The Biden administration is developing regulations (PDF) to cut off federal grants and loans for career-oriented college programs that don’t seem to pay off for graduates. The gainful employment (GE) rule aims to protect consumers and taxpayers from overpriced and low-quality educations, but its debt-to-income test limits the rule’s effectiveness. A GE rule that compares graduates’ earnings to other metrics, such as tuition prices, could provide greater protections than the debt-to-income test.

The GE debt-to-earnings test

A key part of the Biden administration’s proposed GE rule (PDF) is similar to the Obama administration’s final rule from 2014, which the Trump administration repealed. It requires that certificate programs at public and nonprofit colleges, and nearly all programs at for-profit colleges, meet a debt-to-income test for graduates who received federal grants or loans. (We limit our analysis to certificate programs so we can include all types of institutions).

The draft rule measures the median annual student loan payment for a cohort of graduates against the cohort’s median earnings. If payments exceed 8 percent of earnings and 20 percent of earnings above 150 percent of the federal poverty level, the program loses eligibility for federal programs. But the details of the debt-to-income ratio show why the policy will have a more limited effect than would be expected. First, the GE rule measures median debt burdens among borrowers and nonborrowers (who received federal grant aid) as a group, meaning nonborrowers are included in calculating the annual debt payments and recorded as having $0 payments.

Though this approach is logical in that it treats programs more favorably if fewer students borrow (median debt payments are lower), it does not measure whether graduates can afford their debts. Annual loan payments calculated for a cohort of graduates can be heavily influenced by the share of students without loans, regardless of borrowers’ own loan balances, and borrowers’ debts appear artificially more affordable as the share of borrowers declines.

