<p>Basketball great Earvin "Magic" Johnson, far left, and music industry executive Jheryl Busby, second from left, shareholders in a new national network of African-American-owned community banks, pose with Board of Directors members Kevin Cohee, center, Leon T. Garr, second from right, and Kenneth T. Lombard at a ceremony in Los Angeles, California, on Wednesday, May 2, 2001. Boston Bank of Commerce, Peoples Bank of Commerce in Miami and Founders National Bank of Los Angeles announced Wednesday the completion of a merger creating America's first black-owned national bank. (AP Photo/Chris Pizzello)</p>

Black banks support Black communities, lending mostly to Black homebuyers and maintaining community lending even in tough economic times. Recent interest in supporting these institutions is a welcome and positive step.

But their small sizes and declining numbers mean that today, they cannot tackle the problem of capital access in predominantly Black neighborhoods by themselves. To bring greater capital to communities of color, our recent study on the benefits and limits of Black banks suggests a two-pronged approach: increase capital to Black banks, and adopt policies that support community development financial institutions (CDFIs) more broadly.

Black banks are strong but small-scale supporters of Black communities

Most Black banks are headquartered in and support predominately Black neighborhoods.

The median share of mortgage originations to Black borrowers for owner-occupied homes is substantially higher among Black banks than among other lenders. The typical Black bank originated between 75 and 100 percent of its one-to-four-family purchase loans for Black borrowers between 2004 and 2018, averaging 1,260 purchase loans a year.

In contrast, the overall share of purchase loans to Black borrowers from other types of lenders never exceeded 10 percent over this same period.

Black banks practice relationship banking. They go beyond assessing a potential borrower’s financial status to account for the borrower’s personal needs and preferences developed over the length of their relationship. In so doing, Black banks are often able to creatively meet a diverse array of consumer credit needs within their community, producing greater access to credit to a wider group of borrowers through specialized underwriting practices that consider risk characteristics.

Black banks provide countercyclical mortgage lending during weak economic periods.

Amidst the Great Recession, mortgage credit availability tightened dramatically. During that recession and the initial stages of recovery when credit standards remained tight, Black banks increased their service to Black borrowers who were shut out of traditional channels.

Between 2007 and 2013, purchase mortgage originations by Black banks increased 57 percent. In contrast, purchase mortgages to Black borrowers overall dropped 69 percent over the same period.

Black banks are small in size and number.

