<p>Photo via Shutterstock.</p>

Many former students are not repaying their loans.

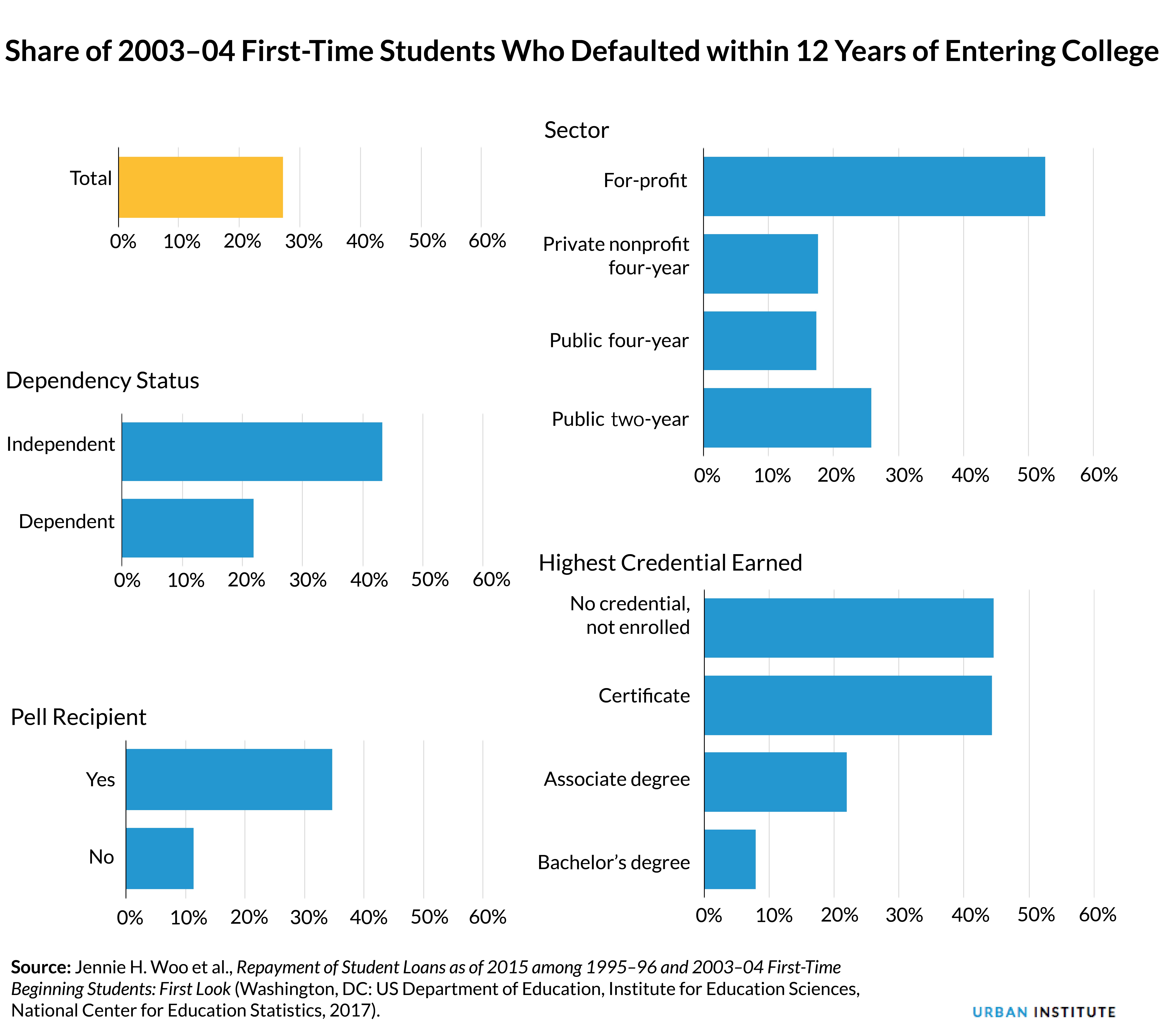

The National Center for Education Statistics (NCES) recently released a report detailing student loan repayment patterns for borrowers who first began college in 1995–96 and in 2003–04. Many of the numbers are startling. Twenty years after they began college, the median borrower in the 1995–96 cohort still owed 22 percent of the principal. Twenty-five percent had defaulted on at least one loan. Only 38 percent of borrowers had fully repaid their loans without defaulting.

These figures call for serious reconsideration of many aspects of our higher education system. It’s not just about student debt. We should be asking about how students choose where to enroll and what to study. We should be asking about the quality of the institutions and the programs the federal government funds through its financial aid system. We should gather better evidence about why so many students leave college without a credential. And we should learn more about why borrowers do not repay their student loans.

But to answer these questions, we have to look at more than averages. The data in the NCES report make it clear that the problems are concentrated among particular groups of students.

- Among borrowers in the 2003–04 cohort, only 8 percent of those who earned a bachelor’s degree had defaulted on at least one loan after 12 years. But the default rate was 45 percent for borrowers who had not earned a credential and were no longer enrolled in college, 44 percent for those who had earned a certificate, and 22 percent for associate degree recipients.

- More than half (53 percent) of borrowers who began at a for-profit institution in 2003–04 had defaulted on at least one loan after 12 years.

- After 12 years, the median amount owed by dependent borrowers in the 2003–04 cohort was 71 percent of the original principal. For independent borrowers, it was 96 percent.

- The median borrower who had received a Pell grant still owed 91 percent of the original principal after 12 years, compared with 43 percent for non-Pell borrowers.

Based on these data, the solutions lie not in entirely restructuring how student pay for college, but in focusing on how loans work for Pell recipients, independent students, and students at two-year or for-profit colleges.

Concerns about low completion rates at community colleges and for-profit institutions, which grant certificates and associate degrees, are widespread. These data suggest that even borrowers who complete these credentials struggle to repay their debts. There is wide variation in the payoff to these credentials, and too many students follow unproductive paths. And although there is variation across institutions in all sectors, loan performance in the for-profit sector demands a focus on protecting students enrolling in these institutions.

Independent students, most of whom are age 24 or older, are overrepresented at public, two-year and for-profit institutions. The federal government sets higher borrowing limits for independent students than for most dependent students. These students are more likely than dependent students to pursue certificates and associate degrees rather than bachelor’s degrees. As we urge adults to go back to school to improve their prospects in the labor market, we should think carefully about their experiences with student loans.

And Pell grant recipients—who are either dependent students from low-income families or independent students—have more difficulty than others repaying their loans. This is not surprising because students from more financially secure families have a fallback if they run into trouble. But it raises questions about the adequacy of grant aid and how effectively the large investment in financial aid narrows the gaps in resources between students from different socioeconomic backgrounds.

The new data on student loan repayment are not an indictment of the idea of borrowing to finance investments in higher education. But they do raise red flags about the groups of students who are not well served by the current system.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.