A recent New York Times article discussed arguments for and against down payment requirements, which are currently being considered as a way to prevent foreclosures.

These proposed rules, though, could potentially widen the country’s sizeable wealth inequality gap.

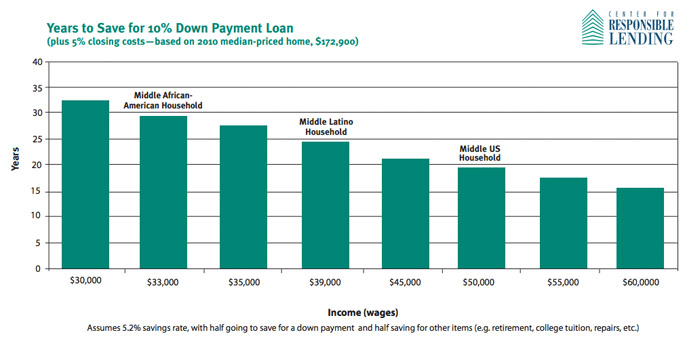

A 20 percent or even a 10 percent down payment requirement is likely to make homeownership difficult, especially for families with low and middle wealth or income, including many young families and families of color. The Center for Responsible Lending estimates that based on median incomes, it will take nearly 25 years for a typical Hispanic household to save for a 10 percent down payment loan and nearly 30 years for a typical African American household.

To make matters worse, black and Hispanic families are five times less likely to receive a large gift or inheritance—lump sums that can help families make down payments for homes and other assets. These disparities contribute to the racial wealth gap.

Homeownership is still the key wealth-building avenue for most Americans, so limiting access to mortgages could make wealth inequality worse. The power of homeownership as a wealth-building tool comes not primarily from the growing value of property but from automatic, monthly mortgage payments that are a form of savings and build equity.

Policymakers should consider the effects of tightening credit availability given new empirical evidence that younger generations are falling behind their parents in wealth building, the racial wealth gap is not improving, and delayed homeownership is the largest contributing factor to the racial wealth gap. The Federal Housing Administration can continue to fill the gap by insuring lower down payment loans, but do we really want two separate credit markets: one for families of color and another for white families?

We need to be careful not to overreact against homeownership for low-income families as a result of the foreclosure crisis. Homeownership can be done right for low-income families. Foreclosure rates for people who bought their homes through Individual Development Account programs—which provide savings incentives, pre-purchase counseling, and guidance in choosing affordable non-predatory products—were one-half to one-third the rate for other low-income homebuyers in the same communities. This and similar success stories tell us that the down payment is just one among many factors that contribute to successful low-income homeownership.

House image from Shutterstock. Graphic from Center for Responsible Lending.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.