments.

But even at a slow pace, unwinding will, over time, undoubtedly reduce a major source of demand for agency MBS. Therefore the Fed’s withdrawal will surely put some upward pressure on mortgage rates, although it will hardly be the only factor.

How will the Fed’s wind-down affect the housing market?

The exactly impact of the Fed’s pullback is nearly impossible to predict, and it will depend not only on which option the Fed chooses, but also on how it implements it. For instance, under the most likely option of phasing out reinvestments, the Fed will still need to decide how much of the principal paid down should be reinvested, and the pace at which this number ought to be reduced over time.

Equally important, the Fed will need to decide how to allocate reinvestment reductions across agencies—that is, should the reductions be pro rata to avoid any skewing of the market. If reductions focus on conventional MBS (those backed by Fannie and Freddie), any impact will be felt more by conventional borrowers. In contrast, if reductions focus more on MBS backed by Ginnie Mae, any impact will be felt more by first-time homebuyers, low- and moderate-income borrowers, and veterans, who depend heavily on FHA and VA loans (which are exclusively pooled into Ginnie Mae securities).

How the Fed begins to unwind could be crucial to housing affordability in the coming years. Baseline interest rates are already on an upward trajectory, and house prices in several areas are already unaffordable and out of reach for many.

The Fed’s wind-down raises another important policy question about the future of housing finance: should the agency MBS market continue to rely on the federal government for protection during turbulent times? Before the financial crisis, Fannie Mae and Freddie Mac acted as a backstop through their retained portfolios, but at a substantial risk and cost to the taxpayer. Currently, the Fed provides this backstop, though its rationale and mode of operation are very different from that of the GSEs. While the GSEs chose to buy opportunistically with a profit motive when spreads were wide, the Fed has purchased MBS more programmatically as a monetary policy tool.

As policymakers debate the future of housing finance, they will need to decide if there is any role for MBS market intervention in the future, and, if yes, the most appropriate structural framework for it.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.