On August 28, six regulatory agencies[i] released their long-awaited reproposal governing risk retention in securitizations under Section 941 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the Dodd-Frank Act). While the reproposal covers risk retention requirements for securities of many types, we focus here on mortgage-backed securities (MBS). Under Section 941, MBS that are backed by loans that are Qualified Residential Mortgages (QRMs) are not subject to risk retention, while most other MBS are[ii]. The proposal defines QRM and spells out the forms risk retention can take. Comments are due October 30.

Under the proposal, QRM would be set to the standards for a Qualified Mortgage (QM), as defined by the Consumer Financial Protection Bureau (CFPB).[iii] This is the broadest definition possible, as Dodd-Frank requires that QRM can be no broader than QM. The proposal also asked for comments on an alternative QRM definition (dubbed QM-Plus or Alternative QRM), which would, in addition to the QM standards, require a 30 percent down payment, limit second mortgages, require owner occupancy, and include restrictions on credit history. The agencies stated they were putting forth the alternative because they were concerned that “the effect of aligning QRM with QM could ultimately decrease credit availability as lenders, and consequently securitizers, would be very reluctant to transact in non-QM loans.”[iv]

In this article, we look at the portion of mortgage originations that would be exempt from risk retention if QRM were the same as QM, and the portion that would be exempt under Alternative QRM. We provide this information to enhance the ability of those reviewing the proposal to understand and comment on its implications.[v]

Results from the CoreLogic MBS/ABS Databases

QM requires:

- Full documentation

- No interest-only (IOs) or balloon payments

- No negative amortization

- Term of 360 months or less

- Back-end (all-inclusive) debt-to-income ratio (DTI) of 43 percent or less

- Prepayment penalties of three years or less[vi]

Click table to view larger version

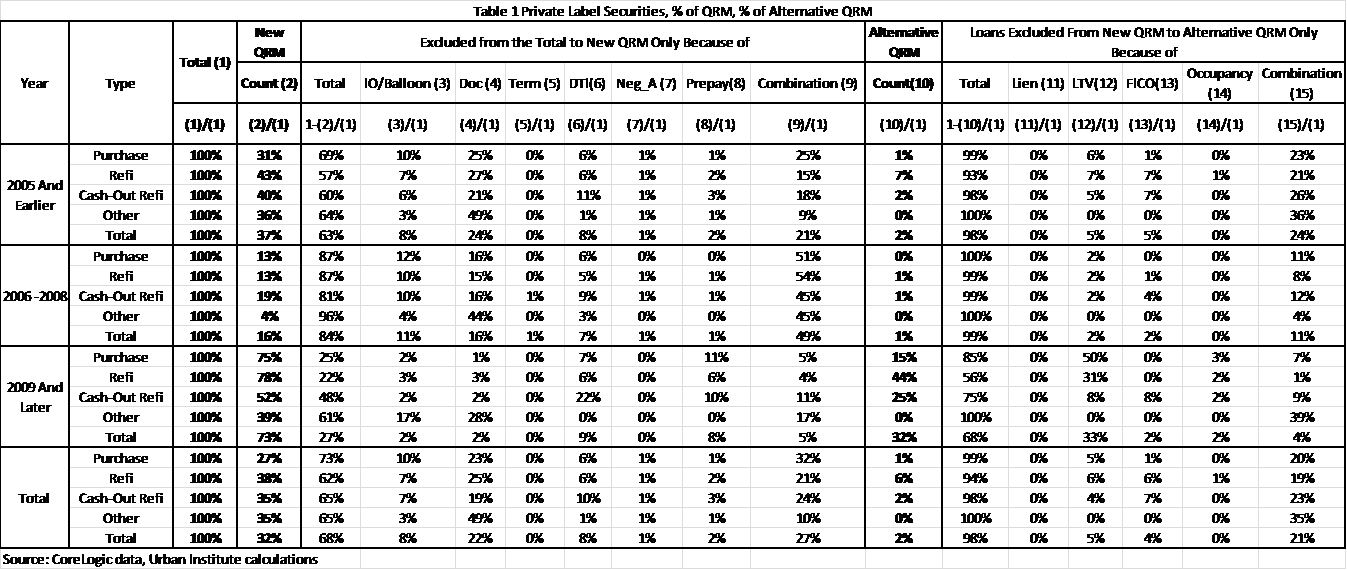

Table 1 shows the percent of loans in private label securities (PLS) that would be QRM eligible (exempt from risk retention) if QRM=QM, using the CoreLogic Securitized (MBS/ABS) databases. For convenience, we have divided the data into 2005 and earlier, 2006–2008, and 2009 and later.

