<p>Photo by Monkey Business Images/Shutterstock.</p>

LIBOR, the London Interbank Offered Rate, which sets the rate for 2.8 million adjustable-rate mortgages (ARMs) and most reverse mortgages, is set to expire in three years. The index that appears to be LIBOR’s most likely successor, the Secured Overnight Financing Rate (SOFR), could potentially create a $2.5 to $5.0 billion annual windfall for forward mortgage holders and an equivalent loss for investors.

Fannie Mae, Freddie Mac (the government-sponsored enterprises, or GSEs), and their regulator, the Federal Housing Finance Agency (FHFA), have the greatest influence on the transition from LIBOR to a new index. Given the scope of the potential impact on investors and consumers, it’s important that the FHFA and the GSEs continue planning for the LIBOR change.

The LIBOR, dubbed “the world’s most important number,” is the rate at which banks report that they lend money to each other. It is a reference index, setting interest rates on mortgages and millions of other financial contracts totaling $200 trillion. Because of the “LIBOR fixing” scandal, in which certain banks deliberately misrepresented their lending rates (which are used to create the LIBOR), LIBOR is expected to be replaced by an alternative index by the end of 2021.

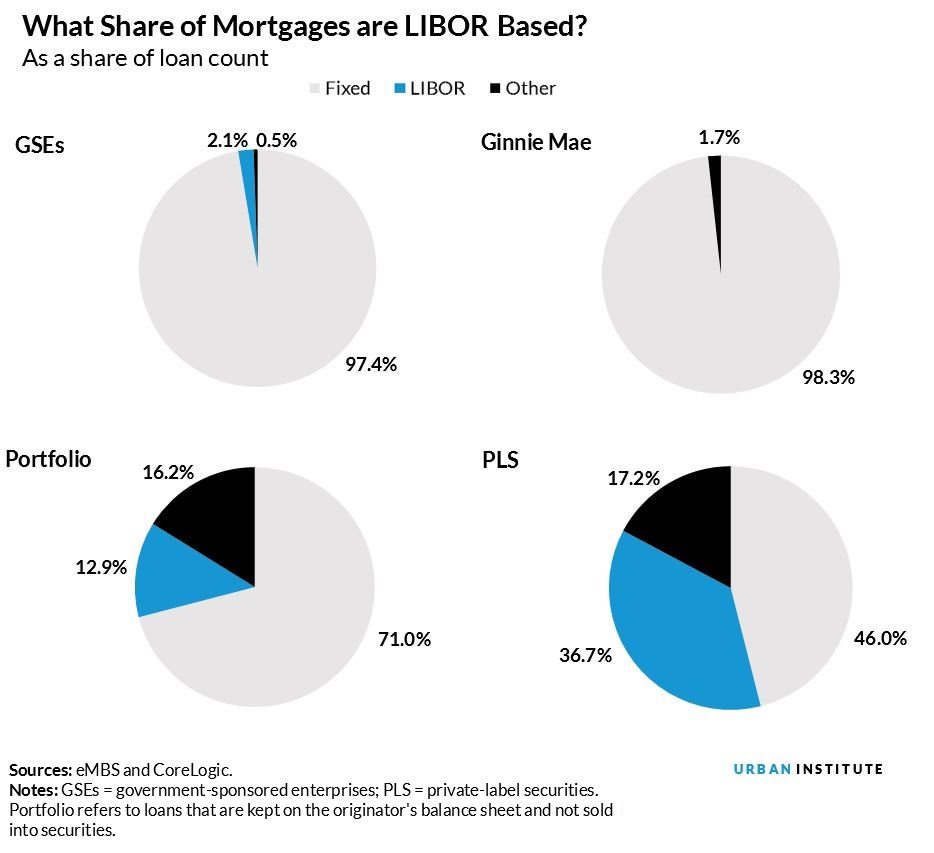

There are about $1 trillion in LIBOR-based adjustable-rate forward mortgages, or 2.8 million mortgages which represent close to 10 percent of the outstanding mortgage market. The greatest concentration is in loans held in bank portfolios and in private-label securities.

