As we seek to reform the housing finance system, we must clearly understand how well the market is providing access to mortgage credit for those who need it. Yet, the four most commonly used measurements of credit availability suffer variously from being too narrow, too subjective, limited in time, opaque, or inaccurate in certain situations.

A new measure of mortgage credit availability

The Housing Finance Policy Center’s new measure—the Credit Availability Index (HCAI)—improves upon existing measures by precisely calculating how much default risk the market is taking at any given point. The HCAI is robust, objective, and intuitive because it weights the likelihood of economic downturns, and takes several borrower and loan characteristics into account. It is also completely transparent. These features make it a powerful tool that can help policymakers better understand the housing finance environment and develop policies to support a healthy housing system.

How does it work?

To determine the default risk of a newly originated home purchase loan, the HCAI probes an enormous database of historic loans to find the set of loans that most closely match the characteristics of the loan of interest. The characteristics used for matching the new loans with the historic loans include borrower characteristics (credit score, loan-to-value, debt-to-income ratio) and loan risk, separating loans with and without risky features (less than 5 years to the reset, interest-only loans, negatively amortizing loans).

The HCAI searches for and uses two historic default rates to determine the likely default risk of a newly originated loan:

- Normal-year default rate: The actual default rate of historic loans with similar characteristics originated in a year followed by normal economic conditions (2001 and 2002). A default is defined as a seriously delinquent (90-plus days) payment, including various stages of foreclosure.

- Stressed-year default rate: The actual default rate of historic loans with similar characteristics originated in years followed immediately by economic stress (loans originated in 2005 and 2006).

The HCAI then weights these two default rates according to the likelihood of normal or stressed scenario, assigning a 90 percent chance for a normal economic environment and a 10 percent chance for a stressed economic environment. The resulting number is the expected default risk the market takes in making this new loan or group of loans.

What does the HCAI tell us?

The HCAI is a powerful tool because it allows us to identify with great specificity the likelihood that a specific loan or group of loans will default and how much that default risk is due to the loan type vs. the borrower. Put simply, it answers this question: is this a risky loan made to a low-risk borrower or a low-risk loan made to a risky borrower? The HCAI allows us to answer this question about any group of current or historic loans.

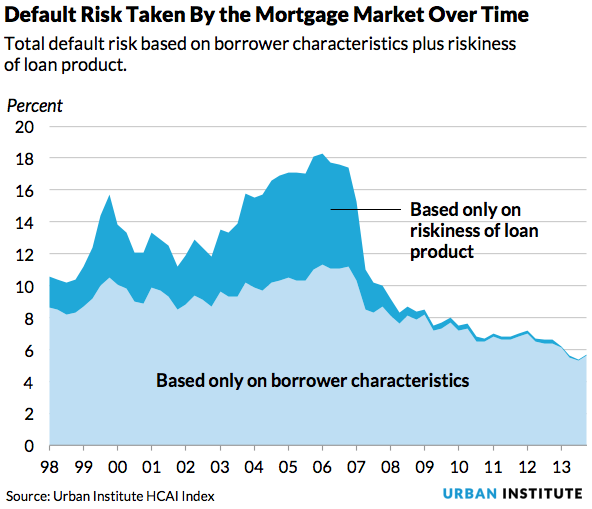

The figure clearly shows one of the most startling insights revealed by the HCAI: Product risk, not borrower risk, fueled the housing bubble. The HCAI shows that the mortgage default risk the market was willing to take peaked significantly from 2005–2008. This makes sense—we know risky lending was going on during this period. We can also see, however, that in the bubble years, the market took almost twice the product risk it took in the pre-bubble years, while borrower risk held steady.

The HCAI also reveals that post-crisis, the mortgage market almost ceased to provide loans with risky terms and significantly curtailed its willingness to accept any borrower risk, dipping well below the level held nearly steady from 1998 to 2007. More recently, lenders have been taking only two-thirds of the borrower risk they consistently maintained in the pre-bubble and bubble years—a tremendous over-correction.

How can we use the HCAI?

The HCAI allows policymakers and interested stakeholders to develop significantly more accurate answers to questions such as:

- What segments of the mortgage market are serving borrowers with less than pristine credit today and how well are they serving these borrowers?

- What percent of the FHA-guaranteed loans made last year (or at any point in time) will default?

- How much will defaults rise if we loosen current GSE-lending standards?

- How tight are credit standards today?

The Housing Finance Policy Center will be releasing the HCAI each quarter going forward. We anticipate that it will be a powerful new tool for making evidence-based housing policies.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.