<p>Tony Anderson/Getty Images</p>

COVID-19 has disproportionally harmed Native communities—and existing data likely don’t account for the extent of the effects. Generations of financial exclusion, wealth-stripping policies, and government subjugation (PDF) contributed to financial fragility that has left majority-Native communities especially vulnerable to the pandemic’s economic ramifications.

Using unique credit bureau and alternative financial service data on more than five million people with a credit file, we explored the financial well-being of people living in majority-Native communities during the pandemic in 13 states: Alaska, Arizona, Minnesota, Montana, North Carolina, North Dakota, New Mexico, New York, South Dakota, Utah, Washington, Wisconsin, and Wyoming.

Our new analysis finds that during the 2020 pandemic, people living in majority-Native communities faced persistently high rates and levels of delinquent debt, nearly half had subprime credit, and some turned to high-cost predatory lenders to meet their financial needs. Policymakers have the power to help address these inequities through targeted investments in Native financial health and access.

Native communities face systemic barriers to wealth-building and access to financial services

The data we analyzed represent people who live in zip codes where more than 60 percent of the population identifies as American Indian or Alaska Native, allowing us to capture the credit health of American Indian and Alaska Native people who live on reservations.

Native communities are diverse and represent hundreds of nations with different social, cultural, and economic characteristics. Aggregating these communities does not allow for deeper analyses into differences between communities, but highlights shared historical trauma based on experiences of settler and government actions to drive them from their lands and prevent them from speaking their languages or expressing their cultures, a legacy with persistent influence on communities’ current financial well-being.

Generations of federal policies undermined the sovereignty, wealth, and power of tribal nations, leaving them without federal support (PDF) and access to basic amenities, including mainstream financial services. Despite improved banking access over the past two decades, tribal citizens still travel at least four times as far to access services such as an ATM (PDF).

Tribal nations also face significant barriers to accessing key wealth-building opportunities, including business development and homeownership. Forced geographical relocation, domination of governments (PDF), and limiting property ownership agreements with the federal government left many tribal nations without infrastructure for services, with poorer agricultural land, and with challenges to cultivating thriving economies.

