<p>Illustration by Alberto Ruggieri/Getty Images</p>

Since the presidential election, primary mortgage rates have increased from 3.54 percent to 4.13 percent, and the yield on 10-year US Treasury notes has increased from 1.83 percent to 2.40 percent.

The market is likely anticipating greater government spending and potential tax cuts that could increase demand and prices. These rate increases will have seven important consequences for the mortgage market:

-

Significantly fewer mortgages will be originated. The average rate on outstanding mortgages as of December 7 was 4.24 percent. A borrower must save at least 75 basis points (1 basis point is 0.01 percent) to find refinancing worth the cost and hassle. Using this assumption, refinancing would be economically worthwhile for 16 percent of current outstanding mortgages, down from 84 percent in 2012 and over 45 percent earlier this year.

Close to half of all mortgage originations were refinances in the first half of this year (see page 11). This interest rate change will eliminate most of these originations, slashing the number of mortgage originations and making mortgage banking less profitable.

- Home prices will rise. The same factors that are causing higher interest rates (greater demand, pressure on prices) will increase home prices. Higher prices should bring higher incomes, which will allow for higher housing payments. The cost of new homes also will be higher as labor and materials are affected by inflation, pushing up home prices from the supply side. This trend toward higher prices will be magnified by the inadequate supply of new units, a factor we don’t see changing quickly.

- Mortgage delinquencies and the number of underwater mortgages will decrease. As home prices rise, the amount of equity borrowers have in their homes will increase. Delinquencies will go down, as equity is one of the largest determinants of mortgage performance.

- Trade-up buying may decrease. Borrowers may be reluctant to sell their home to trade up, as they will face a higher mortgage rate on their new purchase. This will negatively affect home sales.

-

Access to credit is likely to expand. As mortgage bankers try to compensate for the huge decline in mortgage originations, they will be more likely to lend to creditworthy borrowers who have less than perfect credit, borrowers who currently find it difficult to obtain a mortgage.

This happened in 2000, the last time there was a major rate increase. Interest rates in 2000 were, on average, close to 100 basis points (or 1 percent) higher than in 1999 or 2001. Volumes plummeted, but credit access expanded. The combined loan-to-value ratios on full-documentation, fully amortizing Freddie Mac loans increased 1.2 percent (from 77.6 percent in 1999 to 78.8 percent in 2000), and the original debt-to-income ratios increased from 33.2 percent in 1999 to 35.2 percent in 2000. - Risk transfer innovations could slow. The Federal Housing Finance Agency requires that Fannie Mae and Freddie Mac transfer some of the credit risk on at least 90 percent of the targeted securities. To date, Fannie Mae and Freddie Mac have used back-end credit-risk transfer deals to off-load this risk, selling the risk after it is already on their books. As we and others have suggested, the Federal Housing Finance Agency is considering heavier use of front-end deals in which the risk is sold before the mortgage security is created. Unfortunately, the dwindling volumes we anticipate could easily slow this initiative.

-

The mortgage-lengthening effect of three factors could push mortgage rates even higher. Factors that cause homeowners to retain their mortgages longer could turn mortgage-backed securities into longer-duration instruments. These longer-duration instruments would need to be absorbed by the market, which is the equivalent of issuing more bonds—a move that will increase rates overall.

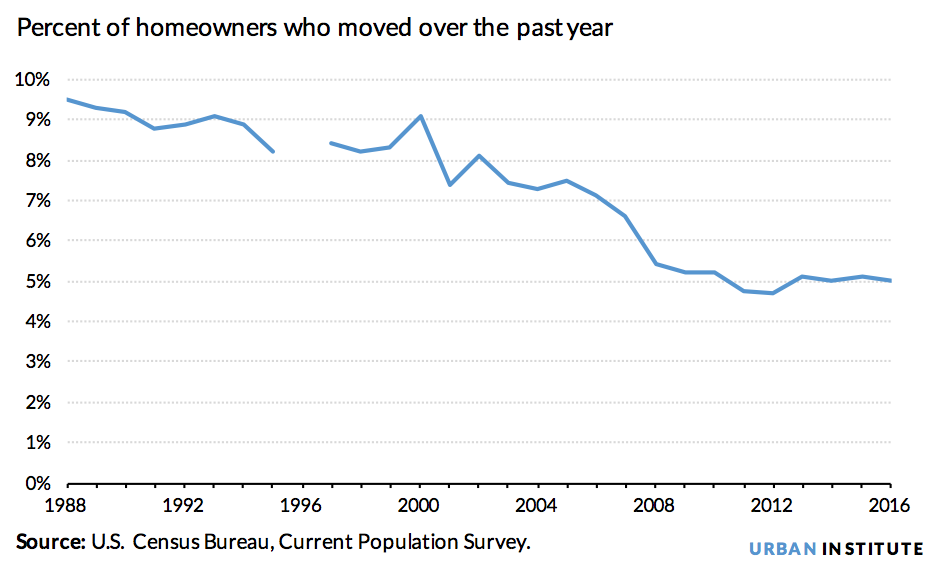

Three factors could lengthen mortgages: a significant decline in the homeowners’ geographic mobility (which has been happening since the early 1980s), the decline in refinancing (point 1), and the decline in trade-up activity (point 4). No model adequately accounts for this phenomenon.

Rates are up because the market anticipates increased spending

Market prices reflect investors’ beliefs about the future; investors today think overall spending will increase, causing prices and interest rates to rise. The market is likely expecting the Trump administration to spend more on infrastructure and anticipating potential increased consumer spending if the new administration’s promised tax cuts materialize.

Higher prices will increase inflation, which will push up interest rates. In addition, Treasury must issue more debt to generate capital for the promised spending, putting further upward pressure on interest rates.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.