<p>Photo by Hero Images via GettyImages.</p>

Historically, purchase mortgages have performed better than refinance mortgages, or “refis,” defaulting less often. But changes made in response to widespread appraisal bias during the crisis have improved the industry’s risk assessment and management abilities overall and, accordingly, have decreased the expected default rate on all mortgages.

We looked at the data and concluded that these improvements have reduced the difference in how purchase and refi mortgages perform. And while the models used in FHA, Fannie and Freddie underwriting systems are not public, our results suggest an update may be in order.

Reducing appraisal bias

The pervasive belief that appraisal bias, especially towards no-transaction refinances, was a significant contributor to the great financial crisis lead to a significant re-evaluation of the appraisal process after the crisis. Appraisals undergo much greater scrutiny today, and the GSEs commonly check these numbers against values generated from automated valuation models (AVMs). AVMs use mathematical modeling, drawing on a huge database of recent transactions, complete with property characteristics, to generate an estimated sales prices.

This increased scrutiny has made for more accurate appraisals and the AVMs have enabled Fannie Mae and Freddie Mac to share concerns with lenders about an appraisal prior to the execution of a mortgage, allowing the lender to take corrective action.

It was predicted that these developments would decrease the expected default rate on all refinanced mortgages, which were particularly susceptible to appraisal fraud. The data reveals that this has indeed been the case.

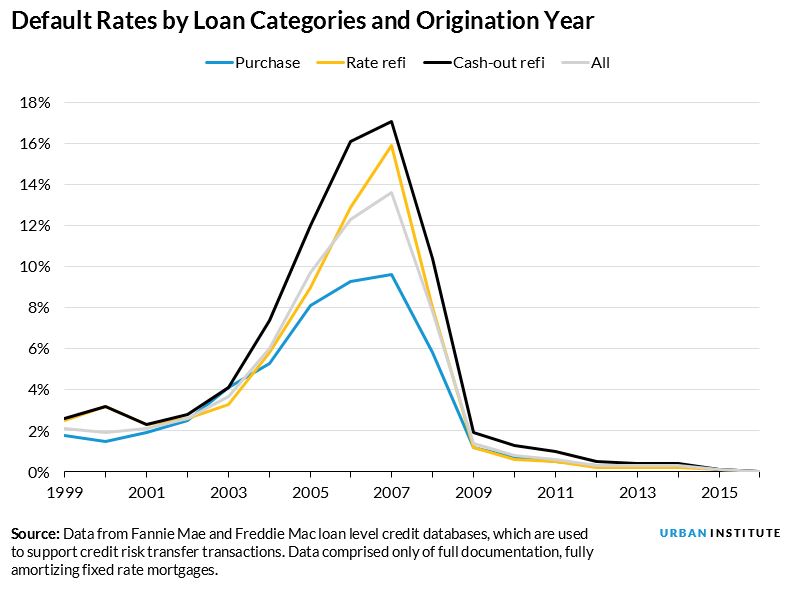

The performance of refis versus purchase mortgages

We examined the characteristics of three broad categories of mortgages:

- Purchase mortgages, which are obtained when a buyer purchases a home

- Rate and term refinance mortgages, which are obtained when a homeowner wants to refinance their home to take advantage of lower rates or to change the length of the mortgage

- Cash-out refinance mortgages, which are obtained when a homeowner wants to tap the equity that has accrued in their home

In an earlier paper, we showed that the risk characteristics of these mortgages—things like loan-to-value ratios (LTV), credit (FICO) scores, debt-to-income (DTI) ratios, and the percentage of owner-occupied loans—did not match the actual performance or default of these mortgages. The loan characteristics indicated that rate and term mortgages would default the least and that cash-out and purchase mortgages should default at about the same rates. But in reality, purchase mortgages defaulted the least, followed by rate and term refis, and then cash-out refis, which defaulted the most.

In other words, the rate and term refinance is riskier for a lender than a purchase mortgage, and a cash-out refinance is the riskiest of all.

But this has been changing (see figure above). The differential between rate and term refinances and purchase loans has been narrowing. This change is exactly what we would expect: as appraisals have become more reliable and AVM models have improved, LTV ratios have become more accurate, and the default differentials have narrowed.

Using regression analyses, we were able to examine the difference in risk characteristics in 2000 to 2009 loans and 2010 to 2017 loans. We learned that the rate and term refinances were 51 percent riskier than purchase loans in the first period but only 11 percent riskier in the more recent period. Cash-out refinances were 96 percent riskier than purchase loans in the earlier period and 55 percent riskier in the more recent period.

In other words, our analysis showed that while the loan characteristics still suggested that cash-out refinance mortgages would be the riskiest and purchase mortgages the least risky, the relative riskiness of the loans had narrowed.

Why do the different default rates between purchase and refinance loans matter?

The GSEs (though Fannie Mae’s Desktop Underwriter and Freddie Mac’s Loan Prospector) and FHA (though is Scorecard) decide which loans to approve using model based inputs on the riskiness of a given set of loan characteristics. Our results suggest that there has been a structural change in the systems which has lowered defaults, especially on refinance loans, and a recalibration of existing models may be order.

Secondly, knowing the default rates for these loans has implications for the proposed capital standards for the GSEs when they emerge from conservatorship (and it has implications for pricing in the interim). Their analysis looks at historical data to determine capital requirements. The standards, as they are currently proposed, require a 1.3 times premium for rate and term refinances and a 1.4 times premium for cash-out refinances.

Our results suggest that the cash-out refinance premium may be fair or a bit low and that the rate and term premium is too high.

A closer look at our methodology

We control for the factors that could drive defaults: LTV ratios, FICO scores, DTI ratios, interest rates, loan balances, and indicators for single-family, owner-occupied, and issue years. We also include an indicator for rate and term refinances and another indicator for cash-out refinances. Purchase loans are served as the reference category.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.