More homebuyers are paying in cash upfront

In the aftermath of the recession, a record share of homebuyers are foregoing mortgages altogether, paying the full sales price upfront and in cash.

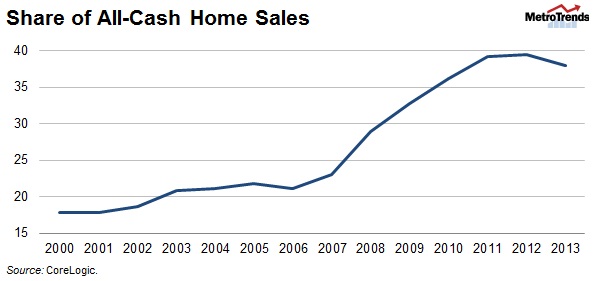

Between 2006 and 2012, cash sales jumped from 21 to 40 percent of home sales before declining slightly in 2013. But what’s driving these elevated cash sales and what does it mean for housing markets and communities?

{kind=link}

Investors entered when lower credit borrowers were locked out.

As a result of the financial crises, over the past six years, a total of nearly seven million borrowers have lost their homes through foreclosure and short sales. Moreover, the slow economy and tightening credit box have made qualifying for a mortgage increasingly difficult for creditworthy low- and middle-income households.

To absorb the large supply of distressed sales and replace the low- and no- credit buyers, investors stepped in, buying up homes to resell or convert to rental units, often at a heavily discounted price. Cash upfront became a competitive advantage when vying for potentially lucrative properties. As a result, the cash share of home purchases has climbed steeply, while the homeownership rate has fallen to 65 percent, down from 69 percent in 2004.

But most of these investors aren’t the big guys.

While media attention has focused on institutional investors managing huge stocks of homes as rentals, those investors are only a small part of the story. The majority of these cash purchasers are individuals who buy just one to ten homes in their own community, according to the Urban Institute’s Laurie Goodman, head of the Housing Finance Policy Center, who shared her analysis in a forum co-hosted by the Urban Institute and CoreLogic last Wednesday night: Cash Sales, Institutional Investors and Single-Family Rentals: Performance, Pricing, and Policy.

Here’s how Goodman interprets the census data: assuming an average sale price of $100,000, the approximately $25 billion in institutional money raised for home purchases equates to roughly 250,000 homes. Compare that with the nearly 4.5 million homes converted from owner-occupied to rental units between 2004 and 2013, and it’s clear that the big institutional players account for just over one twentieth of the shift.

The majority of investors are buying a smaller number of properties, hoping to make a profit off of rental income and rebounding prices, “a common theme throughout history” according to Mark Fleming, CoreLogic’s chief economist, another forum participant. “While institutional investors have been active in this space, they remain a relatively small share of the whole,” says Fleming.

What happens when investor activity ebbs?

Home prices would have fallen much further without investors absorbing the excess supply from distressed sales during the crisis. But the troubling part of this trend may be what happens next. We just don’t know the long-term consequences of neighborhoods transitioning from predominantly owner-to renter-occupied.

“Property management at this scale has never been done,” added Sara Edelman of the Center for American Progress. “We don’t have a whole idea of what’s going on” in neighborhoods with high concentrations of institutional investor units, whether the homes are adequately maintained, or whether prospective renters are fairly evaluated.

And with credit still far tighter than in the years before the boom, we don’t know what will happen to the housing market if overall investor activity continues to taper off. Oliver Chang, cofounder and director of Sylvan Road Capital, put it this way: “Many of the people who got in this to grab the appreciation didn’t understand how to manage scatter-shot single family rentals. Good progress has been made in getting up to speed and bringing these operations in house. But it’s hard and there is no roadmap.”

Sign up here to receive the Housing Finance Policy Center’s monthly newsletter, Housing Finance At a Glance, which contains the monthly chartbook, as well our blog posts, commentaries, events, and other news.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.