A recent Pew Research Center report-- Wealth Gaps Rise to Record Highs Between Whites, Blacks and Hispanics -- reveals that in 2009 the gap between white households and black and Hispanic households was twice as large as it had been over the two prior decades. Whites had 20 times the wealth of black households and 18 times the wealth of Hispanic households.

While the gap is alarming, as heavy media attention to the study attests, even more distressing is the absolute level to which African American and Hispanic wealth had fallen. Median wealth for Hispanic households was only $6,325 in 2009, down 66 percent from 2005. For African Americans, the percentage drop was somewhat smaller (53 percent), but they had only $5,677 in median wealth in 2009. This tiny cushion compares to $113,149 for white households and $78,066 for Asians.

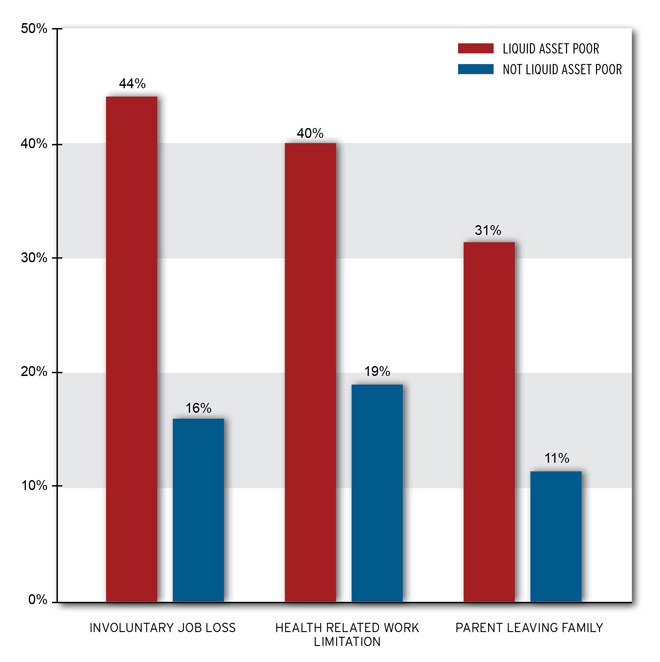

This decline in wealth comes during a precarious economic time when households need assets to replace lost income and fund personal advancement. Research by Urban Institute senior fellows Signe-Mary McKernan and Caroline Ratcliffe with Katie Vinopal has shown that assets can soften the blow when unemployment or poor health strikes families. A reserve can also fund a college education or a new family business. Increasingly, workers are also expected to supplement Social Security and private pensions or retirement funds with other savings.

Percentage of Families Who Experience Material Hardship, Given an Adverse Event, By Asset Poverty Status

The burst housing bubble was a major factor in the decline for all households. But because African American and Hispanic households have proportionally more of their assets tied up in housing than white households, these minorities suffer more from this decline. Hispanics found themselves concentrated in the states hurt most by the housing collapse. For African Americans, personal foreclosure problems combined with high foreclosure rates’ impact on housing values in their neighborhoods most likely account for their situation.

So is the best way to avoid wealth declines in the future to discourage more people from homeownership? Not when housing is still the easiest way for most people to build significant assets over the long term. That means that the real question is what policy options work best when few government resources seem to be available. One option would be to make the homeowners mortgage interest deduction more progressive. As McKernan and Ratcliffe point out in Enabling Families to Weather Emergencies and Develop: The Role of Assets, tilting the deduction more toward moderate income families could do more to reduce the cost of homeownership for moderate income households than the current structure.

Now that Congress is seeking ways to reduce federal budget deficits, a bold look at the huge tax expenditure of mortgage interest deductions should include options that would favor the less privileged. Caps or limits on the deduction could be combined with a tax credit to benefit those who don’t itemize. Alternatively, a sliding scale deduction could give more moderate- income families a leg up .

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.