<p>Living without heat, Rev. Harold Ruddick, 83, wears sweaters to keep warm in his decades old doublewide at Ojai Oaks Mobile Home park in Ojai, which is considering converting to a tenantowned park. Ruddick lives on less than $26,000 a year. Photo by Stephen Osman/Los Angeles Times via Getty Images.</p>

With limited supply and skyrocketing housing costs, renters and homeowners face severe housing affordability issues. A higher share of renters face severe housing cost burdens. Over a quarter of renters, or 11.1 million households, are severely cost burdened, spending at least half their income on rental housing.

In contrast, only 10 percent of homeowners (7.6 million) are severely cost burdened. Renters’ generally lower incomes explain most of this difference. But a close look at the data makes it clear that homeownership doesn’t protect low-income homeowners from the same cost burdens as low-income renters.

Lower incomes make renters more cost burdened than homeowners

Homeowners are less likely to have extremely low or very low income. Eight percent of homeowners have extremely low income (30 percent or less of area median income, or AMI), and 7 percent have very low income (31 to 50 percent of AMI). Twenty-six and 15 percent of renters, on the other hand, have extremely low income or very low income, respectively.

Homeowners are also more likely to be wealthy. Forty-five percent of homeowners are in the highest income group (over 120 percent of AMI), compared with 18 percent of renters.

For both renters and homeowners, the severely cost burdened are generally in the lowest income categories. Ninety-two percent of cost-burdened renters and 72 percent of cost-burdened homeowners are from the extremely low–income or the very low–income groups.

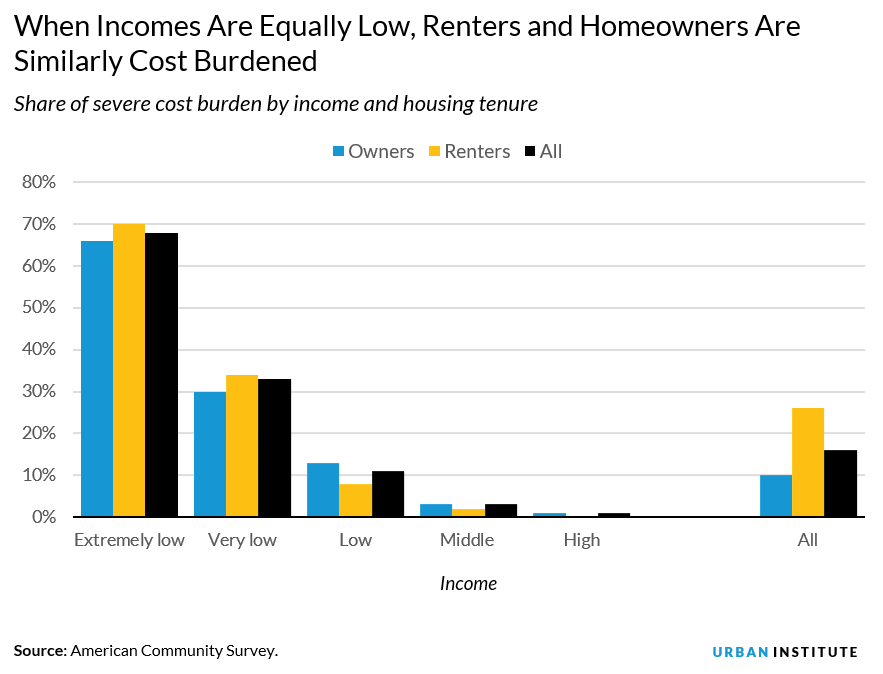

When incomes are equally low, renters and homeowners have similar rates of severe cost burden

When controlling for income, a similar proportion of low-income homeowners and renters are severely cost burdened. Extremely low–income and very low–income homeowners are just as vulnerable to severe housing cost burdens as renters at the same income level.

In the extremely low–AMI group, 66 percent of homeowners and 70 percent of renters are severely cost burdened. And in the very low–AMI group, 30 percent of homeowners and 34 percent of renters are severely cost burdened. Although renters may face greater instability than homeowners, housing presents both groups with difficulties in meeting nonhousing needs.

Extremely low–income and very low–income homeowners tend to be elderly

Although low-income homeowners and renters have similar rates of severe cost burden, the composition of these households differs significantly. Poor, severely burdened homeowners tend to be elderly, while severely burdened renters tend to have young families.

In the lowest AMI group, 37 percent have an elderly household head, and 57 percent have a child in their household. But cost-burdened homeowners are approximately twice as likely as cost-burdened renters to be elderly (54 versus 27 percent), and renters are more likely to have at least one child under age 18 than homeowners (68 versus 38 percent).

The same pattern holds true for the low-income category overall. Severely cost-burdened homeowners are more likely to be elderly and less likely to have children in the home than their renter counterparts.

When incomes are low or very low, renters and homeowners have different rates of moderate cost burden

The figure below shows that for extremely low–income households, a similar share of homeowners and renters face a moderate cost burden (spending 30 to 49 percent of their income on housing). But the benefits of homeownership kick in at the very low–income and low-income levels, where fewer households spend 30 to 49 percent of their income on housing.

Many low-income homeowners, especially low-income elderly homeowners, do not have a mortgage. For extremely low–income borrowers, the burden of property taxes, maintenance, utilities, and homeowners’ insurance overwhelm income, whereas those costs are less overwhelming on a slightly higher budget. Cost burdens equalize again between owners and renters at higher income levels (albeit at much lower burden levels), likely because some higher income owners are carrying a sizeable mortgage relative to income.

Although renters shoulder the bulk of the severe housing cost burdens, our data show that low-income homeowners, a predominantly elderly group, struggle as well.

Higher cost burdens for elderly homeowners reflect their lower incomes following retirement. But we need to understand more about this group and what kind of impact this severe cost burden has on low-income, elderly homeowners. . How does this decline in the portion of their income available for non-housing uses impact their quality of life? Can they still buy food and necessary medication, pay utility bills, maintain their home, and pay for transportation?

As populations of low-income renters and homeowners differ, the policy solutions for these challenges will likely differ as well.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.