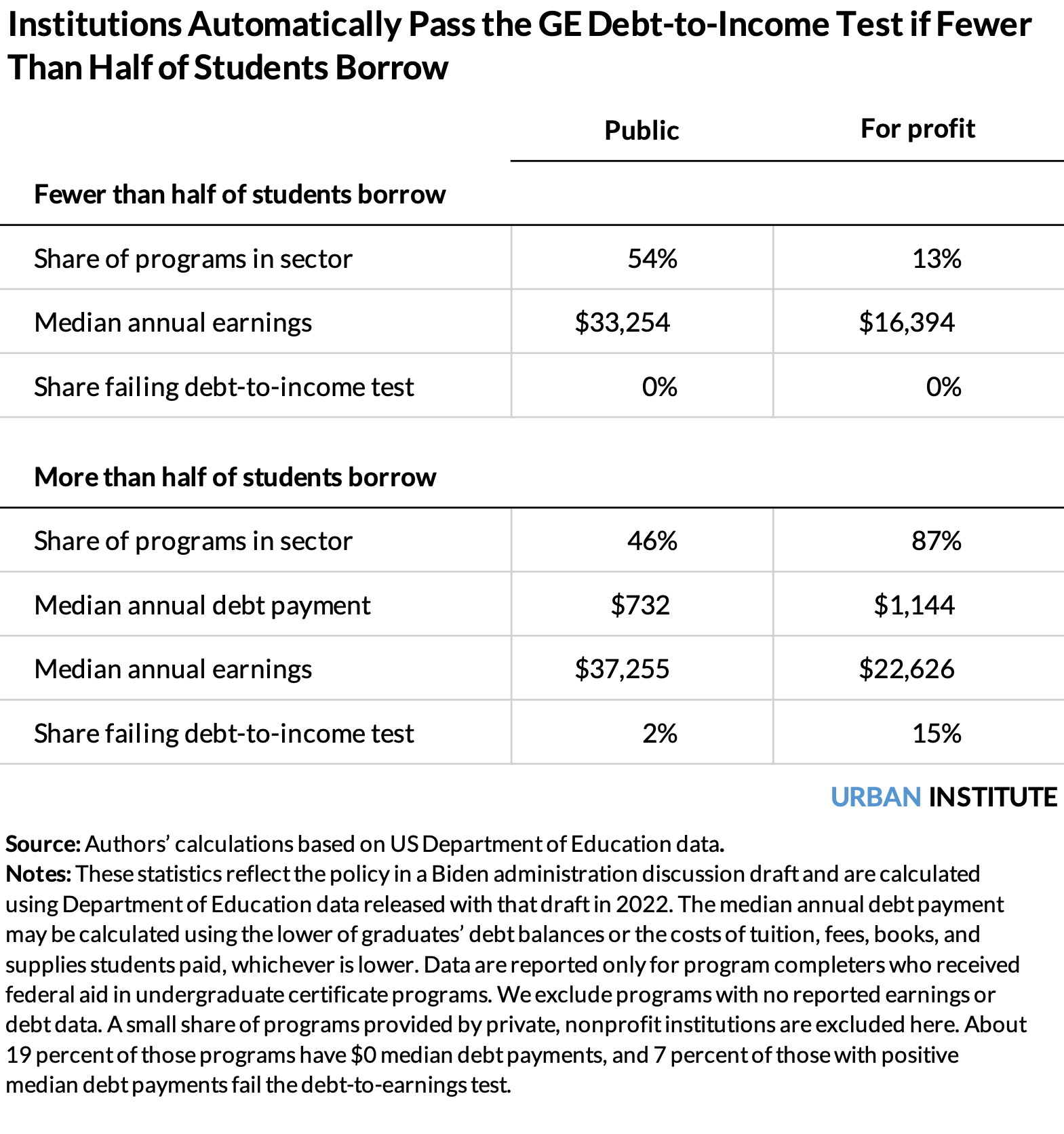

Including nonborrowers in the debt-to-earnings test is most problematic in programs where fewer than half of graduates have debt. The median debt payment in those programs is $0, meaning they automatically pass the debt-to-income test, regardless of borrowers’ actual debt burdens. In those programs, we don’t know how affordable the debt among borrowers is relative to their earnings. And there is evidence that their debts may be just as high as in other programs, as shown in figure 2.

Most of the programs that would automatically pass the debt-to-income test are at public institutions, according to GE data issued in 2022. Using data from the National Postsecondary Student Aid Study 2015–16 (NPSAS), we find that graduates who borrow in these programs take on similar debts as students at other institutions—just fewer of them borrow.

Certificate Completers Who Took Out Student Loans Have Roughly the Same Debt Regardless of Institution Type, 2015–16

Calculating the GE debt-to-income test based only on students who borrowed also introduces problems. Entire programs could be judged (and sanctioned) on the debts of a relatively small share of graduates. If only 10 or 20 percent of students take on debt, it may not make sense to assess the quality and affordability of the entire program based only on these students’ outcomes.

When GE measures tuition, not debt

Another trade-off in the debt-to-income test is that policymakers must decide whether to include loans for tuition and living expenses or only tuition. The Biden administration has opted for the latter. Specifically, colleges can have borrowers’ actual debt levels replaced in the debt-to-income calculation with what students were charged for tuition, fees, and course materials, if that number is lower.

This approach acknowledges that colleges have less control over students’ living expenses and that colleges cannot prevent students from using federal loans for these costs. But it also means that the GE rule does not reflect students’ actual debts, despite the fact that experts argue living expenses should be included in college affordability metrics.

According to the GE data from 2022, excluding debts for living expenses appears to significantly reduce the debt burdens for public institutions and slightly for for-profit institutions. Among public institutions where a majority of students borrow, the $732 annual debt payment in the GE data is about half what the NPSAS data suggest these students actually owe.

Strengthening the GE rule

Using debt as a key component of the GE rule forces policymakers to make trade-offs that compromise its effectiveness. To the extent that policymakers see the need for a test based on the cost to attend a program, rather than earnings alone, one solution would be to use tuition and related costs instead of debt, but in a way that is more transparent and consistent than how it is used in the proposed rule. A tuition-to-earnings ratio that covered students regardless of the type of federal aid they received, instead of a debt-to-earnings ratio (that sometimes measures tuition prices), could provide greater consumer and taxpayer protections.

Such a measure would treat programs with similar prices and earnings outcomes similarly, regardless of the share of students with debt, and it would clearly communicate to stakeholders that the standard is based on graduates earning enough to justify tuition and related costs.

The Urban Institute has the evidence to show what it will take to create a society where everyone has a fair shot at achieving their vision of success.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.