For the 2005 and earlier originations, only 37 percent of the loans would be QM/QRM eligible, with the remaining 63 percent ineligible. Twenty-four percent of the loans were ineligible because they lack full documentation, another 8 percent due to DTI, 8 percent due to product features such as IO or balloon, and 21 percent due to a combination of risk factors. For the 2006–2008 period, only 16 percent of the loans would have qualified under the proposed QM/QRM standard. Of the remaining 84 percent, 16 percent were ineligible because they lacked documentation, 7 percent had a DTI above 43 percent, 11 percent had IO or balloon features, and 49 percent of the loans were not QM/QRM eligible due to a combination of risk factors (difference due to rounding).

For the 2009-and-later period, 73 percent of the loans are QM/QRM eligible. The most common reason for eligibility failure is DTI (9 percent), followed by prepayment penalties (8 percent), product features such as IOs and balloons (2 percent), documentation (2 percent) and a combination (5 percent). We believe that, had the QM rules been in effect, the prepayment penalty and IO/balloon features could have been eliminated to make these loans QM eligible, bringing the eligibility percentage to around 83 percent.

QM/QRM eligibility is slightly lower for purchase loans than for refinance (refi) loans. Over the total period, 27 percent of the purchase loans would have been QM/QRM eligible versus 38 percent of the refis and 35 percent of the cash-out refis.

The Alternative QRM definition is very restrictive. It starts with QM and then adds all of the following features:

- Loan to value ratio (LTV) of 70 or less

- First liens only; the first lien is disqualified if there is a second lien on a purchase loan

- Owner occupied only

- Credit history requirements: not currently 30 days past due on any debt, not 60 days past due on any debt in the past 24 months, no bankruptcy or foreclosure in the past 36 months.[vii]

If the Alternative QRM definition had been used, the portion of eligible PLS loans would have been very low—2 percent in the 2005-and-earlier period, 1 percent in the 2006–2008 period, and 32 percent in the 2009-and-later period, which consists of pristine origination. Recall that for the 2009-and-later period, 73 percent of the loans were eligible under the QM/QRM standard. Thus 68 percent of the 2009 and later PLS mortgage loans are not QRM under the Alternative QRM definition, with the breakdown as follows: 27 percent non-QM, plus 33 percent due to DTI alone, plus 2 percent due to FICO alone, plus 2 percent due to occupancy alone, plus 4 percent due to a combination of factors equals 68 percent. For the 2009-and-later period, while 32 percent of the overall PLS market is alternative QRM eligible, only 15 percent of the purchase loans qualify, compared with 44 percent of the refis and 25 percent of the cash-out refis.

Results from the Freddie Mac Loan-Level Database

It can be argued that prior to 2008, private label securities were adversely selected (the weakest loans went this route), and the PLS database is therefore not representative of the entire market. Moreover, as the Federal Housing Finance Administration shrinks the Fannie Mae and Freddie Mac (GSE) footprint by raising guarantee fees and possibly reducing loan limits, some GSE loans would be securitized into PLS, and could be affected by risk retention. Under the current QM rules (and QRM proposal), any mortgage that would qualify for GSE execution is assumed to be a qualified mortgage and not subject to risk retention. Under the Alternative QRM proposal, "loans that are QRM because they meet the CFPB’s provisions for GSE-eligible covered transactions, small credit or exceptions or balloon loan provisions would, however, not be considered QRMs under the QM-plus approach." If a loan is GSE eligible and sold to the GSE, there are no risk retention issues (the GSE is assumed to have retained risk by virtue of its guarantee). However, loans that are GSE eligible but in PLS securities would be subject to risk retention if they do not meet the Alternative QRM criteria.

In light of this, we examine Freddie Mac loan-level data to figure out how much of the universe would qualify under the QM/QRM standard, and how much of the universe would qualify under the Alternative QRM requirements.

