<p>Photo via Shutterstock</p>

Despite skepticism by many advocates, the Federal Housing Administration (FHA) and Fannie Mae and Freddie Mac (the government-sponsored enterprises, or GSEs) increasing rely on auctioning off severely delinquent mortgages to private investors to dispose of these distressed assets. In January, we showed that sales of distressed or nonperforming loans (NPLs) have been effective from the borrowers’ and taxpayers’ perspectives, but these conclusions were based on limited data. Over the past few weeks, the FHA and the GSEs’ regulator, the Federal Housing Finance Agency (FHFA), have released new, more complete data, which allow us to confirm that this program significantly cuts foreclosures rates and is a win-win for borrowers, lenders, and investors.

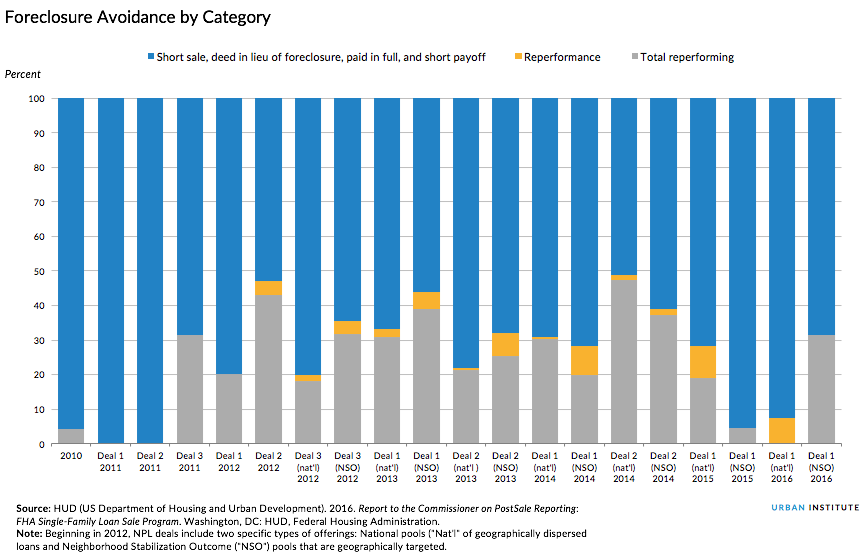

FHA loan sales significantly reduce foreclosures

The latest FHA report details the outcomes of investor sales and reveals that 67 percent of the loans have been resolved and nearly 42 percent of the resolved loans have avoided the worst outcome for all parties: foreclosure.

These loans are on average 28 months delinquent when investors purchased them, and the servicers have exhausted every loss-mitigation option available through the FHA. Had the loans remained in the US Department of Housing and Urban Development’s portfolio, they would have resulted mostly in foreclosures.

Focusing on resolved loans in these investor deals tells us the likely outcome of the lengthy resolution process. The loans in the deals completed from 2010 to 2013 are mostly resolved, but loans from more recent deals are still mostly in the delinquent servicing process.

Twenty-eight percent of the 104,000 resolved and unresolved loans in the 13 deals completed to date have avoided foreclosure through one of the six ways listed below, 37 percent have been foreclosed upon, and 3 percent are being held for rental. The balance, 33 percent of the loans, remains delinquent, awaiting resolution. This is not surprising, as 4 of the 13 completed FHA deals occurred between 2014 and 2016 and consist mostly of unresolved loans.

The report tracks six ways that a loan can be resolved without foreclosure:

- Reperformance: the borrower begins paying the loan again

- Forbearance: the lender allows the borrower to stop paying for a period

- Short sale: the property is sold for less than is owed, and the lender forgives the remaining debt

- Deed in lieu of foreclosure: the borrower gives the lender the deed to the house and forgives the outstanding debt

- Paid in full: the borrower sells the home and pays the full amount owed to the lender

- Short payoff: the borrower sells the property for less than is owed to the lender and agrees to pay the remaining amount owed to the lender either over time on in a lump payment.

Almost one-third of FHA loans that avoid foreclosure get back on track

Most encouragingly, the loans sold to investors that avoid foreclosure often get back on track. While deals vary, borrowers have begun paying again, or reperforming, on 32 percent of the loans, mostly thanks to loan modifications. Short sales (33 percent) and deeds in lieu of foreclosure (29 percent) were the two most-commonly used foreclosure alternatives.

FHA’s NPL sales save taxpayers an additional $16,000 per loan

These sales save taxpayers money as well. According to the latest FHA report, 104,259 nonperforming loans were auctioned off from 2010, the program’s inception, to 2015. The Mutual Mortgage Insurance Fund’s Actuarial Report reveals that NPL sales have gone from less than 1 percent of FHA dispositions in 2010 to 15.9 percent in 2015, resulting in savings to taxpayers of $2.4 billion, approximately $16,000 per loan above what would have been collected otherwise. Approximately $2.2 billion of these savings was generated since mid-2012, when the NPL sales program was made permanent and renamed the Distressed Asset Stabilization Program.

FHFA data also show reduced foreclosures

Similar results are apparent from the FHFA release. Because Freddie Mac and Fannie Mae did not sell many loans before 2015, only 31 percent of the 25,612 NPL sales that settled by the end of 2015 were resolved by the end of June 2016. The results for the resolved loans were strong: 16 percent were resolved without a foreclosure, and 15 percent were foreclosed upon. Loans that were less delinquent at the time of sale performed better than their more delinquent counterparts, emphasizing the importance of early intervention to avoid foreclosure.

The comparison between loans that remained with the FHFA and loans sold to investors is the most instructive: 29 percent of the NPLs that had been with the new servicers the longest (14 months) avoided foreclosure, compared with 19 percent of the NPLs that were not sold. And fewer of the sold NPLs were foreclosed upon: 26 percent versus 30 percent of the benchmark. These results are especially dramatic considering that the loans that were sold were more delinquent and had a higher loan-to-value ratio than the loans that were not sold.

The evidence from the FHA and FHFA is unequivocal: loan sales programs are highly valuable to taxpayers, borrowers, and investors. Selling troubled loans to investors brings better outcomes to borrowers, avoiding foreclosure more often than if the loans stayed with the agencies, and reaps greater profits for taxpayers.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.