Approximately 57 percent of these 2.8 million LIBOR-based mortgages were originated pre-crisis. In terms of credit characteristics, LIBOR ARMs tend to look similar to fixed-rate loans originated at the same time, except in the private label securities market, where the characteristics of the pre-crisis LIBOR product were weaker. LIBOR ARMs tend to be larger loans than their fixed rate counterparts. This is particularly pronounced in the bank portfolio space, where the average ARM loan is $582,400 versus $306,200 for all portfolio loans.

We also need to consider the possibility of a “zombie” LIBOR

LIBOR is apt to disappear at the end of 2021. Regulatory bodies are encouraging banks to continue to submit the numbers used to create the LIBOR through the end of 2021, at which point they are likely to stop. At that point, a substitute index will need to be used.

The legal documents on most adjustable-rate mortgages allow for the substitution of a new index based on comparable information if the original index is no longer available. But contract language for most mortgages is largely silent on how to define a reasonable substitute and what it means for LIBOR to be unavailable.

On the latter issue, there is also the possibility that the LIBOR will become increasingly unreliable before it expires. As banks begin to pull back from providing information, they may create what has been nicknamed a “Zombie LIBOR,” which would be an unreliable LIBOR index and a real risk.

We believe that Fannie Mae and Freddie Mac, while they play a small role in the LIBOR market for adjustable-rate mortgages (20 percent by loan count), will decide under FHFA guidance how they want to handle GSE adjustable-rate mortgages, and the rest of the market will follow suit.

What will the SOFR do to mortgage rates?

A group convened by the Federal Reserve has recommended that the SOFR be the successor to the LIBOR, but the SOFR differs from the LIBOR in two important ways:

- The SOFR is a secured rate, while the LIBOR is unsecured and, therefore, includes a risk premium. Historically, this has meant that the SOFR has been both lower than the LIBOR and less volatile.

- The SOFR is an overnight rate, while the LIBOR is quoted for a variety of terms.

Efforts have been made to encourage the development of a longer-term SOFR, but this market has not yet matured, so it’s not clear how the longer-term SOFR will be priced. But by comparing the historic LIBOR and SOFR rates and comparing one-year LIBORs with one-year Treasuries (as a proxy for the still-emerging longer-term SOFR), we estimate that a one-year SOFR will be 25 to 50 basis points lower than a one-year LIBOR. If this is accurate, substituting the SOFR for the LIBOR could decrease the mortgage rate on the outstanding LIBOR-indexed ARMs by 25 to 50 basis points.

If SOFR was substituted for LIBOR, we estimate that, over the entire $1 trillion forward ARM market, this differential would give borrowers a change in cumulative payments and investors an increased cost of $2.5 to $5.0 billion a year, or $15 to $30 billion on a present-value basis.

Close to 90 percent of the recent reverse mortgage market originations (home equity conversion mortgages, or HECMs) and 60 percent, or $50 billion, of the overall HECM market is also LIBOR based. In the $50 billion LIBOR HECM market, the likely beneficiary would be the heirs or the Federal Housing Administration (FHA) for any paid insurance claims, and the investors in Ginnie Mae securities would face increased costs. We estimate this transfer could be about $125 million a year, or a present value of $2 billion.

Why not align the SOFR more closely with the LIBOR?

Conceptually, the SOFR rate could be more closely aligned with the LIBOR rate by defining the new index as term SOFR + x basis points. This would leave borrowers, on average, in the same position as they are now. But even here, there are potential issues.

Any add-on may work on average or “ex ante,” but it is subject to dispute. Reasonable people may come up with different estimates of the add-on, and even 1 basis point on $1 trillion is $100 million a year. We have seen litigation over smaller amounts. It may also be difficult for the mortgage market to use an add-on if the larger $200 trillion LIBOR market does not make this adjustment.

Historically, the GSEs have tried to be considerate of borrowers when reference rates are discontinued, and we would indeed see a benefit to consumers if the GSEs move to the SOFR index without an add-on.

Given the scope of the potential impact on investors and consumers, it is important that the FHFA and the GSEs continue planning for the LIBOR change in the forward market and that the FHA think about the impact in the reverse market. This is a complicated issue with no easy solution.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.