<p>James Leynse/Getty Images</p>

On November 10, the US Supreme Court will hear oral arguments in the California v. Texas case. In this case, a group of state attorneys general, led by the Texas attorney general, argues that the entire Affordable Care Act (ACA) is now unconstitutional because of a 2017 tax law that eliminated the ACA’s individual mandate penalties beginning in plan year 2019. Their effort is supported by the Trump administration, and it is being fought by a group led by the California attorney general.

In our recent analysis, we found if the Supreme Court overturns the ACA, an additional 21.1 million people nationwide would be uninsured in 2022. We also found the following consequences of eliminating the ACA:

- 9.3 million people would lose income-related subsidies for marketplace insurance in 2022;

- Medicaid and Children’s Health Insurance Program coverage would decline by 15.5 million people in 2022; and

- federal government spending on health care would fall by $152 billion per year in 2022.

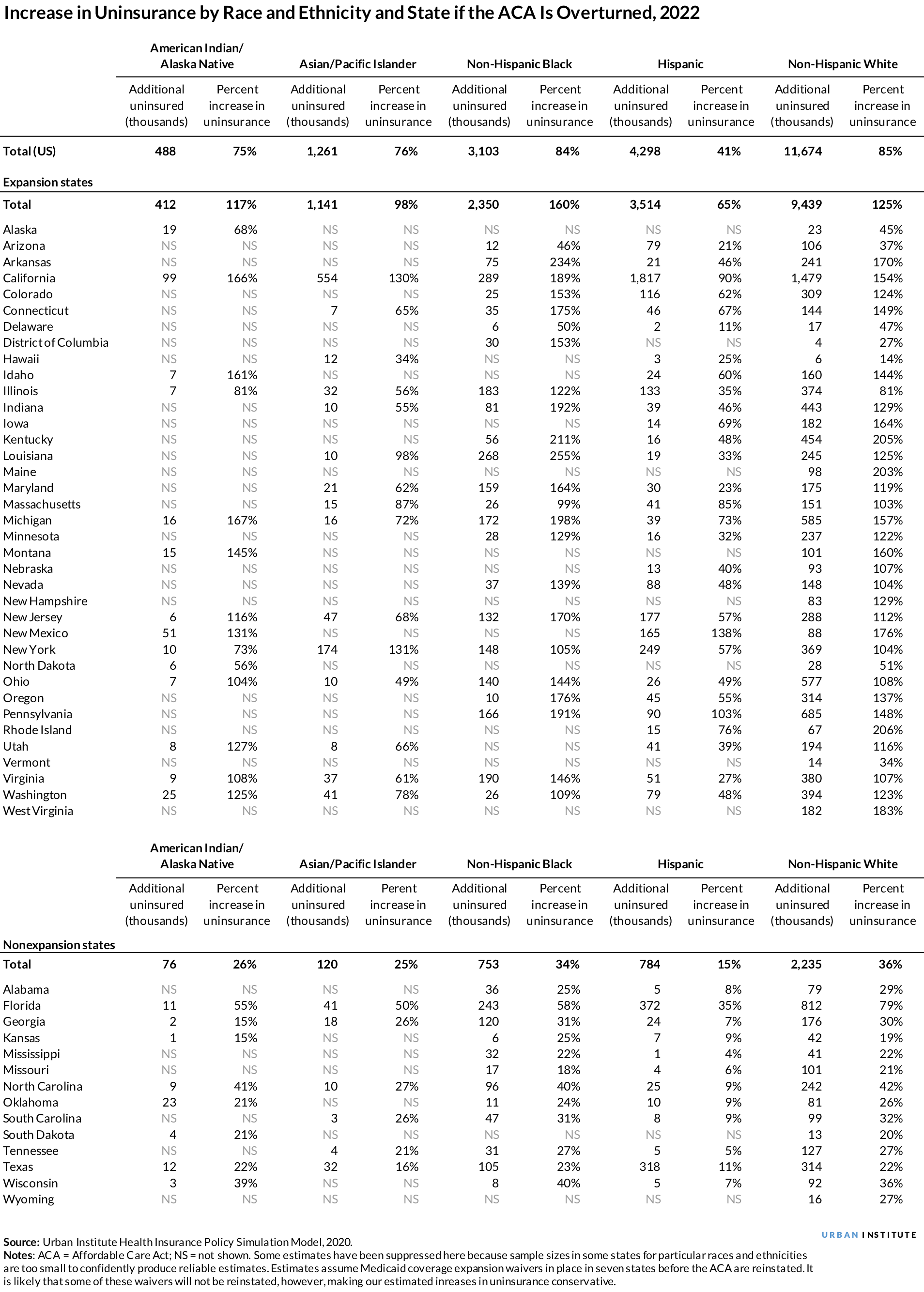

Based on this study, we produced additional, state-level estimates of the effects on coverage by age group (table 1) and race and ethnicity (table 2) if the ACA is overturned. Full data tables with additional elements not shown in these tables are downloadable separately. Some of our key findings for 2022 include the following:

