<p>Illustration by John Lamb/Getty Images.</p>

Recent news articles suggest that the significantly higher mortgage denial rates for black and Hispanic borrowers establish the presence of racial discrimination in mortgage lending. However, traditional mortgage denial metrics are flawed because they don’t control for the creditworthiness of applicants.

Our recently developed metric, the “real denial rate,” does just that. The real denial rate also reveals a gap between denial rates of non-Hispanic white borrowers and black and Hispanic borrowers, but the gap is smaller than that of the traditional metric.

A better way to look at mortgage denial rates and discrimination

The traditional method of determining mortgage denial rates, called the “observed denial rate,” divides the total number of denied applicants by the total number of mortgage applications. The observed denial rate shows that the denial rate for black families was 2.0 times that of whites in 2017, which looks alarmingly high (figure 1).

While the observed denial rate can be useful, it can’t provide evidence that equally qualified applicants are being treated differently because of race or ethnicity. To see disparate treatment by race or ethnicity, we must also consider applicants’ credit profiles.

The real denial rate method divides owner-occupied purchase borrowers in two groups: higher-credit-profile applicants (strong applicants that have virtually no chance of being denied a mortgage) and lower-credit-profile applicants (weaker applicants that have some chance of being denied a mortgage.) We then compare the number of denials to the number of lower-credit-profile applicants.

The observed denial rate was 9 percent in 2017 for non-Hispanic whites, 18 percent for non-Hispanic blacks, 13 percent for Hispanics, and 11 percent for Asians. Thus, observed denial rates for black families are 2.0 times that of whites, 1.4 times that of Hispanic families and 1.2 times that of Asian families.

Though the denial rates have moved around, the ratios have been constant over time for black families and have narrowed slightly for Hispanic families. These differences in denial rates partly reflect differences in credit profiles by race and ethnicity: in 2017, the average share of applicants with lower credit profiles was 47 percent for blacks, 40 percent for Hispanics, 29 percent for whites, and 24 percent for Asians.

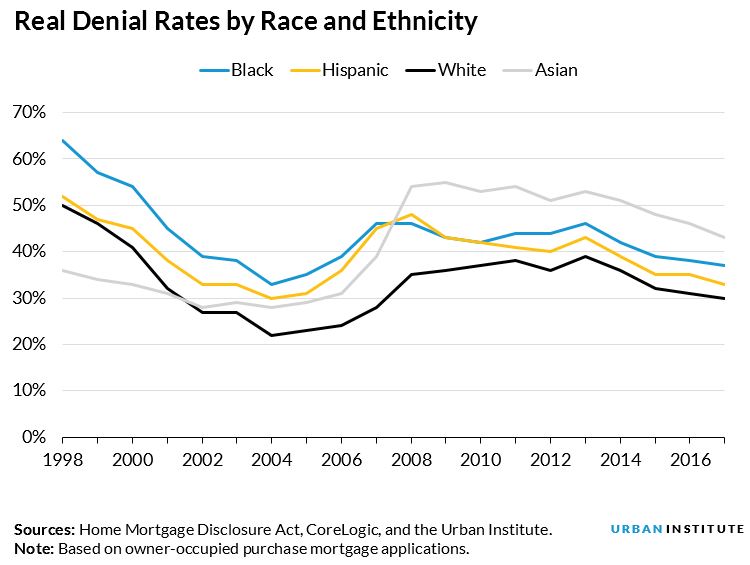

The real denial rate takes these differing credit characteristics into account and shows both higher denial rates across the board and smaller racial and ethnic gaps (figure 2). The higher denial rates stem from the fact that we are looking at the same number of denied mortgages, but the denominator includes denied applicants plus lower-credit-profile borrowers only, rather than all borrowers. Thus, the real denial rate is 30 percent for whites, 37 percent for blacks, 33 percent for Hispanics, and 43 percent for Asians.

Using the real denial rate method, the denial rate for black families is 1.2 times that of whites, while the rates for Hispanics and Asians are 1.1 times and 1.4 times, respectively, that of whites.

It may seem surprising that Asian borrowers have the highest denial rate, but a closer look shows that this stems from the low number of lower-credit-profile applicants in this group. The lending channel also matters: government loans (FHA, VA, USDA’s rural housing) generally have lower real denial rates than conventional loans, and Asian borrowers tend to rely less on government loans than other groups. By contrast, black and Hispanic borrowers tend to rely more heavily on government loans than do white borrowers.

To be clear, we still find differences in denial rates by race and ethnicity using the real denial rate method. But these differences are substantially smaller than that indicated by the observed denial rate.

The real denial rate provides greater insight into racial disparities in homeownership

Mortgage discrimination shown by the real denial rate arms policymakers with a more accurate and powerful tool to understand and address current problems in the housing market.

Since 2001, the black homeownership rate has seen the most dramatic drop of any racial or ethnic group, declining 5 percent compared with a 1 percent decline for whites and increases for Hispanic and others. We have helped sound the alarm about the losses in black homeownership, mapping the black homeownership gap and discussing the issue in many forums.

Our analysis using the real denial rate adds to this body of work by showing how the generally lower credit scores among blacks and Hispanics borrowers is a significant factor in their higher denial rates. Policy solutions need to focus on this disparity.

The real denial rate is still a blunt tool, because it requires the simplification of complex data and trends. It considers credit scores, loan-to-value ratios, debt-to-income ratios (DTI), and product and documentation types, but it does not consider income or income variability (we only have access to DTI; the lender will have more detailed financial information).

We are also unable to access information about borrower assets. Money in the bank can alter a borrower’s subsequent probability of default; this factor, which lenders do consider, is not captured in our analysis. Accordingly, to the extent black or Hispanic families have more income variability or are less wealthy than white families, we are not completely correcting for differences in credit profiles.

Proving the presence or absence of discrimination is difficult, but using the observed denial rate as a measure of discrimination is misleading. The real denial rate, though it has limitations of its own, paints a clearer picture and highlights the need for greater exploration of the large differences in credit profiles among different racial and ethnic groups.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.