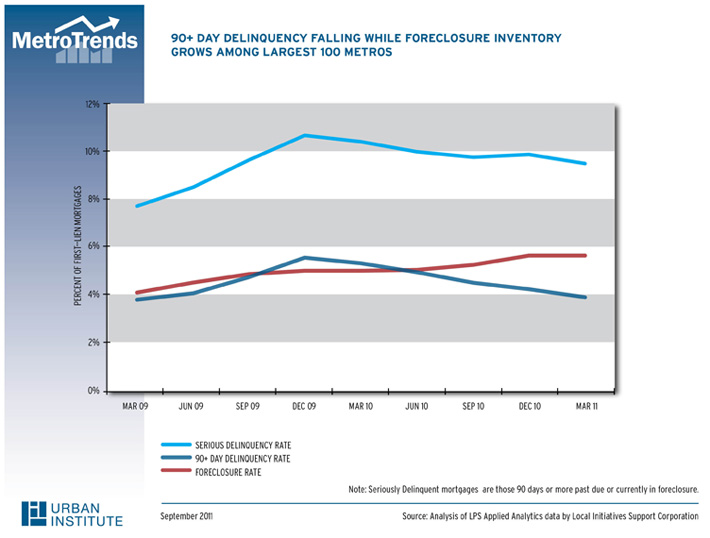

Serious mortgage delinquency rates continue to stabilize in the largest 100 U.S. metros, but remain historically high. Rates dropped about 10 percent from the peak in December 2009 to March 2011. As this chart shows, two dimensions of serious delinquency – the 90+ day delinquency rate and the share of mortgages in foreclosure – are now moving in opposite directions. The 90+ day delinquency rate fell from 5.5% in December 2009 to 3.9% in March 2011, and the share of all mortgages at least 30 days past due is also falling. Meanwhile, the foreclosure rate increased 12%.

90+ Day Delinquency Falling while Foreclosure Inventory Grows Among Largest 100 Metros

{kind=link}

LPS Applied Analytics’ Mortgage Monitor presentations indicate that the number of new foreclosures has been relatively flat, suggesting that properties are not being sold or subjected to either loan modification or alternate resolution. Instead, mortgages are lingering in foreclosure for long periods. Just how long depends on such factors as whether the property is in a state where courts get involved, whether the law specifies voluntary or mandatory mediation, and how servicers’ and lenders’ move properties through foreclosure.

Faster foreclosure, usually in states where courts don’t get in the act, may help stabilize neighborhoods if properties are quickly reoccupied. The downside of a speedy process is that it doesn’t allow homeowners enough time to work out loan modifications or negotiate short sales. Homeowners whose circumstances change – often, an unemployed borrower finding work and once again being able to make mortgage payments – have more opportunities to save their homes in states where foreclosure takes longer.

Unfortunately, there’s no easy way to strike a balance between a short and a long foreclosure process. But continued support for housing counselors would help borrowers navigate delinquency and foreclosure. So would further improvements by lenders and mortgage servicers in their loan-modification procedures –especially speeding up the negotiation of short sales or other graceful exit options.

For the complete data analysis on serious delinquency see the commentary. For data on all 366 metropolitan areas visit Foreclosure-Response.org.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.