- Invalidating the ACA will increase uninsurance among the nonelderly in every age group. Children ages 18 and younger will feel the smallest effect because their pre-ACA eligibility for public insurance coverage (through Medicaid and the Children’s Health Insurance Program) is greatest. Still, 1.7 million more children will be uninsured, an increase of 48 percent. Adults ages 50 to 64 will experience a 95 percent increase in uninsurance, an additional 5.6 million people. And 4.9 million young adults ages 19 to 26 will be uninsured, a 76 percent increase compared with current law. Adults ages 27 to 49 will experience a 60 percent increase in uninsurance, 8.8 million more uninsured.

-

States experiencing the largest coverage gains under the ACA will experience the largest increases in the uninsured. These states include those that expanded Medicaid eligibility under the law, those with high enrollment rates in the ACA-subsidized Marketplaces, and those that had high uninsurance rates before implementation of the law.

For example, Pennsylvania and Michigan are among the most populous states that will have the largest percent increases in the uninsured if the ACA is overturned. In Pennsylvania, the uninsurance rate among young adults will climb by more than 170 percent (to 27 percent uninsured). For adults ages 27 to 49, the uninsurance rate will increase by 152 percent (to 20 percent uninsured), and for adults ages 50 to 64, by 154 percent (to 16 percent uninsured). In Michigan, the uninsurance rate for young adults will increase by nearly 200 percent (to 31 percent uninsured), by more than 150 percent for adults ages 27 to 49 (to 23 percent uninsured), and by 148 percent for adults ages 50 to 64 (to 18 percent uninsured).

Among states that have not expanded Medicaid eligibility, Florida will experience the largest increases in the uninsured in both absolute numbers and percentage terms because the state has high enrollment in the ACA Marketplace. In Florida, the insurance rate among young adults will increase 35 percent (to 36 percent uninsured). For 27-to-49-year-olds, it will increase 52 percent (to 30 percent uninsured), and for 50-to-64-year-olds, it will increase 89 percent (to 25 percent uninsured). - People of all races and ethnicities will experience large increases in uninsurance. Again, the largest increases across races and ethnicities will occur in states that expanded Medicaid eligibility under the law. In 10 states with sufficient sample sizes to measure the effects (Michigan, California, Idaho, Montana, New Mexico, Utah, Washington, New Jersey, Virginia, and Ohio), uninsurance rates will more than double among American Indians and Alaska Natives. In Louisiana, Kentucky, Michigan, Indiana, and Pennsylvania, uninsurance rates for non-Hispanic Black people will nearly triple or more. Uninsured non-Hispanic white people will more than double in number in 29 states. Uninsurance among the Hispanic population will more than double in Pennsylvania and New Mexico.

- States that did not expand Medicaid eligibility under the ACA stand to lose somewhat less coverage, but uninsurance will still increase substantially among people of all races and ethnicities. Across all nonexpansion states combined, uninsurance among American Indians and Alaska Natives will increase 26 percent (to 23 percent uninsured). Among Asian and Pacific Islander populations, uninsurance will increase by 25 percent (to 21 percent uninsured). Among non-Hispanic Black people, uninsurance will increase by 34 percent (to 19 percent uninsured). The number of uninsured Hispanic people will increase 15 percent in these states (to 33 percent uninsured). Uninsurance among non-Hispanic white people will increase 36 percent (to 15 percent uninsured), and uninsurance among other races and ethnicities will increase by 28 percent (to 14 percent uninsured).

If the Supreme Court overturns the ACA in California v. Texas, coverage will fall considerably in every state and within every age group and across people of all races and ethnicities. And as we have estimated previously, federal spending on health care will fall in every state, and health care providers—hospitals, physicians, prescription drug manufacturers—will experience sizable decreases in revenue. The gains in access and affordability of care and improvements in health status achieved by the ACA that have been documented by an array of research will be reversed.

However, the implications of the law being invalidated have far greater reach than we can estimate, because virtually all insurers, providers, and households across the country have been affected by the law’s many provisions. Policymakers have straightforward legislative options that could protect the ACA as it is operating under current law if they are passed before the court issues its decision; thus far, Congress has not passed bills to do so.

Full data tables with additional elements not shown in these tables are downloadable separately.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.