Native communities lack access to low-cost credit options

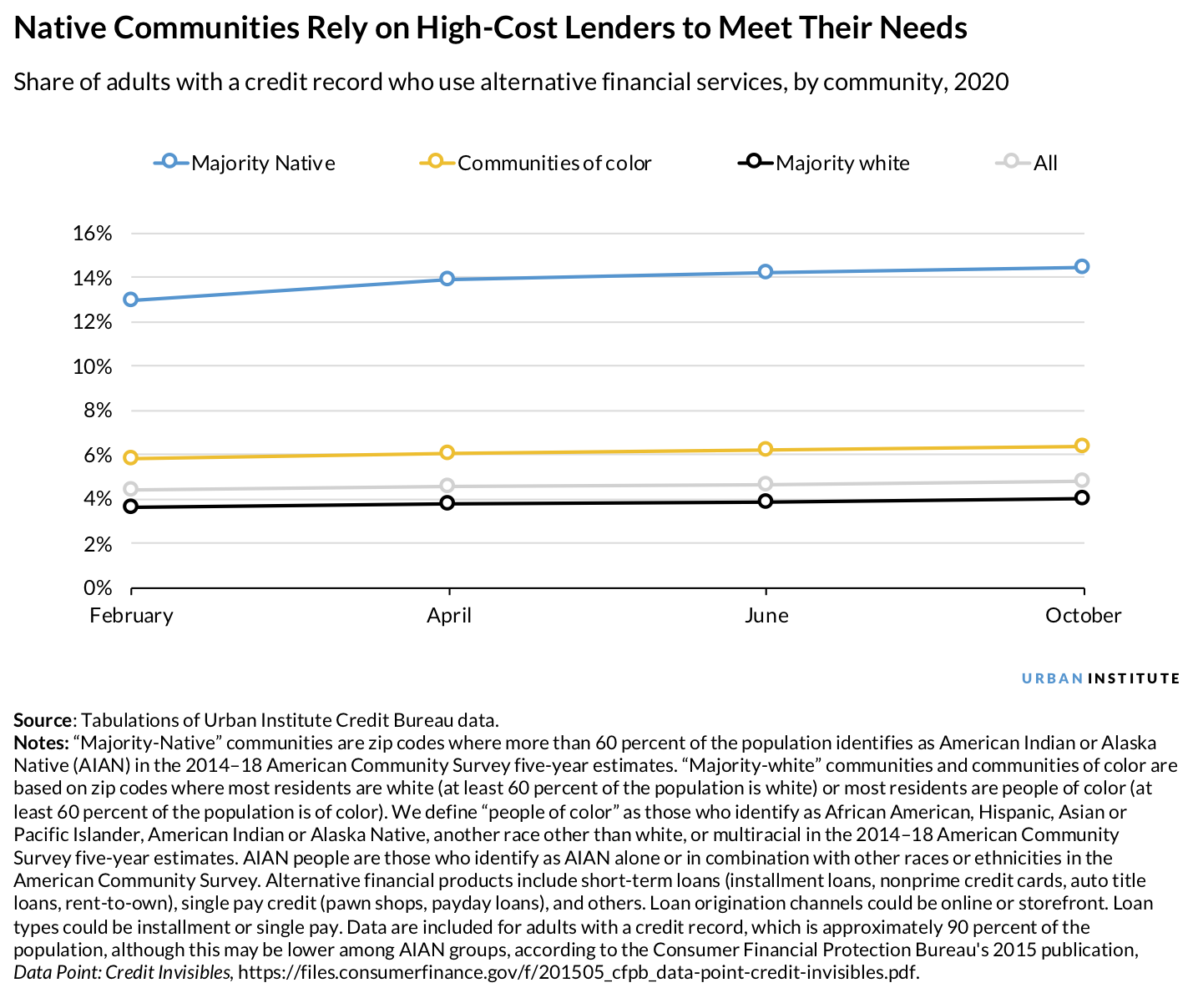

Native communities continue to lack access to affordable credit to meet their financial needs. With 17 percent (PDF) of the population not using checking services at banks or credit unions, many Native Americans rely on high-cost lenders to meet their credit needs (PDF).

Majority-Native communities used high-cost lenders (such as payday or pawnshop loans) more than other racial and ethnic groups and increasingly over the course of the pandemic. Native communities’ use of high-cost lenders may threaten their financial stability and upward mobility, and indebtedness to high-cost lenders may make it more challenging to access low-cost financial services later (PDF).

Disconnection from mainstream financial services can deteriorate peoples’ credit health. Growing up in “financial deserts” can lead to lower credit scores, more delinquent accounts, and higher lending costs when using traditional credit.