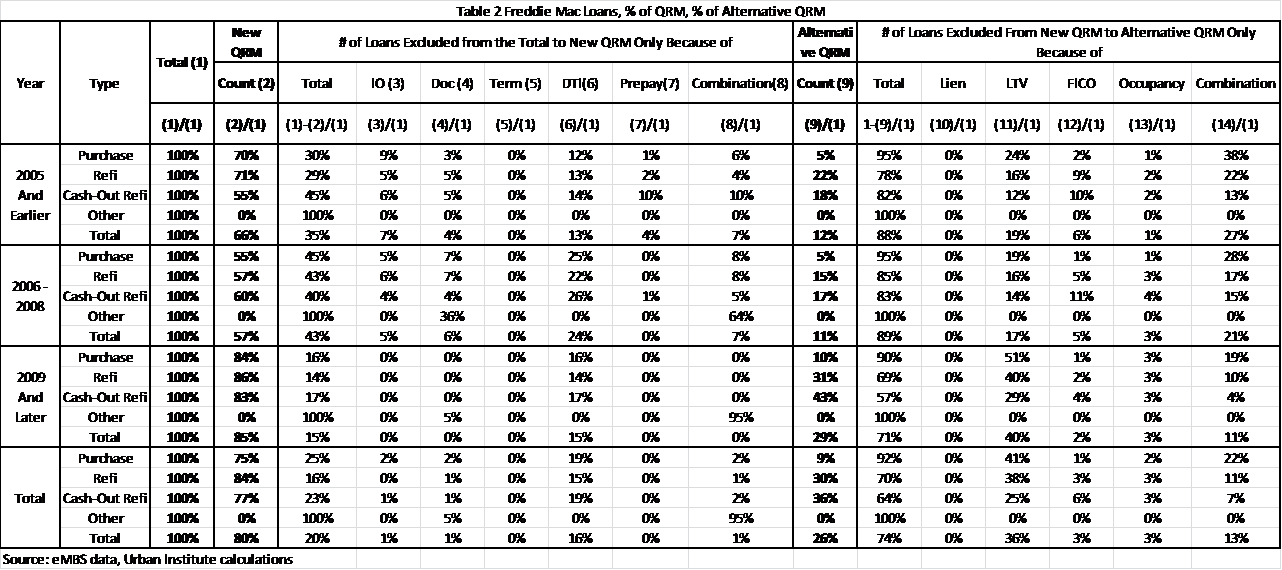

Freddie releases loan-level data on mortgages purchased in December 2005 and thereafter; the result of this analysis is shown in table 2[viii]. Our results indicate that 66 percent of the loans purchased in 2005 and earlier would have been eligible under the QM/QRM standard; in the 2006–2008 period, 57 percent were eligible. GSE lending became more pristine in 2009 and later, and 85 percent of the loans from this later period would have been eligible under the QM/QRM standard. All of the exclusions in the later period were due to DTI. For all periods, 75 percent for purchase loans qualify as QM/QRM, compared with 84 percent of refis and 77 percent of cash-out refis. For 2009 and after, the qualifying percentages are virtually identical for all types of loans.

Click table to view larger version

Comparing the Freddie loan-level data in Table 2 with the PLS data in Table 1, the Freddie data shows massively more loans qualifying in the early periods than does the adversely selected PLS data. For example, for the 2005-and-earlier period, 66 percent of Freddie loans would have qualified as QM/QRM, but only 37 percent of PLS; for the 2006–2008 period, 57 percent of Freddie loans would qualify compared with only 16 percent of PLS. However, from 2009 on, if one looks at the PLS data and adds back loans with product features that would not have been offered if the QM/QRM rules had been in effect (prepayment penalties and IOs/balloons), the portion of loans qualifying under the QM/QRM standard is approximately the same for PLS as for Freddie: 83 percent for PLS (73 percent QRM qualifying plus 8 percent due to prepayment penalty plus 2 percent due to IOs/balloons) compared with 85 percent for Freddie.

The number of Freddie Mac loans that would qualify under the Alternative QRM is very low: 12 percent of the 2005 and earlier loans, 11 percent of the 2006–2008 loans, and 29 percent of the 2009 and later loans. And while 29 percent of the total loans from the 2009 and later period would qualify under the Alternative QRM, only 10 percent of the purchase loans would do so. The largest single cause of a failure to qualify under the Alternative QRM was LTV.

