The Federal Housing Finance Agency, the conservator of the government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, is currently considering what fee to charge lenders for Fannie and Freddie’s guarantee. The GSEs’ guarantee ensures timely payment of principal and interest to investors in mortgage-backed securities (MBS). Recent GSE deals that allow the private market to share credit risk provide the first clear indication of how the market prices this risk. This market pricing is significantly below the current guarantee fees (g-fees) charged by the GSEs—a critical benchmark that supports reducing the fees.

Risk-sharing experiments. When the GSEs issue fully guaranteed single-family MBS, they retain all of the risk associated with losses should the underlying mortgage loans default. To encourage private capital participation in the housing finance system and transfer some of this “credit risk” from the GSEs and taxpayers, the GSEs began sharing credit risk with the private market through a series of experimental transactions in July 2013. The risk sharing initiative was first outlined in 2012 in A Strategic Plan for Enterprise Conservatorships: The Next Chapter in a Story that Needs an Ending.)

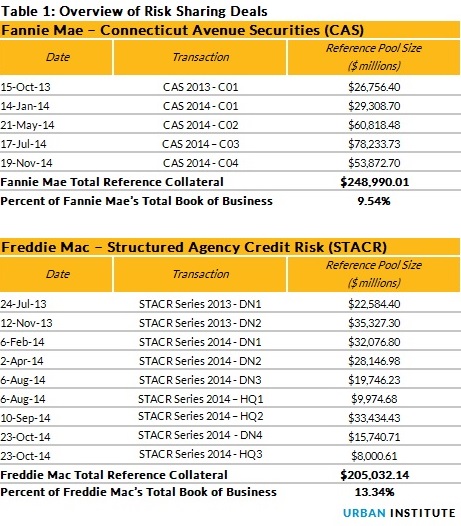

Freddie Mac’s first risk sharing Structured Agency Credit Risk (STACR) deal in July 2013 was followed by Fannie’s first deal -- Connecticut Avenue Securities (CAS) -- in October, 2013. While these early deals focused primarily on loans with very low loan-to-value (LTV) ratios, these deals have also included mortgages with LTVs over 80 percent since May 2014.

Through this initiative, the GSEs have laid off a significant amount of risk on $454 billion of loans. Freddie’s nine deals to date constitute 13.34 percent of its total outstanding book of business, and Fannie Mae’s five deals constitute 9.54 percent of its total book (see Table 1 and our monthly chartbook). A closer look at Fannie Mae’s most recent deal reveals how the private market prices the same credit risk the GSEs take, which in turn sheds some light on what would be reasonable for the GSEs to charge for taking comparable risk.

A deeper dive into Fannie Mae’s most recent deal: Fannie Mae’s November 19, 2014 Connecticut Avenue Securities deal (CAS 2014 C04) was backed by two groups of loans:

-

Group 1: Comprised of $35.8 billion worth of loans with LTVs greater than 60 and less than or equal to 80 percent. Fannie Mae retained the first 30 basis points (bps) of lifetime losses and sold two sets of notes to investors, with the 1M2 tranche bearing the losses before the 1M1:

- 1M1 tranches: Notes that take losses from 200 bps to 300 bps (a thickness of 100 bps). 1M1 sold at 195 bps over 1-month LIBOR.

- 1M2 tranches: Notes that take losses from 30 bps to 200 bps (a thickness of 170 bps). 1M2, the riskier of the two tranches, sold at 490* bps over 1-month LIBOR.

-

Group 2: Comprised of $18 billion worth of loans with LTVs greater than 80 percent. These loans must have mortgage insurance. Fannie Mae retained the first 65 basis points of lifetime losses and again sold two sets of notes to investors, with the 2M2 tranche bearing losses before the 2M1:

- 2M1 tranches: Notes that take losses from 255 bps to 375 bps (a thickness of 120 bps). 2M1 sold at 210 bps over 1-month LIBOR.

- 2M2 tranches: Notes that take losses from 65 bps to 255bps (a thickness of 190 bps). 2M2 sold at 500 bps over 1-month LIBOR.

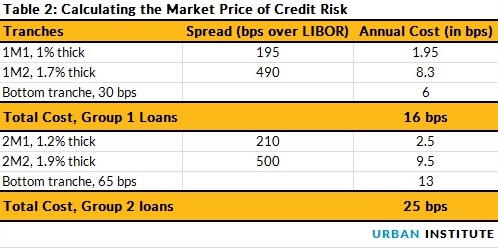

Calculating the credit risk: When an event that causes a credit risk occurs, such as a 180-day delinquency, deed-in-lieu, short sale, note sale, or REO sale, the loan is pulled out of the pool and a loss is registered at a pre-defined severity. Fannie retains the risk of losses that exceed 3 percent, and since these are 10-year notes, Fannie also retains any risk of losses after 10 years. The cost of this protection for the first 10 years (assuming the risk that losses will exceed 3 percent is near zero) is shown in Table 2.

Group 1 loans reveal a market-implied g-fee of 33 bps. To calculate the market-implied cost of credit protection, we multiply the thickness of each tranche by the spread, resulting in an implied cost for Group 1 loans of 1.95 bps on the 1M1 tranche, and 8.3* bps on the 1M2 tranche. We also take into account the cost of Fannie Mae’s retained 30 bps first loss position which we assume to be approximately 6 bps per year (by dividing the 30 bps g-fee by the assumed 5 year duration of the loans.)

Adding up all three tranches, the market has priced the credit protection for the lower risk, Group 1 loans at about 16 bps. Adding in the 10 bps payroll tax supplement and 7 bps in costs and expenses brings the market’s estimated guarantee fee to around 33 bps.

Currently,the g-fee charged by the GSEs on lower LTV borrowers with a similar FICO distribution is around 61 bps – nearly twice the 33 bps implied by the market. Although 33 bps may understate the cost slightly, as some losses will occur beyond 10 years, the out-year losses are likely to be very modest, increasing the cost minimally.

Group 2 loans reveal a market-implied g-fee of 42 bps. Adding up all the Group 2 tranches, the market has priced the credit protection for the higher risk Group 2 loans at about 25 bps. Adding in the 10 bps payroll tax supplement and 7 bps in costs and expenses brings the market’s estimated guarantee fee to around 42 bps. Again, this g-fee is significantly below the 61 bps g-fee charged by the GSEs currently on similar borrowers. Note that the g-fees are coincidentally the same for Groups 1 and 2 because while Group 2 loans have higher LTVs, the FICO distribution is similar and all Group 2 loans have mortgage insurance.

We do not take capital considerations into account because the impact is minimal. Taking them into account would increase costs only minimally. At the extreme, if the GSEs were not in conservatorship and laid off all risk, they would still need some working capital, but the cost would be quite small. If you assumed the GSEs need 10 percent capital against monthly cash payments (50 bps of unpaid principal balance), that would be 5 bps of capital. At a 10 percent rate of return, that would be 0.5 bps. But they have not laid off all risks and they retain the residual risk after 10 years, which would require capital that would need to earn a rate of return. This residual risk, however, is very small. The GSEs also retain the risk that losses during the first 10 years are greater than the protection provided by the credit risk transfer. This risk is remote, as the tranches are sized to withstand a 2007 scenario.

The bottom line. G-fees should be informed by what the market would charge. Judging by the market’s pricing of recent risk-sharing transactions, there is no reason to increase g-fees, and indeed, lowering them might well be appropriate.

* This post has been updated with two corrections. The spread of the 1M2 tranche is 490 bps over LIBOR, not 450 bps. The annual cost of this tranche is 8.3 bps, not 7.65 bps.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.