Our recent study “Lost Generations? Wealth Building among Young Americans” showed that young Americans are falling behind in building wealth. While the average wealth of American households doubled over the last quarter century, people in their 20s and 30s did not share in that growth. The average wealth of 20- and 30-year-olds in 2010 was 7 percent lower than the average wealth of those in their 20s and 30s in 1983. Those who took the largest hit were people ages 29 to 37 in 2010—their wealth fell by 21 percent. Why?

The foreclosure crisis gutted home equity

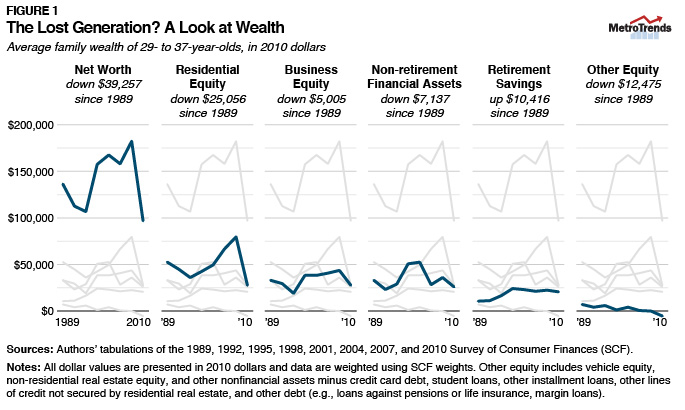

Lost home equity associated with the housing and foreclosure crisis played the largest role in the wealth declines for those ages 29 to 37. Their home equity fell by an astonishing 65 percent between 2007 and 2010, and a longer-term view also shows large declines in home equity for this group (figure 1). Between 1989 and 2010, home equity fell by nearly half.

People typically buy their first home in their early 30s, so many young adults bought their first home in the years leading up to the housing crash. These homeowners had large mortgages relative to their home value and many ended up in underwater mortgages. Of the young adults able to hang on to their homes, many were unable to take advantage of the low interest rates following the recession because they had little to no home equity, further limiting their ability to save and build wealth.

Ballooning student loan debt played a role Student loan debts are a smaller but still important part of the story. Student loan debt stands out because it has increased sharply in recent years while all other debts have fallen (figure 2). At roughly $1 trillion in our economy, student loan debt now exceeds credit card debt. For 29–37-year-olds in 1989, it was a relatively small component of debt; for 29–37-year-olds today, it is second only to mortgage debt.

Beyond the burden of paying back student loans, this early debt can have ripple effects, delaying homeownership and saving for retirement, meaning the process of building wealth is delayed.

Credit card debt was not a major factor

What about credit card debt? Is it a key driver in this "lost generation"? The simple answer is no. Credit card debt for younger Americans did rise prior to the Great Recession, following overall trends, but has fallen in recent years. Vehicle loans, business debt, and other types of debt have also fallen since the Great Recession.

Business equity and other assets fell…

Other pieces of the puzzle include drops in non-retirement financial assets and business equity, which were 22 percent and 15 percent lower for 29–37-year-olds in 2010 than in 1989 (figure 1). Non-retirement financial assets and business equity are important components of average wealth for this age group (nearly 30 percent each). However, nearly all young adults have non-retirement financial assets, while only a small minority owned their own businesses (1 in 10 in 2010, down from 1 in 7 in 2007 and 1989).

…but retirement wealth has been stable

On the positive side, the retirement wealth of younger Americans has been relatively stable over the past decade. Those who had their retirement savings invested in stocks and were able keep the money invested benefited from the recent recovery of the stock market. The increase in retirement wealth over the previous decade (figure 1) likely reflects the switch from defined-benefit plan retirement savings (which are not captured in these data) to defined-contribution retirement savings (which are represented in the data).

What steps can 30-somethings take to improve their wealth holdings?

Research shows that even people living below the poverty line can build wealth, so get started. Make saving automatic. Set up automatic deposits into a saving account each pay period for emergencies and into a tax-preferred account for retirement.

Despite the experiences of the Great Recession, homeownership remains a key avenue for wealth building for most Americans over their lifetime. It provides an automatic mechanism for homeowners to build wealth as they pay off the principal on their mortgages and as inflation erodes the real value of their debt, even in the absence of property value appreciation.

What can policymakers do to help?

Policymakers can help by focusing more attention on wealth building among younger households and other low-wealth groups. Reforming the home mortgage interest tax deduction, avoiding high down payment requirements for homeownership, and making higher education more accessible for low- and middle-income families are all important steps to help younger generations.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.