A consequence of the Great Recession and the sluggish recovery has been the rising use of nonbank credit products such as payday loans, pawnshop loans, rent-to-own agreements, and refund anticipation loans. A disturbing underlying trend is that many of the consumers using such short-term, high-interest loans are first-time users and have characteristics normally associated with economic advantage, not distress. Additionally, many nonbank borrowers are using more than one such product.

From June 2010 through May 2011, the second year of the recovery, 7.2 million U.S. households used at least one of the nonbank credit products listed above. That’s 6 percent of all households nationwide. These households have found themselves unable to meet their basic needs and emergency expenses through other available resources: their own income or savings, government benefits, private support networks, or bank loans. So they have turned to the alternative financial services sector for credit, often at exorbitant interest rates.

Here are the unsettling patterns of recent nonbank credit use, based on our analysis of data from the June 2011 National Survey of the Unbanked and Underbanked:

- One-sixth of the prior-year users, or 1.2 million households, turned to nonbank credit sources for the first time, reflecting the severity of their recent earnings losses, the depletion of their assets, and (for those in long-term joblessness) the expiration of unemployment insurance.

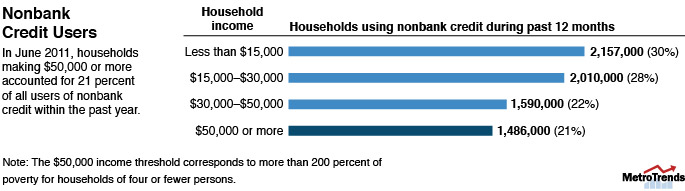

- Many of those using nonbank loan products have demographic characteristics typically associated with financially stable individuals: many have an annual household income of at least $50,000 (21 percent) and are age 55 years or older (17 percent), married (36 percent), and white non-Hispanic (55 percent).

- Nearly one in five of the prior-year users, or 1.3 million households, used two or more of the four nonbank credit product types within the 12-month survey period.

The uncomfortable reality is that continued slow job growth, coupled with the stringency of retail lending among mainstream banks, has left many American consumers with little choice but to rely on high-cost alternative lenders. And they’re doing so at a time when they can little afford the high fees and charges attached to nonbank credit products.

For an analysis of the growth in nonbank credit use from 2009 to 2011, see “The Rising Use of Nonbank Credit among U.S. Households: 2009-2011” from the Urban Institute’s Unemployment and Recovery Project.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.