<p>Photo by Patricia Toth McCormick/Getty Images.</p>

To help more borrowers in distress avoid foreclosure and stay in their homes longer, Fannie Mae created the streamlined modification program in 2013. Borrowers were solicited for this innovative no-documentation program when they failed to respond to the requests for income documentation to participate in the Standard Modification program and Home Affordable Modification Program and were three months delinquent.

One would expect that a loan modification with no documentation required would have a higher use rate but a lower success rate relative to an equivalent modification with documentation. Our new report finds that both assumptions are correct and that the streamlined approach increases the total success of mortgage modifications by 34 percent.

If the streamlined approach had been available over the entire 2012–15 period, it would have prevented 6,100 additional foreclosures each year on Fannie Mae mortgages. This provides compelling evidence that the streamlined approach is beneficial to loss mitigation.

Streamlining generates significantly more use and slightly higher redefaults

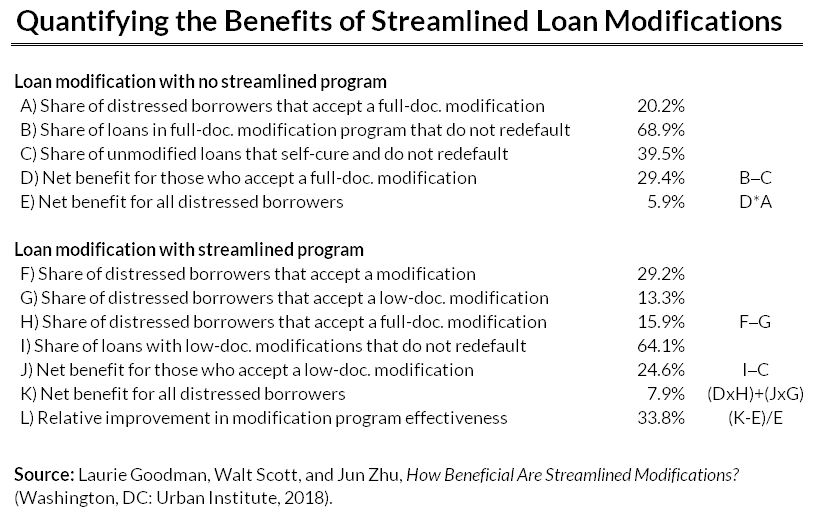

Using data from 2012 to 2015, we found that the rate at which distressed borrowers agreed to participate in a modification, or the “take-up” rate, improved from 20.2 percent without streamlining to 29.2 percent with the program. This is a 9 percentage-point, or 44.6 percent, improvement.

But streamlined modifications have a higher redefault rate, even after controlling for borrower characteristics because borrowers who submit documentation might be more motivated to make the modification work. We compared the success rates for streamlined modifications with standard modifications, a program with identical payment but more documentation requirements.

The success rate for streamlined modifications was 64.1 percent in the first 36 months after modification, compared with a 68.9 percent success rate for standard modifications, a 4.8 percentage-point difference.

To calculate the net benefit of the streamlined approach, we must also consider the loans that would have self-cured or otherwise been paid off if there had been no modification. Without a streamlined modification, the net benefit for all borrowers (take-up rate times the benefit for those who accept) is 5.9 percent.

That is, borrowers who took advantage of the standard (baseline) modification would have achieved a 68.9 percent success rate. But the cure rate without a modification would have been 39.5 percent, for a net benefit of 29.4 percent, which must be multiplied by the 20.2 percent of borrowers who took advantage of the modification.

With streamlined modifications, the total modification take-up improves 9 percent to 29.2 percent. About 15.9 percent of delinquent borrowers continue to submit full documentation, while 13.3 percent accept the modification offer with reduced documentation. But we observe a smaller net benefit for borrowers who accept a streamlined modification of 24.6 percent (the 64.1 percent success rate less the 39.5 percent cure rate without a modification). The net benefit of the entire modification program, once the streamlined option is introduced, comes to 7.9 percent, or nearly a 34 percent improvement over the baseline—a significant amount.

Innovation in loan modification is ongoing

In 2017, Fannie Mae and Freddie Mac introduced the Flex Modification program, or Flex Mod, replacing the myriad of modification programs in use at that time. This new modification program adopts the streamlined modification approach and allows eligible borrowers who are more than three months delinquent to obtain a mortgage modification without submitting any paperwork. If the borrower then makes the new payment for three months (the trial period), the modification becomes permanent.

Our research released today confirms that the streamlined modification approach adopted in this Flex Mod program is a positive innovation. We expect to see its widespread adoption by portfolio lenders and the private-label securities industry as well.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.