Native communities experience high delinquency and subprime credit rates

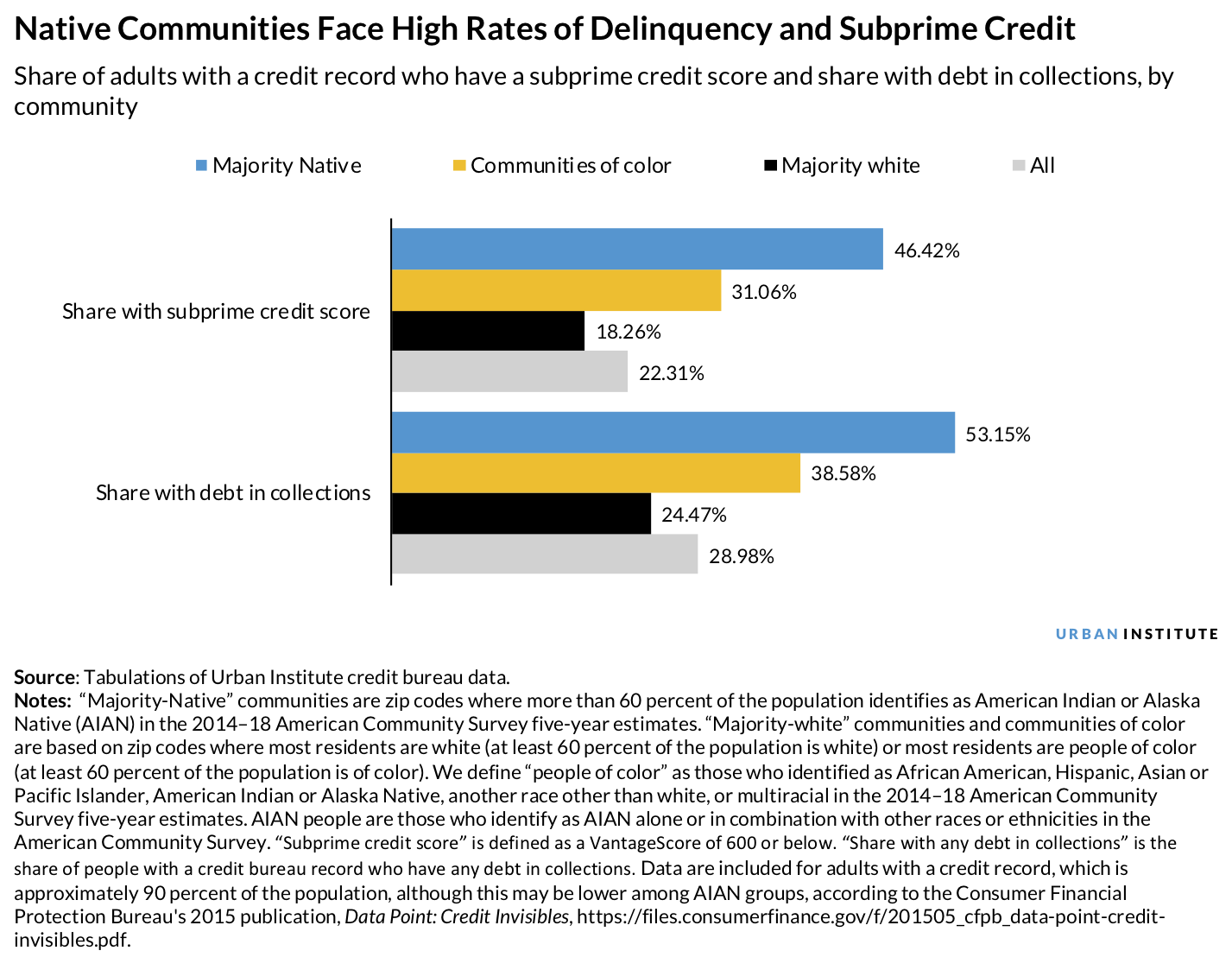

Even if people living in majority-Native communities surmount barriers to accessing mainstream credit, they may still face high costs in lending stemming from subprime credit and delinquent debt.

Nearly half of people who live in majority-Native communities have subprime credit (46.4 percent), 2.5 times higher than majority-white communities. More than half of people who live in majority-Native communities have debt in collections, and the median amount of debt in collections has remained high throughout the pandemic ($2,088 in October 2020).

Such high levels and shares of delinquent debt indicate that people living in majority-Native communities are under financial stress. Even before the pandemic, Native Americans were 1.41 times more likely to have difficulty making ends meet (PDF). This may have worsened during this year, as stay-at-home orders and tribal businesses shuttered to limit the spread of the coronavirus.

Policymakers can improve access to financial services and wealth-building for Native communities

Federal policymakers can follow the lead of tribal leaders and provide enhanced, culturally appropriate federal support to tribal nations to support their recovery from the pandemic (PDF). Some areas for investment to target financial well-being include the following:

- Strengthen and fund Native-owned financial institutions. Community development financial institutions or credit unions that serve Native communities can provide targeted services to build Native families’ financial capability and assets (PDF). Access to these institutions (PDF) can help Native families save, buy a car or home, or get a short-term loan for emergency expenses.

- Provide opportunities for wealth building. Federal policies that perpetuate fractionated ownership and hold land in trust cut Native communities out of key wealth-building opportunities in homeownership and business development, costing tribal members between $770 and $4,300 (PDF) in lost wealth per acre. The Helping Expedite and Advance Responsible Tribal Home Ownership Act of 2012 (HEARTH Act) provided an avenue for tribes to lease trust land without additional federal approval, but additional policies could remove barriers to tribes’ self-governance and ability to support wealth-building efforts. Though private ownership, a key driver of wealth-creation for many Americans, may not reflect Native communities’ relationship to their lands, federal policymakers can grant full authority for tribal leadership (PDF) in community ownership and wealth holding.

- Improve broadband access to tribal nations. Broadband infrastructure can support expanding mainstream banking services into Native communities. Currently, 35 percent of residents on tribal lands lack access to broadband (PDF), compared with 8 percent of all Americans—but this is likely an underestimate (PDF). Targeted funds for broadband development like those proposed in the Bridging the Tribal Digital Divide Act could enhance broadband infrastructure, and policies restricting the operation of high-cost lenders online can limit their proliferation as broadband access expands.

People living in majority-Native communities increasingly rely on high-cost lenders to meet their credit needs, and roughly half have poor credit or delinquent debt. Centuries of wealth-stripping policies have created and perpetuated these challenges. A better understanding of financial access barriers provides opportunities to enact respectful and culturally appropriate policies that facilitate tribes’ economic development efforts, increase investments, and bolster Native communities’ financial well-being into the future.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.