<p>Illustration via LinorR/Getty Images.</p>

Technology is changing the way we finance, renovate, build, buy, and sell homes. Investors are eager to cash in, with venture capital in real estate technology skyrocketing from $20 million in 2008 to $3.4 billion in 2017.

Yet less than 15 percent of homes were sold online in 2017, pointing to vast potential for more growth and change.

In a recent brief, we explore how financial technology, or fintech, is penetrating and affecting the owner-occupied housing market. Substantial innovation has altered the mortgage ecosystem, boosting efficiency and benefitting consumers, but major gaps exist in the provision of fintech services.

Little progress has been made toward easing structural barriers in the housing market, such as expanding housing affordability and improving access to credit. We hope and expect that improvements in these areas will take place in the coming years as fintech start-ups mature into established companies.

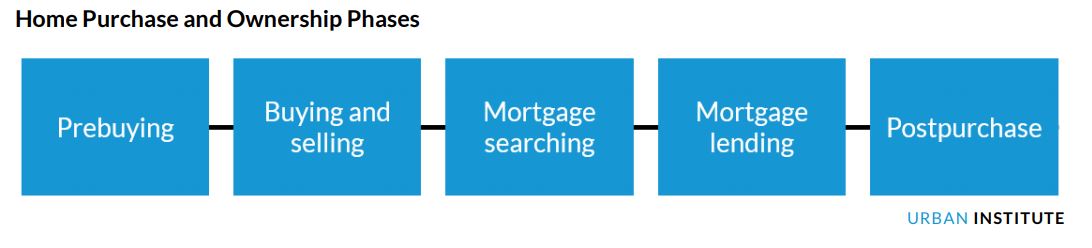

Our recent brief provides a landscape analysis of fintech activity across the five phases of the homebuying process:

Fintech is changing each of these phases, but certain segments of the market might be less conducive to technology innovation, and market, legal, or regulatory barriers might discourage innovation.

Our analysis reveals three impacts of fintech on homebuying.

1. Boosting efficiency

Technology and automation is streamlining the homebuying process. For example, the speed of processing mortgage applications for fintech lenders is about 20 percent faster than it is for nonfintech lenders.

2. Improving the mortgage buying process

About three-quarters of fintechs in the homebuying space work in the mortgage lending phase. Nevertheless, the end-to-end mortgage buying process is less automated than the process for other loan products.

We believe this is partly because of the fragmentation of the mortgage process, which is controlled by different entities at different points.

Many firms focus on only one part of the process and may not have an incentive to improve the whole process, which can require substantial resources and may yield uneven benefits. Consumers will benefit more when innovations enable seamless handover of the process from one entity to another.

3. Starting to address structural barriers (but more needs to be done)

Some fintech firms are attempting to address structural barriers to mortgage lending by helping less wealthy consumers build credit, which can could help them qualify for a mortgage.

Although this trend is encouraging, we’ve yet to see major innovations that help approve more borrowers for mortgages, as access to credit remains tight by historical standards.

These impacts raise three questions.

1. Who really benefits from fintech?

Some research finds that fintech firms are more likely than nonfintech lenders to lend to consumers from nonmetropolitan areas (PDF), where there tends to be less lender competition and lower borrower credit scores. This suggests that fintech firms may be penetrating previously underserved markets.

But other studies find that fintech lenders are more likely to provide loans to more creditworthy borrowers, that they a charge premium for the convenience, and that interest rates for mortgages originated by nonbank fintech firms are higher on average than rates charged by traditional banks.

2. Is fintech helping communities of color?

Some research shows that fintech lenders discriminate less than nonfintech lenders (PDF), while other research finds that both fintech and nonfintech lenders charge higher interest rates to minorities. More research finds that lending discrimination goes away after correcting for upfront points and rebates.

These findings may seem confusing, as few studies have looked at this issue. We need to continue to monitor how different consumers and communities are affected by fintech and newly developed fintech products.

Both policymakers and those who produce fintech products should make inclusion a priority to ensure everyone can access the benefits of innovation.

3. When will fintech reach mortgage servicing?

Costs for mortgage servicers have increased significantly in the past decade, particularly servicing nonperforming loans, but this high-touch, labor-intensive function that requires substantial in-person interaction has proven difficult to automate using technology. We are seeing some new fintech entrants hoping to change this.

The benefits of fintech in the homebuying process have been lopsided, with big advances in efficiency but little progress in easing structural barriers to homeownership.

Identifying the impediments to progress in this area should help expand the benefits of fintech beyond those already well served by the current housing market.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.