<p>Trinidad de Leon shares a moment with his daughters Maria, left, and Ofelia de Leon while out for a walk on Thursday, October 14, 2010 in Oceanside, California. Photo by Sandy Huffaker/Corbis via Getty Images</p>

Hispanics are among the fastest-growing groups in the nation, nearly quadrupling between 1980 and 2014. Although the population is relatively young, the number of Hispanics ages 65 and older will more than triple over the next 25 years, accounting for 15 percent of the older US population by 2040. Many of those older Hispanics face steep financial challenges, according to our new report, often because their employment histories are marked by low-earning jobs that lack retirement benefits.

In 1989, US-born Hispanic men ages 25 to 64 and employed full-time had median earnings that were 23 percent lower than that of white men. Median earnings for foreign-born Hispanics were 47 percent lower.

The earnings shortfall for full-time working Hispanic women relative to whites was smaller, but still substantial. Low wages reduce Social Security benefits decades later and make it harder to save for retirement.

In addition, relatively few employed Hispanics had access to workplace retirement plans. In 1990, only 32 percent of Hispanic men ages 25 to 64 and employed full-time participated in an employer-sponsored retirement plan, compared with 54 percent of white men and 47 percent of black men. Disparities were similar for employed women.

Educational shortfalls account for part of these workplace disparities. In 1980, nearly half (47 percent) of Hispanics ages 25 to 44 lacked a high school diploma, compared with only 15 percent of whites and 31 percent of blacks. But even after we controlled for education, age, marital status, occupation, and English speaking ability, we found that full-time earnings in 1979 for men ages 25 to 64 were 11 percent lower for older US-born Hispanics and 15 percent lower for older foreign-born Hispanics than for whites.

These disparities persist. More research is needed to better understand why Hispanics tend to earn less than whites and why they are less likely to participate in employer-sponsored retirement plans.

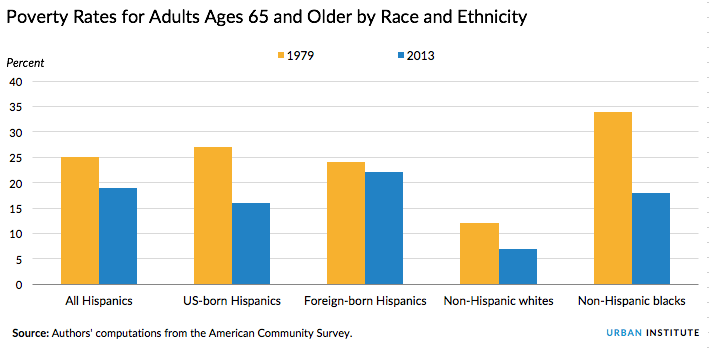

Low lifetime earnings and limited access to employee retirement benefits reduce older Hispanics’ wealth and income and raise their poverty rate. In 2012, median household wealth for Hispanics ages 65 and older was less than one-fifth that of their white counterparts. In 2013, median family income, adjusted for family size, was one-third lower for older Hispanics than for older whites, and the older Hispanic poverty rate was 12 percentage points higher.

Despite these challenges, older US-born Hispanics’ financial security improved substantially over the past three decades as educational attainment increased. Between 1979 and 2013, the poverty rate fell 11 percentage points for older US-born Hispanics, narrowing the gap between them and older whites. In 1980, 67 percent of US-born Hispanics ages 45 to 64 lacked a high school diploma; that share fell to 30 percent in 2000 and 16 percent in 2014. High school graduation rates did not improve nearly as fast for foreign-born Hispanics. Consequently, the poverty rate for older foreign-born Hispanics fell only 2 percentage points between 1979 and 2013.

Finances are especially precarious for older foreign-born Hispanics because many spent part of their careers outside the United States and had less time to accumulate Social Security and employer-sponsored retirement benefits than those who spent their entire careers in the United States. Moreover, many Hispanic immigrants came from countries with relatively low levels of educational attainment, and their skills are not always transferable to the Unites States. Language barriers and employment discrimination can create additional hurdles, especially for immigrants without legal authorization. Consequently, median 2012 household wealth for older foreign-born Hispanics was only about one-third that of older US-born Hispanics and less than one-ninth that of older whites.

Various policy options might improve retirement security for Hispanics. Workforce development initiatives and efforts to promote education could enhance skills and raise earnings, boosting future Social Security benefits and allowing more Hispanics to save for retirement. Policy initiatives that promote retirement savings, such as state mandates requiring employers to offer automatic payroll deductions that would fund retirement accounts, could help narrow disparities in retirement savings. Social Security reforms that increase benefit progressivity or create a meaningful minimum benefit would also raise retirement incomes for people with low lifetime earnings. Such changes could reduce poverty rates for all older adults, regardless of race or ethnicity.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.