<p>The New Hampshire State House in Concord. Photo by Ritu Manoj Jethani via Shutterstock.</p>

New Hampshire is moving forward with implementation of its work and community engagement requirements in Medicaid, which were approved by the Centers for Medicare & Medicaid Services in 2018. Like those in Kentucky and Arkansas, which were blocked by a federal judge in March 2019, New Hampshire’s Medicaid work and community engagement requirements are being challenged in court.

We assessed potential access to employer-sponsored insurance (ESI) coverage among New Hampshire residents who could lose Medicaid coverage because of the new requirements. Many would likely face limited and costly employer-sponsored health insurance options.

Fewer than 1 in 10 part-time private-sector employees in New Hampshire were eligible for employer-sponsored coverage and just over half (55.0 percent) of full-time employees at firms with fewer than 50 employees were eligible for employer-sponsored coverage in 2017. On average, annual employee contributions for a single-coverage plan would represent 12.5 percent of annual income for a minimum-wage, full-time worker and 25.0 percent of annual income for a minimum-wage, part-time worker—above the 2.04 percent premium limit in the Marketplace for individuals earning 100 percent of the federal poverty level.

These findings are consistent with our earlier analyses, which found low levels of eligibility for ESI among part-time workers and high employee contributions for ESI plans in Kentucky and Arkansas.

To comply with the New Hampshire work and community engagement requirements, nondisabled adult Medicaid enrollees, including parents of children ages 6 and older, must either meet an exemption or complete and report at least 100 hours of qualifying activities per month. A person's eligibility is suspended after two consecutive months of noncompliance.

How accessible is employer-sponsored insurance?

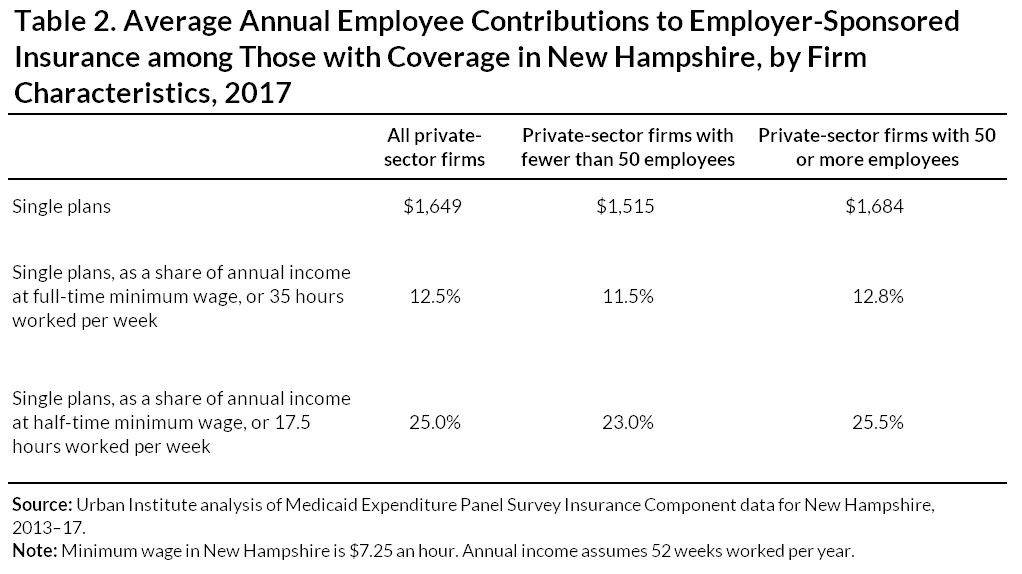

We used 2017 information from the Medical Expenditure Panel Survey Insurance Component to assess potential access to and affordability of ESI from a sample of 416 private-sector employers in New Hampshire (we present additional data from 2013–16 and flag one estimate with a high relative standard error in the notes below table 1).

To substitute employer coverage for lost Medicaid coverage, employees would need to receive a health insurance offer from their employer, be eligible for that coverage, and be able to afford any required premium contribution. In New Hampshire, 88.6 percent of full-time employees and 70.6 percent of part-time private-sector employees worked at a firm that offered health insurance in 2017.

But among firms that offer insurance, not all employees are eligible for that coverage, based on factors such as hours worked or length of employment. In 2017, only 5.9 percent of part-time private-sector employees in New Hampshire were eligible for ESI, compared with 81.5 percent of full-time private-sector employees. Eligibility rates for full-time employees were lowest at small firms (55.0 percent in 2017).

According to 2015 data, a little more than one in six private-sector employees in New Hampshire worked at a firm with 20 or fewer employees.

How affordable is employer-sponsored insurance?

For workers who are eligible for ESI, the required employee premium contribution will be a key factor in determining the affordability of that coverage.

On average, annual employee contributions were $1,649 for single-coverage plans, representing 12.5 percent of the annual income of a full-time worker (35 hours per week) earning minimum wage. A minimum-wage employee who works part time (17 hours per week) would have to pay 25.0 percent of his or her annual income to remain insured, provided the firm did not prorate the employer contribution to align with hours worked. If the employer contribution were prorated, the employee contribution would increase further.

These shares exceed the Affordable Care Act’s Marketplace premium limits of 2.04 percent of income for people earning 100 percent of the federal poverty level and 4.08 percent of income for people earning 150 percent of the federal poverty level—a range that includes full-time minimum-wage workers in New Hampshire.

Our analysis shows that working Medicaid enrollees in New Hampshire who fail to meet the 100-hours-a-month work and community engagement reporting requirements would have limited ESI options.

Very few private firms in New Hampshire offer employer coverage to part-time employees, and qualifying for an offer of employer coverage could also prove difficult for full-time workers, particularly at small firms.

Obtaining employer coverage would be out of reach for many Medicaid enrollees who would be eligible for such coverage. Employee contributions toward premiums would constitute a larger share of income on average than deemed affordable under the Affordable Care Act.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.