<p>In this Oct. 1, 2009 photo, appraiser Katherine Scheri conducts an appraisal at a 1920s-era Spanish bungalow in South Los Angeles. Photo by Reed Saxon/AP</p>

If you want a mortgage, you need a real estate appraisal, which means obtaining an appraisal is a part of the homebuying process for most homebuyers. But obtaining an appraisal has become a longer process in recent years, creating challenges for many Americans, like those who can’t afford to pay in cash.

How big is this problem, and what does the solution entail? Four experts on appraisals gathered at the Urban Institute last month to talk about improving their industry. The bottom line: the real estate appraisal industry must streamline the appraisal process, reevaluate professional requirements for new appraisers, and embrace new technology to meet the demands of today’s housing market.

Why is the real estate appraisal process so sluggish?

The slow pace of real estate appraisals can kill deals and give a big advantage to cash buyers over borrowers in the housing market.

According to Pete Carroll from Quicken Loans, appraisers fill out a long, outdated form that contains a lot of redundant information. And the process is slow in some markets and during certain times because of capacity issues with appraisers.

Zach Dawson from Fannie Mae explained that mortgage origination volume is highly variable, while appraisers’ capacity is relatively fixed. This difference leads to unpredictable earning potential for appraisers and volatility in costs and turn times for lenders and borrowers.

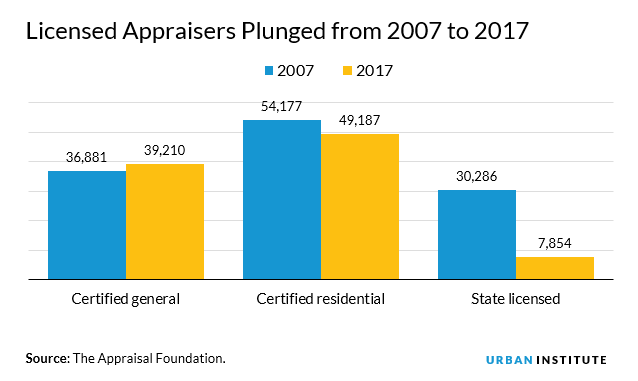

This disparity became a significant problem in 2016, as the government-sponsored enterprises saw unprecedented levels of appraisals performed by a static number of appraisers. The unpredictable earning potential for appraisers is a deterrent to new people joining the profession, and increasing education and experience requirements make it hard to become an appraiser.

David Bunton from The Appraisal Foundation confirmed that the fees appraisers earn don’t compensate them enough for all the additional work they do these days. He also pointed out that the appraisal industry is still transitioning from a trade, with apprenticeships, to a true profession. There are remnants of the apprenticeship system that technology could replace, like the required oversight of a supervising appraiser.

What are the solutions to these problems?

Simplify the qualifications. Dawson explained that we need a viable way to attract and retain professionals. Along these lines, Carroll argued that the college education requirement could be eliminated and the experience requirement could be shortened. He recommended targeted, relevant training and noted that the Appraiser Qualifications Board was moving in this direction.

But Bunton pointed out that, while the United States has only recently caught up with other industrialized countries in elevating the qualifications for appraisers, the Appraiser Qualifications Board is considering proposals that would allow people to gain experience through computer-simulated properties or by taking an advanced test that contains practical applications.

Sue Allen from CoreLogic suggested having an alternative pathway where appraisers could combine different amounts of experience and college courses to qualify for full licensure. She also suggested that honorable discharge from military service be included as a credential that counts toward licensure.

Streamline the appraisal process. Carroll suggested that the current appraisal process be shortened and simplified to require only relevant data. Creating a centralized database with market- and property-level data would become the centerpiece of a future process, though determining who owns and maintains the database poses some challenges.

Dawson agreed that we need to make the process more efficient, which could include alternatives to traditional appraisals or even appraisal waivers for some properties.

Embrace new technology. Technological advances could bring significant improvements (and disruption) to this industry. But, as Susan Allen from CoreLogic humorously demonstrated when discussing imaging technology, relying on technology can produce unique problems. And although drones can capture many images for a property, it’s more expensive to send a drone than an appraiser.

Bunton also pointed out that, although technology can perform well with homogenous housing stock, big data can’t always detect nuances. The system will always need human expertise, the type of analysis that professional appraisers are trained to provide.

Dawson reminded the group that the appraisals industry has made big strides. Fannie Mae has created a vast database of appraisal information for analysis while standardizing data collection, so everyone notes the presence of one and a half bathrooms the same way, for example.

This has allowed Fannie Mae to capture over 24 million appraisals, and then use these data to build their Collateral Underwriter, which helps lenders better assess an appraisal’s quality and allows Fannie Mae to waive many appraisal representations and warranties at origination.

Allen reiterated that technological advances must be tailored for specific uses, implementable on a large scale, and cost-effective to minimize errors. She also explained that early innovations may first come from home equity lending, where lenders already use more alternatives to a full appraisal, such as a desktop appraisal or an assessment by a real estate agent.

Leaders in the appraisal industry can help by exploring options for entering the profession, simplifying the process, and adopting new technology. These efforts can improve the real estate appraisal process for everyone, putting mortgage borrowers and cash buyers on more equal footing.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.