<p> </p>

<p>(Maxian/Getty Images)<br />

</p>

Households of color often experience worse homeownership outcomes because of structural barriers, such as systemic discrimination in employment and mortgage underwriting, that reduce their ability to purchase a home, increase the likelihood of entering foreclosure, and contribute to persistently worse disparities over time.

Although inequities by race and ethnicity are persistent, we have demonstrated in past research that economic downturns can lead to even worse outcomes for people or households of color. In our most recent report, we illustrate how the structural barriers that affect households of color combined with an economic downturn would likely result in higher foreclosure rates across the city of Newark, relative to the state of New Jersey, absent federal forbearance policies and foreclosure moratoriums. These results reflect the short-term impacts recessions can have on already disadvantaged neighborhoods.

But the trend of mortgage delinquencies in Newark, as compared with the US overall, suggests that recessions can also have disparate long-term outcomes. In other words, uneven recoveries over successive economic recessions can contribute to persistent inequity by race and ethnicity.

To avoid these cyclical disparities from becoming more deeply entrenched, policymakers can focus on stabilization policies that help households in need. The Homeowner Assistance Fund (HAF), which targets low-income homeowners and homeowners of color, can help ensure these households and the places they live can fully recover from the COVID-19 economic catastrophe.

Using place-based analysis in Newark to understand potential trends by race and ethnicity

Newark has a large Black and Hispanic population relative to New Jersey and the US, with 84 percent of the Newark population either Black or Hispanic and only 12 percent considered non-Hispanic white in 2019. Comparatively, 34 percent of the New Jersey population and 30 percent of the US population were Black or Hispanic in 2019, and 54 and 60 percent were non-Hispanic white, respectively.

The large Black and Hispanic populations in Newark, which are also predominately low-income households, suggest that many of the racial and ethnic disparities identified by research can be observed in the city as well. Given the smaller Black and Hispanic share of the New Jersey and US populations, the structural barriers related to race and ethnicity may be smaller in those geographies too. As a result, comparing trends in Newark with those of the state or the country may echo many of the conclusions found when analyzing outcomes for white people with those experienced by people of color.

