Policymakers count on a wide range of measures to gauge the state of the housing and mortgage markets, but when it comes to the availability of credit, are we as precise as we can be?

Given the many recent steps to increase access to mortgage lending, credit availability is at the center of housing finance policy discussions. But measuring access to credit is complicated. Traditional measures of credit availability, such as median credit scores or standard denial rates, are incomplete, unreliable, or lack historical accuracy. On January 6, the Urban Institute’s Housing Finance Policy Center convened a panel of experts to discuss three promising new indices that provide a robust measurement of credit availability.

Three ways to better measure credit availability

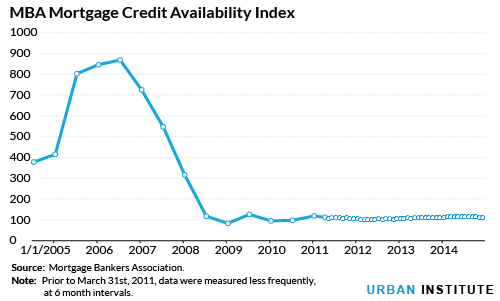

1.)Mortgage Bankers Association’s Mortgage Credit Availability Index. “This Index was developed out of frustration,” Michael Fratantoni of the Mortgage Bankers Association (MBA) noted, speaking of his organization’s Mortgage Credit Availability Index (MCAI). The MCAI relies on AllRegs Market Clarity Data to measure the quality and quantity of credit offered by wholesale lenders over time. More specifically, it measures the types and quantities of “loan programs,” a blend of underwriting criteria and credit standards offered each month by nearly 100 of the largest mortgage investors, including Freddie Mac and Fannie Mae, the Federal Housing Administration, mortgage insurance companies, and other large, medium, and small investors. Indexed to March 2012, with complete data back to March 2011, and a sampling of data points back to 2004, the MCAI picks up changes in lender behavior in a timely manner in both the government and conventional markets. As a result, Fratantoni noted, one of the strengths of the MCAI is “you know how lenders are responding to policy.”

2.) CoreLogic’s Housing Credit Index. Alternatively, the lender response can be measured by the size of the credit box, which CoreLogic’s Housing Credit Index (HCI) estimates. The HCI measures variability in underwriting using a 5 percent sample of the CoreLogic Prime and Subprime Servicing database, or about 1.5 million first-lien originations. As Sam Khater of CoreLogic explained, the multidimensional metric, which is captured through a principal components analysis, traces the relative size of the credit box based on loans from about the top 30 servicers, capturing about 80 percent of the market outside of portfolio loans. The HCI is benchmarked to January 2000, and uses monthly data thereafter.

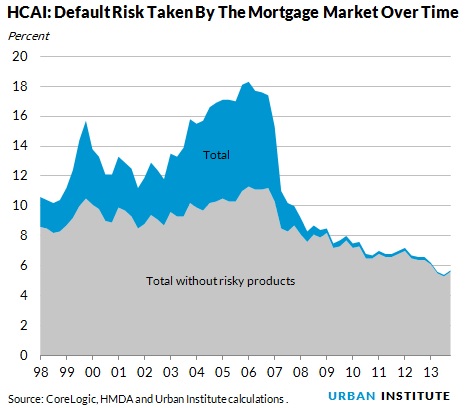

3.) Housing Finance Policy Center’s Credit Availability Index. Recognizing the complexity of directly measuring the credit box, the Housing Finance Policy Center’s Credit Availability Index (HCAI) instead measures the amount of anticipated default risk taken by the market at origination for any group of loans. The underlying concept, according to Wei Li of the Urban Institute, is that the market expands credit availability by taking more default risk, and vice versa. To determine the default risk of any set of home purchase loans, the HCAI compares the characteristics of the loans of interest against a database of historic loans divided into 360 buckets. Each loan of interest is assigned to one of the 360 buckets that vary by borrower characteristics (credit score, loan-to-value, debt-to-income ratio, income documentation) and loan risk, separating loans with and without risky features (less than 5 years to reset, interest-only loans, negatively amortizing loans).

The default risk of each of these buckets of loans under normal economic conditions equals the actual default rate of the same bucket of loans originated in 2001 and 2002. Similarly, its default risk under stressed economic conditions equals the actual default rate of the same bucket of loans originated in 2005 and 2006. HCAI for any vintage of loans equals the vintage’s default risk under the normal condition weighted by 90 percent plus the vintage’s default risk under the stressed condition weighted by 10 percent. By weighting both product risk and borrower risk, the HCAI allows an unexplored aspect of credit availability to be revealed: how much of the risk is caused by borrower characteristics and how much by product characteristics.

Immediate policy considerations

All three indices represent significant contributions to the problem of measuring credit availability, and each has important policy implications. Noted Fratantoni, with a quick look at the MCAI one can “point to… changes in lending patterns” in response to policy initiatives, such as when lenders pulled back on ARM programs in anticipation of the January 2015 implementation of the Consumer Financial Protection Bureau’s Qualified Mortgage rule. Similarly, a graph of the HCAI over the last 17 years makes it clear that product risk, not borrower risk, fueled the housing crisis and that lenders today are only taking two-thirds of the borrower risk they consistently maintained in the pre-bubble and bubble years—a tremendous over-correction.

With further changes (a growing jumbo market, higher LTV programs, lower FHA premiums) on the horizon, these indices will allow us to more closely track the success of attempts to expand access to credit and widen the exceptionally tight credit box shown in all three indices—and to make course corrections with new and better information.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.