Results from the Prime Servicing Database—GSE Loans

Click table to view larger version

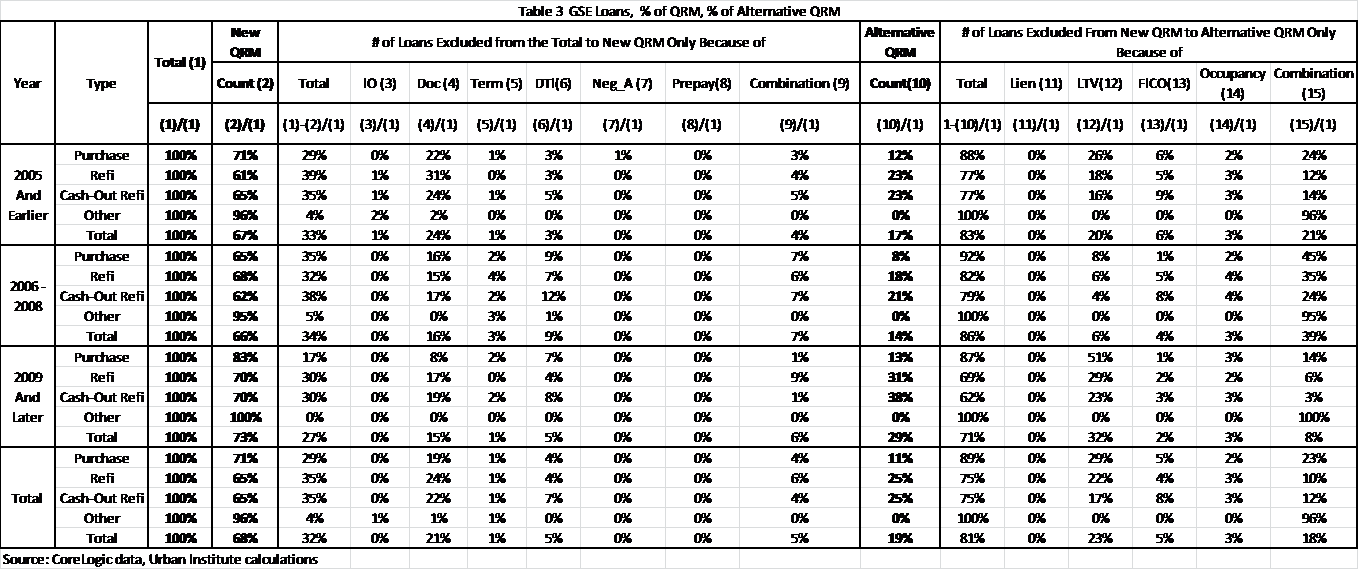

One can argue that the Freddie Mac database does not adequately represent loans originated prior to 2006. Moreover, we have not included Fannie Mae at all. To show that these omissions do not substantially change the conclusions, we look at GSE loans in the CoreLogic Prime Servicing Database. This database covers more than 130 million active and closed loans from the largest servicers. Table 3 shows that 67 percent of the loans in the 2005-and-earlier period qualified under the QM/QRM standard, as did 66 percent in the 2006–2008 period and 73 percent in the 2009-and-later period. These numbers are similar to those in the Freddie loan-level database. For the entire period, 71 percent of purchase loans qualified, compared with 65 percent of refi loans. This reflects the fact that the servicers contributing to the Prime Servicing Database are the largest servicers, who account for an outsized portion of the Home Affordable Refinancing Program refinancings. Like many streamlined refis, the documentation on many of these loans would not be QM qualifying.

The portion of GSE loans that qualify for the Alternative QRM proposal is consistent between the Freddie loan-level database and the GSE loans in the prime servicing database. It was very low in the pre-2009 periods (17 percent in 2005 and earlier, 14 percent in 2006–2008), and a still small 29 percent from 2009 on. Purchase loans are much less likely to qualify for Alternative QRM than refinance loans. For 2009 and on, only 13 percent of the purchase loans qualify (versus 29 percent for all).