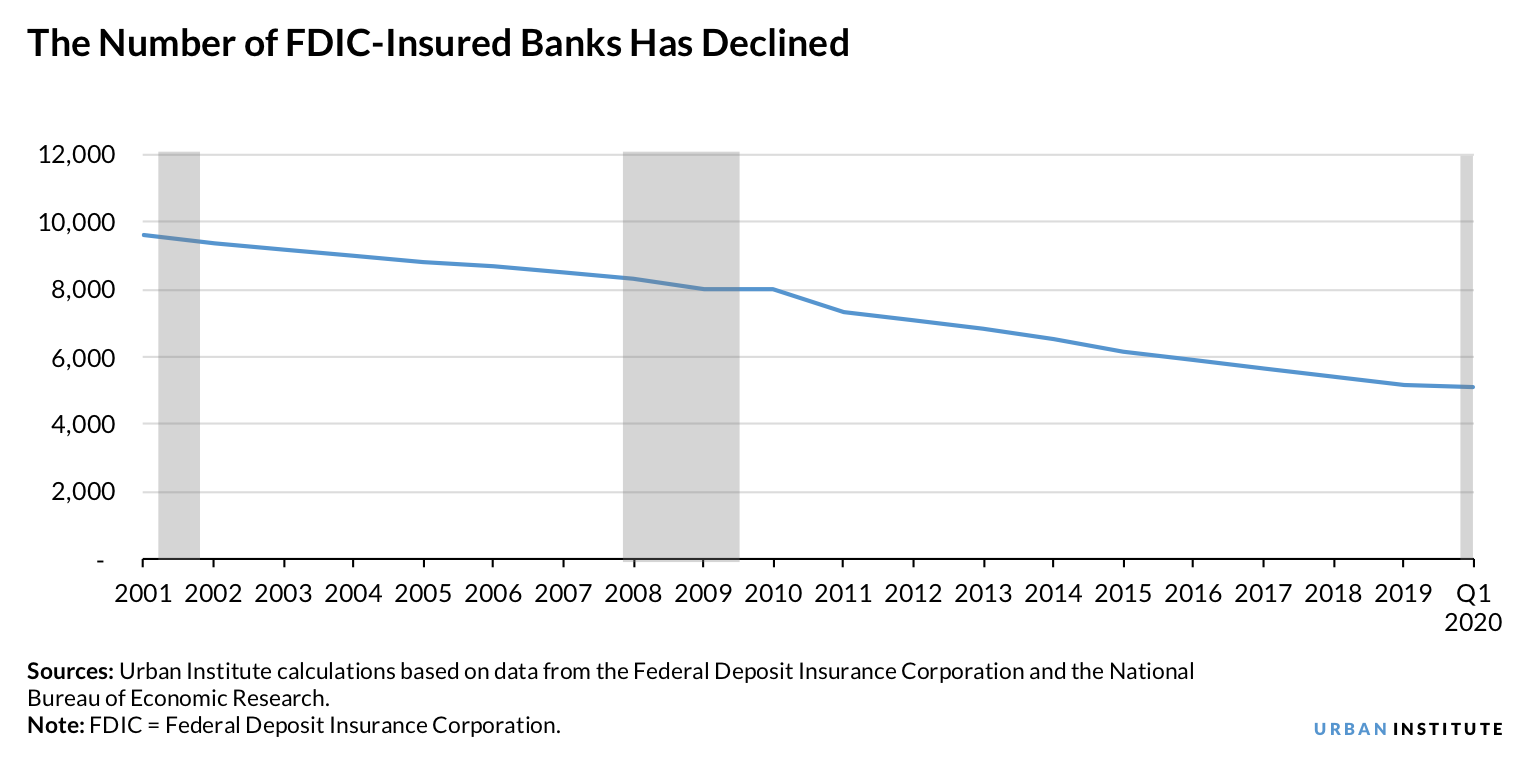

After 30 years of banking industry consolidation, the 21 remaining Black banks represent just 0.4 percent of the 4,681 community banks insured by the Federal Deposit Insurance Corporation (FDIC). And although the typical Black bank originates the majority of its purchase mortgages for Black borrowers, Black banks account for less than 1 percent of total purchase mortgage loans going to Black homebuyers in any given year.

Black banks are more susceptible during recessions.

The number of Black banks has declined since at least 2001. In the years leading up to the Great Recession, the number of Black banks shrank by 15 percent, from 48 to 41, proportional to the 14 percent decline in the total number of FDIC-insured institutions, 9,614 to 8,305.

But since 2008, the decline in the number of Black banks has fallen by 49 percent, to 21, while the number of banks overall decreased 38 percent to 5,116. In the first quarter of 2020, there were just 21 Black banks, a 9 percent drop from 2018. Over this period, City National Bank of New Jersey in Newark and Urban Partnership Bank in Chicago closed.

The activities of Black banks often help broader communities of color, which typically have lower incomes. These dynamics, during times of economic stress, can cause Black banks to fail. Research shows that minority-owned community banks experienced higher rates of failures and closures relative to non-minority-owned banks in the wake of the Great Recession, as Black households were experiencing significant loss of wealth through foreclosures and home equity losses.

Black banks need greater access to capital.

Access to capital has been an ongoing constraint for America’s remaining 21 Black banks. In aggregate, these banks held $4 billion in deposits in the first quarter of 2020. This makes Netflix’s reported $100 million cash infusion into Black financial institutions a significant and sorely needed investment in communities of color. This investment will help some Black families meet their financial goals, including homeownership, and support small business growth.

The FDIC has taken steps to raise awareness of minority depository institutions, but more can be done. Expanding access to capital for Black banks and other financial institutions targeting underserved neighborhoods, particularly during a crisis, can help spur home and business lending to Black families and bring much-needed economic development to communities of color.

Black banks cannot do the job alone. Enter CDFIs.

All financial institutions could better serve the Black community. But CDFIs, with their ability to tap into US Treasury funding, are already well positioned to make a difference in neighborhoods of color. Increased support for CDFIs by policymakers will also help most Black banks, as 18 of them claim this designation.

Public policies that support CDFIs would increase mortgage and small business loans to many Black communities and other historically underserved areas on a larger scale. More than a third of CDFIs are led by minorities, and more than 40 percent of CDFIs’ loans and investments go to majority-minority communities.

CDFIs can serve distressed communities, but they must expand their work to cover all areas in need across the nation. Policy ideas put forward by Urban Institute colleagues—such as adding state, local, and philanthropic support for community development capacity building, in addition to continued federal leadership and support—could address these shortcomings and maximize progress toward closing the racial and ethnic wealth gap through homeownership and other asset-building strategies.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.