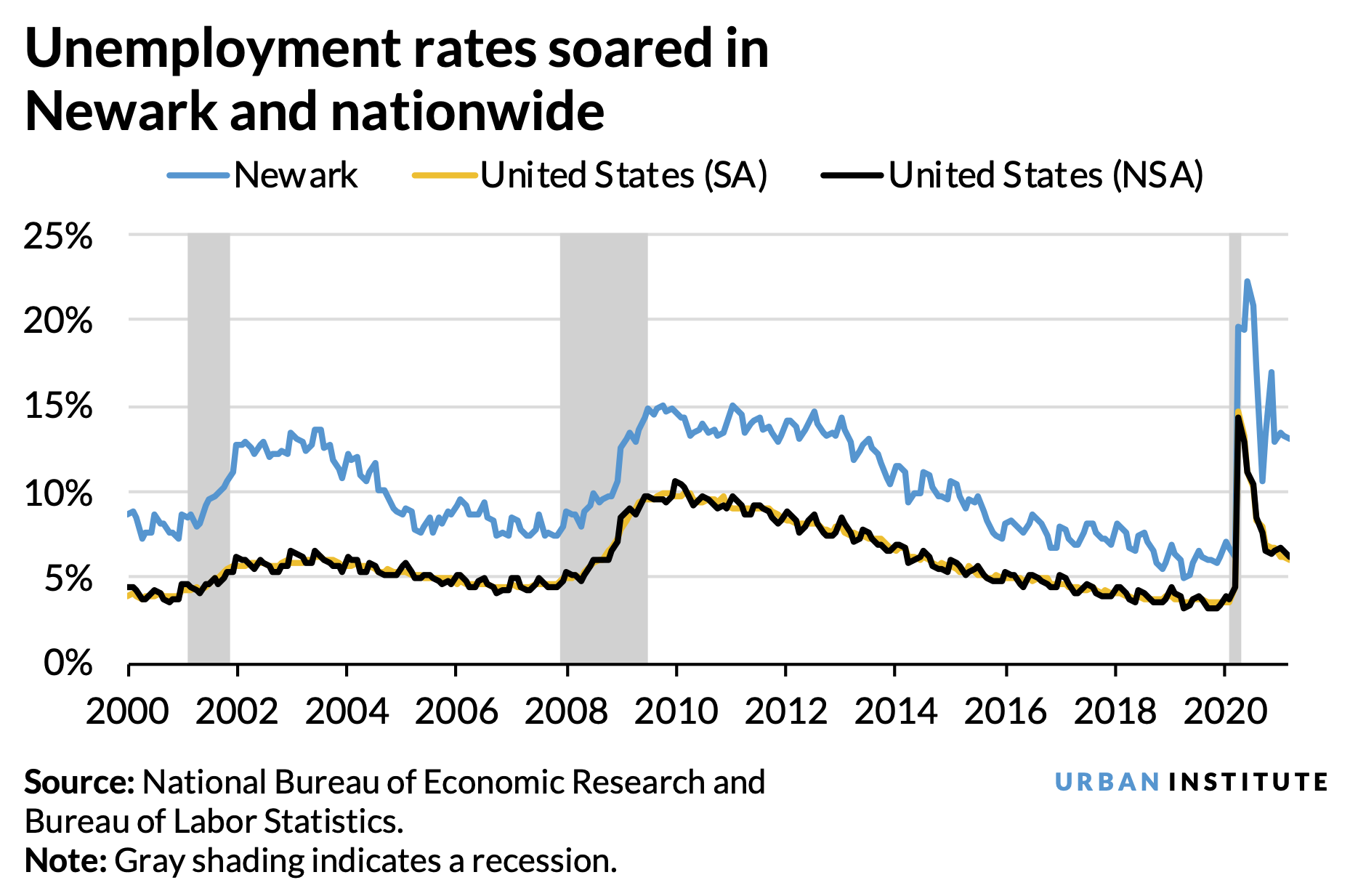

Using place-based analysis of Newark in relation to the US overall may explain the persistent gap in the 90-or-more-day mortgage delinquency rate. For at least two decades, the delinquency rate gap has remained. At the onset of both the Great Recession and COVID-19 economic recession, delinquency rates increased, and the gap between Newark and the US widened. These trends in delinquency rates are also consistent with a prediction of trends based on racial equity analysis.

Following the Great Recession, the delinquency rate gap eventually narrowed but never returned to its prerecession average. In January 2020, the gap was 3.0 percentage points, higher than the 2.2 percentage-point average between 2002 and 2006, a period during which the gap never exceeded 2.8 percentage points. This wider gap before the COVID-19 recession reflects the lack of a full recovery in Newark. In January 2020, the mortgage delinquency rate in Newark was 4.0 percent, which exceeded its 2002–06 average of 3.2 percent. In contrast, the mortgage delinquency rate nationwide reached 0.9 percent in January 2020, below its 2002-2006 average of 1.0 percent.

Before the delinquency rate gap in Newark could normalize, the COVID-19 recession caused the gap to widen again. During the pandemic, the gap exceeded its previous highs recorded after the Great Recession as the delinquency rates in Newark returned to their previous highs but the nationwide delinquency rates did not.