Results from the Prime Servicing Database—Bank Portfolio Loans

Click table to view larger version

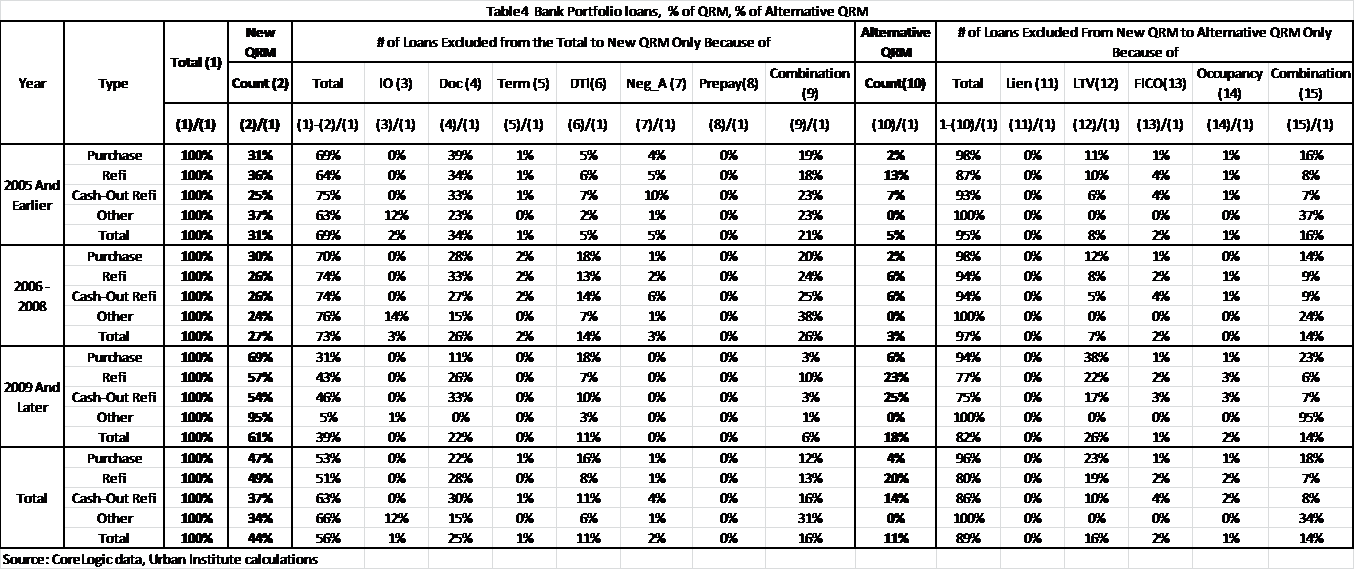

Banks have the option to securitize the loans in portfolio, so we do the same analysis for bank portfolio loans as we have done for the GSE and the PLS markets. The result of this analysis is shown in table 4. We would expect that banks have greater flexibility to consider compensating factors on portfolio loans hence a lower proportion of these loans to qualify under the QM/QRM rule than would be the case for GSE loans. Our results bear that out: 31 percent of the loans in the 2005-and-earlier period qualified under QM/QRM, 27 percent in the 2006–2008 period and 61 percent and the 2009-and-later period. These numbers, shown in table 4, are quite a bit lower than for the GSE loans. Especially for the most recent period, banks likely could have resolved the documentation problems that disqualified some refis.

Only 5 percent of the bank portfolio loans originated in the 2005-and-earlier period qualified under the Alternative QRM criteria; it was 3 percent for the 2006–2008 period. Eighteen percent of the bank portfolio loans would have qualified under Alternative QRM for the 2009-and-later period—but only 6 percent of purchase loans.

Conclusion

We have looked at the number of loans that are QRM eligible from a number of different sources: PLS data, Freddie loan-level data, and CoreLogic Prime Servicing data for three separate periods: 2005 and earlier, 2006–2008, and 2009 and later. A few elements are common to all the results:

- In the earlier periods, fewer loans, regardless of the source, were QM/QRM eligible than in the 2009-and-later period. In the later period, the overwhelming majority of the loans qualify for QM/QRM.

- Very few loans qualify under the Alternative QRM definition. If the alternative definition were adopted, the vast majority of loans would require risk retention, making these loans more expensive.

- The portion of purchase loans that qualify for Alternative QRM is even smaller than the total portion of loans qualifying; few purchase borrowers can make a 30 percent down payment.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.