<p>Ken Voorhees, a self-employed builder, inside a construction project in Litchfield, Maine, on Wednesday, March 15, 2017. (Staff photo by Shawn Patrick Ouellette/Portland Press Herald via Getty Images.)</p>

By most measures, the US economy is running well. The unemployment rate is low, wages are rising, and the financial condition of households is improving. Many households have recovered ground lost during the Great Recession, but others are still catching up.

As we showed in a recent research brief, self-employed households continue to earn more than salaried households, but self-employed households were hit harder by the housing crisis and have been slower to recover, partly because their incomes have been slower to recover.

But at all income levels, both mortgage use and the homeownership rate for self-employed households has declined more than that of salaried households. The mortgage market is not adequately meeting the lending needs of self-employed households.

Nearly one-tenth of all US households are self-employed

In 2016, about 8.5 percent of US households were headed by a self-employed person, according to the American Community Survey, which defines “self-employed” as someone working for his or her own enterprise. Another 3.4 percent were salaried but earned some income from self-employment per the Federal Reserve’s Survey of Household Economics and Decisionmaking.

The incomes of the self-employed have not returned to their precrisis heights

While annual incomes for self-employed households have been and remain higher than for salaried households, the incomes of self-employed households decreased more significantly than those of salaried households during the recession, and, unlike salaried households, they have yet to return to their precrisis peak.

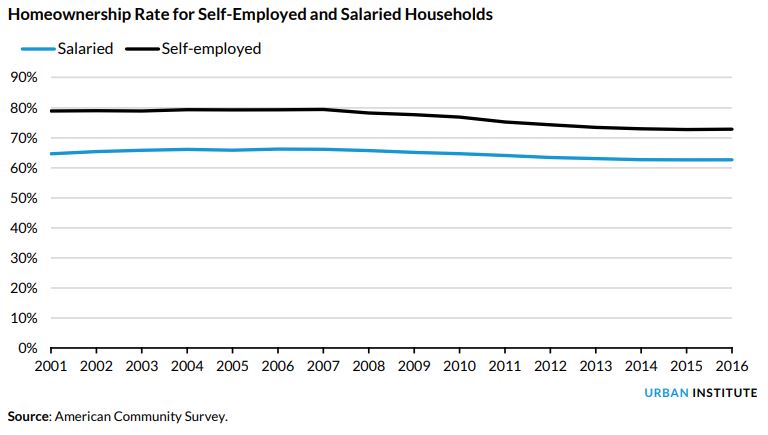

Self-employed households suffered a greater drop in homeownership during the recession

Thanks to their higher incomes, self-employed households have had a higher homeownership rate than salaried households going all the way back to 2001. From 2001 to 2007, the homeownership rate for self-employed and salaried households averaged 79.2 percent and 65.8 percent, respectively, a 13.4 percentage-point gap.

In 2016, the gap shrank to 10.2 percentage points, when self-employed households had a 72.9 percent homeownership rate and salaried households had a 62.7 percent rate. And while the homeownership rate fell for both self-employed and salaried households during the recession, the rates of self-employed households dropped more significantly.

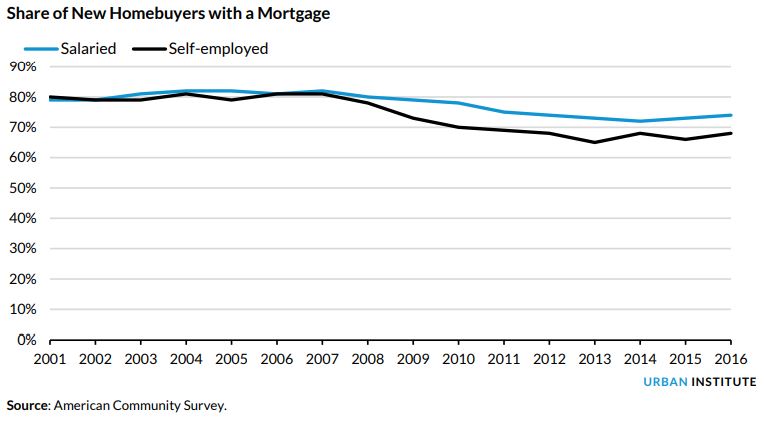

Mortgage use by self-employed households has declined more than for salaried households

Before 2007, self-employed households purchasing a home were almost as likely to carry a mortgage as salaried homebuyers—about 80 percent in each category. Use declined for both groups after 2007, but self-employed households purchasing a home in 2016 were less likely to have a mortgage (67 percent) than salaried households that purchased a home in the same year (74 percent), notwithstanding the higher median income of self-employed households.

Mortgage use among the self-employed is down in part because they face additional hurdles when applying for a mortgage. Unlike salaried workers, self-employed applicants lack pay stubs or W-2 wage statements.

Lenders must therefore rely on specific alternatives, such as tax returns and bank statements, to determine loan eligibility. These documentation requirements and guidelines for analyzing them are described in detail in appendix Q to the Consumer Financial Protection Bureau’s qualified mortgage rule. As we explain in the full brief, these prescriptive requirements are difficult to satisfy and likely make it harder for self-employed households to obtain mortgages.

Accounting for 10 percent of US households, self-employed Americans are too large a segment of the economy to be left behind in mortgage access. Absent major changes to mortgage eligibility rules, the homeownership gap between salaried and self-employed households will likely persist or even widen in the coming years.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.