<p>John Vega suffered damage to the base and walls of his trailer home and furnishings to swelling South Platte waters in September 2013. Between his insurance and FEMA, he has replaced floors, quarter walls and vents, and is living on the very same ground near this irrigation waterway. Photo by Joe Amon/The Denver Post via Getty Images on September 5, 2018 in Milliken, Colorado. </p>

Last year, Hurricanes Harvey, Irma, and Maria brought record damage to Houston, Miami, and Puerto Rico. As the recovery from Hurricane Florence begins, policymakers should think about the effectiveness of our current flood insurance system.

The number of flood insurance policies in force through the National Flood Insurance Program has declined over the past 10 years and stood at just over 5 million in 2018. Although private policies play a major role, and may play an increased role in the future, the current system leaves too many homeowners vulnerable when disaster strikes.

New data collected in a special edition of the recently released 2017 American Housing Survey (AHS) show that just over 1 in 10 homeowners have flood insurance nationally. But in cities that are more prone to flooding, such as Houston and Miami, the number is closer to 1 in 3.

These data also offer new insights. Of all homeowners who had a flood insurance policy in 2017, 60 percent chose to buy a private policy on their own accord and only 40 percent bought flood insurance because it was required by their mortgage lender.

We don’t know the reasons for this, but two possibilities are that mortgage borrowers are highly conscious of the extreme damage that floods can cause or that flood maps (on which required insurance are based) are outdated. In addition, because homeowners with no mortgage who buy flood insurance are not subject to insurance purchase requirements, this group may also contribute to the voluntary population.

What is flood insurance?

Standard homeowners insurance policies do not protect homes in the event of a flood, so homeowners need to buy separate flood insurance to protect their home and belongings from this type of damage. Owners are required to buy flood insurance if their home is in a high-risk flood area and they have a mortgage from a federally regulated or federally insured lender.

In addition, all Fannie Mae, Freddie Mac, Federal Housing Administration–insured, and Veterans Administration–guaranteed mortgages in flood zones require mortgage insurance. If they can afford it, homeowners can purchase flood insurance even if they do not live in a federally designated flood plain or do not have a mortgage.

What prompts homeowners to buy flood insurance?

In the 2017 AHS, survey respondents were asked about the presence of flood insurance and the reason for its purchase, including whether it was (1) required for mortgage, (2) bought after a neighbor bought it, or (3) bought for other reasons. Considering the second and third choices as voluntary purchases, we see some interesting trends for when and why homeowners choose to buy flood insurance.

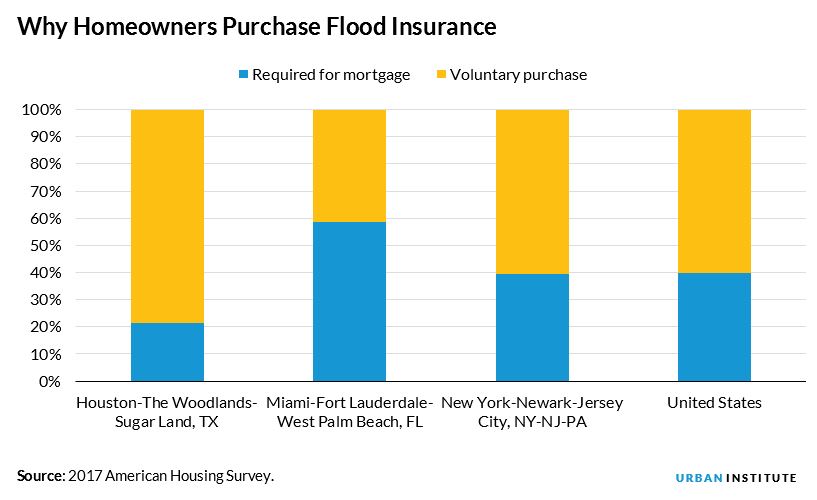

Most Americans with flood insurance purchase it voluntarily

Nationally, 40 percent of those who have flood insurance purchased it because it was required and 60 percent purchased it voluntarily.

In Houston, which was pummeled by Hurricane Harvey in August 2017, of the homeowners surveyed between April and September 2017 who had flood insurance at that time, 78 percent had purchased flood insurance voluntarily. Harvey’s recent damage may have spurred some homeowners to buy insurance, and the multiple floods in the years before Harvey likely led to an increase in the number of insured homeowners.

In Miami, which was traumatized by Hurricane Irma in September 2017, just 42 percent of homeowners with flood insurance had purchased it voluntarily when surveyed between April and September 2017. Even though hurricanes are common in this area, Hurricane Andrew in 1992 was the most recent significant storm to hit the region, so it’s possible that homeowners were lulled into a sense of security.

In New York City, where hurricanes are less frequent but memories of Hurricane Sandy loom large, 60 percent of homeowners—right at the national average—had purchased voluntary flood insurance.

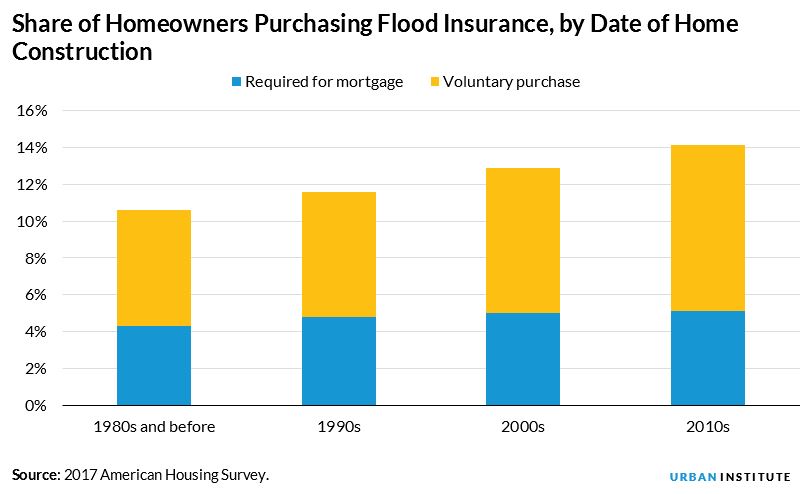

Flood coverage has increased for newly built homes in recent years

The share of voluntary flood insurance purchases is also higher for newly built homes compared with houses built 40 years ago. Flood insurance coverage increases from about 11 percent for homes built in the 1980s to 14 percent for homes built between 2010 and 2017.

For homes built in the 1980s, just 59 percent of homeowners with flood insurance voluntarily purchased it, compared with 64 percent for homes built since 2010.

This trend suggests that owners of newly built homes, which are generally more expensive than existing homes, are more cognizant of the possibility of flooding and are looking to protect their investment.

Flood insurance can be critical in getting homeowners and entire communities back on their feet after natural disasters, and the new AHS data reveal that current flood insurance holders are opting into this protection. Given the usefulness of these data, researchers and policymakers would benefit from the Census Bureau permanently including this question in the biennial AHS.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.