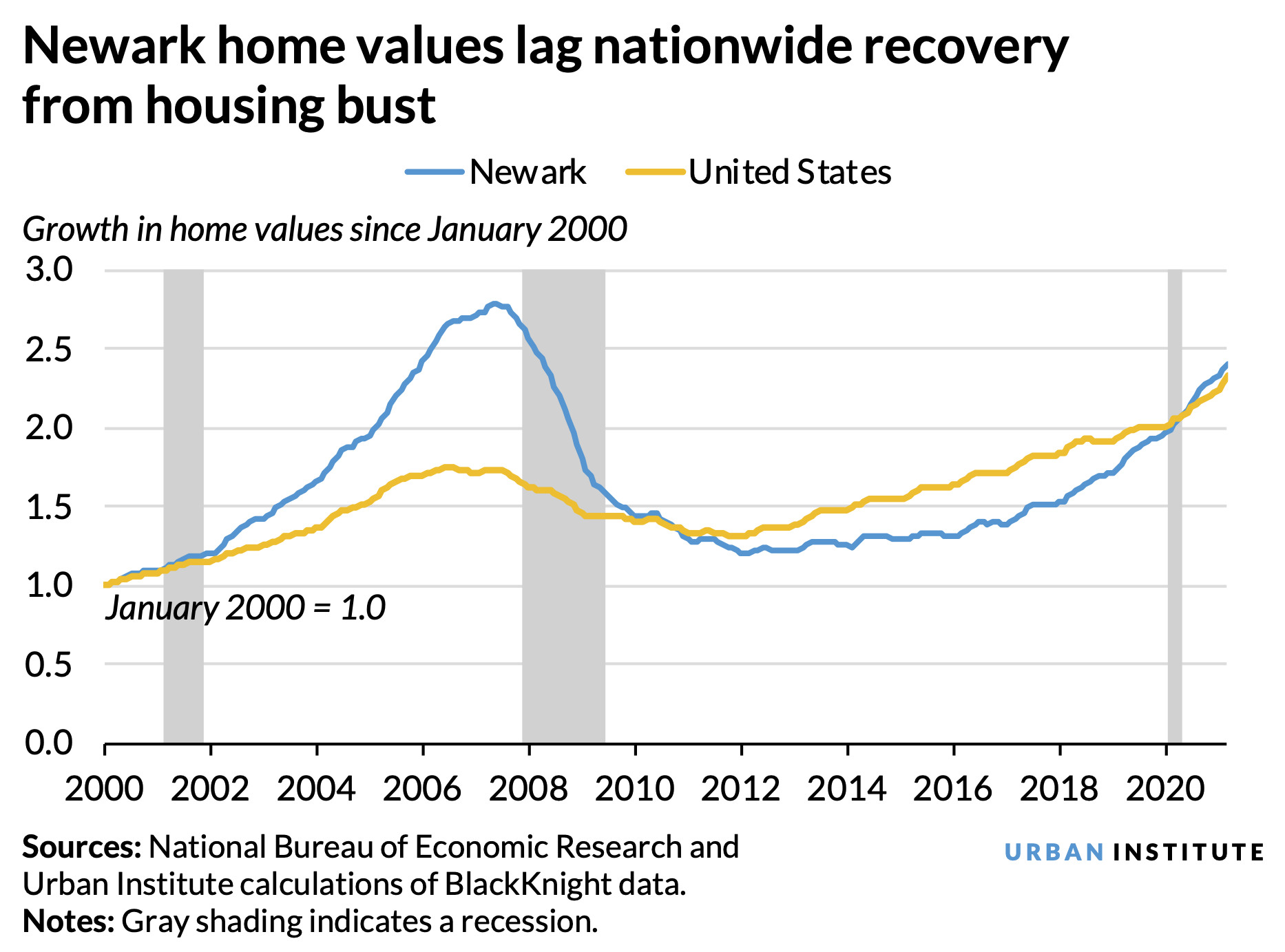

Mortgage delinquency reflects unemployment rates and house prices. In Newark, home values lagged in January 2020 relative to their high before the Great Recession. This lag suggests a larger share of households that remained homeowners through the housing bust also were underwater on their mortgage, which could explain the lack of a full recovery in delinquency rates. We estimate that 41 percent of mortgaged homeowners in Newark were still underwater as of January 2020, 10 times the nationwide rate of 4 percent.

Although home prices continued to rise throughout the COVID-19 recession, limiting the prospect of mortgage delinquency, its affect was overwhelmed, particularly in Newark, by soaring unemployment rates.

How the HAF can support homeowners most in need

If the delinquency rate gap between Newark and the US does not return to its pre-COVID-19-recession level by the start of the next economic downturn, these economic shocks would contribute to persistent long-term inequity in delinquency rates.

For policymakers, mitigating the potential for an uneven recovery is crucial. Through the HAF, nearly $10 billion is offered to states, the District of Columbia, US territories, Tribes or Tribal entities, and the Department of Hawaiian Home Lands to provide relief for homeowners in need. The fund explicitly targets low-income households (PDF), which will in turn assist many homeowners of color.

To ensure an equitable recovery, state-level policymakers should consider effectively targeting HAF assistance toward communities in need. Research suggests that many states, including New Jersey, may not receive enough federal aid to cover all missed payments. And structural barriers, such as a lack of internet access, may limit the speed and ability of policymakers to disburse these funds. Given the potential for the recession to solidify long-term inequities, policymakers should consider making every effort to guarantee that homeowners at risk of losing their homes can access funds to weather this crisis.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.