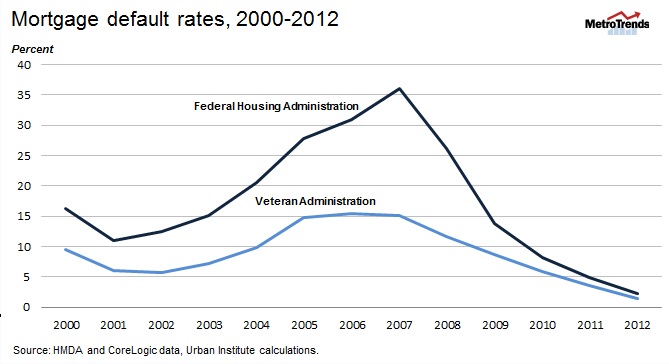

Default rates on loans guaranteed by Veterans Affairs (VA) are consistently lower than on loans insured by the Federal Housing Administration (FHA). For loans originated in 2007, the worst origination year, 36 percent of FHA loans have experienced at least one delinquency of 90 days or more, compared with only 16 percent of VA loans, as shown in the figure. These differences persist; for 2012 origination, the 2.3 percent FHA default rate was 64 percent higher than the VA’s 1.3 percent default rate.

While FHA and VA borrowers spend roughly the same percentage of their income on their mortgage payments, FHA borrowers have lower incomes and lower credit scores. When controlling for income and credit score, VA borrowers still have considerably lower default rates. For 2008 loans, for example, the default rate for FHA loans was 26.1 percent compared with just 11.6 percent for VA loans. But even if we apply VA borrower characteristics to FHA borrowers, the FHA default rate for 2008 loans would still have been 20.1 percent.

Why does the difference persist over time? In a commentary posted today, we looked at some possible explanations:

- Military culture – Could military culture or special incentives not to default, such as potential loss of a security clearance, cause a significant difference? Evidence is weak to support this theory and in 2013, only 17 percent of VA borrowers were on active duty when they took out their loan.

- Direct contact – The VA has a statutory requirement to service its borrowers and contact them directly. FHA does not engage in direct contact; the servicer contacts the borrower. As a result, the VA intervenes at an earlier point in a more uniform manner. While this might improve the likelihood that a delinquent loan reperforms, often referred to as the cure rate (it actually doesn't seem to), it is unlikely to explain the difference in the substantially higher rate at which FHA loans go 90 days delinquent.

- Skin in the game – Unlike the FHA’s 100 percent insurance, VA lenders remain on the hook for losses after the VA’s limited guaranty is exhausted. As a result, VA loans tend to be concentrated in lenders who are familiar with the VA’s special underwriting and servicing systems. We hope to explore FHA and VA default rates for lenders who originate both types of loans.

- Residual income test -- While the VA’s uses a residual income test and debt-to-income (DTI) guidelines to assess a borrower’s ability to pay, the FHA and conventional lenders rely exclusively on DTI. The residual income test measures whether a borrower will have enough money left after paying their mortgage and related expenses each month to meet unanticipated expenses. Although the expense side of the VA’s test has not been updated for years, and therefore probably understates the residual income a family actually needs, it works. For 2008 originations by borrowers with incomes under $50,000, the VA default rate was about 60 percent of the FHA default rate.

While adding a residual income test may cause some families to rethink or delay a home purchase or purchase a less expensive house, it also appears to be an effective way to reduce default rates and ensure borrowers take out mortgages they can afford. FHA and conventional programs should consider adding residual income to their underwriting. Moreover, lenders making higher cost Qualified Mortgages may want to consider using a residual income screen to provide more certainty that their borrowers can truly repay the loan.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.