<p>Workers place prefabricated pieces in new house construction in Wilmington, NC. Photo by John Greim/LightRocket via Getty Images.</p>

Rob Dietz of the National Association of Home Builders contributed to this post.

Homeownership builds wealth and brings stability to neighborhoods, but a lack of housing supply, particularly of affordably priced homes, is suppressing homeownership today. Analysis by the National Association of Home Builders (NAHB) suggests there is a shortage of about 400,000 for-sale units nationwide, with other estimates showing even larger deficits.

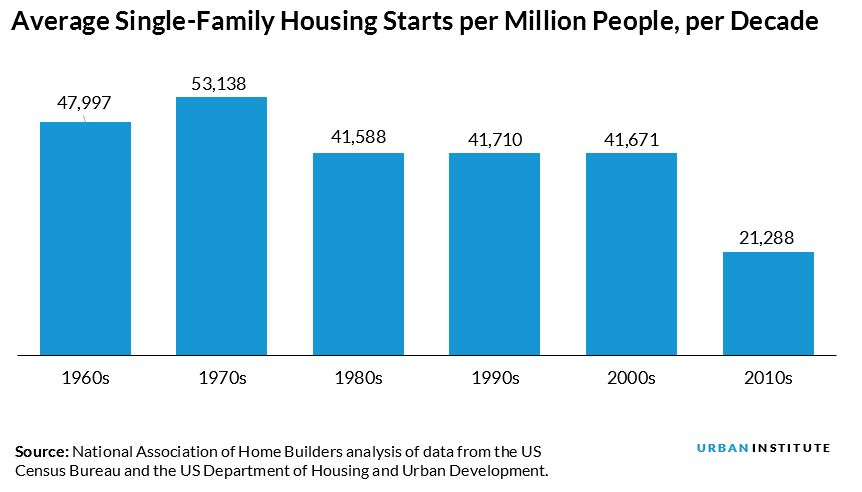

Reduced production of single-family homes over the past decade is counterintuitive because the US population has increased over time. After a downshift following the 1970’s wave of baby boomer–induced single-family home construction, the population-adjusted pace of single-family construction was remarkably constant, despite year-to-year ebbs and flows.

From 1980 through the early 2000s, single-family construction averaged just higher than 41,000 starts per million people. In the 2010s, the Great Recession triggered a production plunge, and single-family construction fell to nearly half the pace of the three previous decades.

The relative weakness of today’s affordable housing supply coincides with indications of relatively stronger demand. An assessment of online searches relative to active for-sale inventory by realtor.com suggests that a “demand surplus” is evident across much of the for-sale inventory priced below the $340,000–350,000 level, a prime price range for potential first-time homebuyers.

A key trend driving the lack of affordable for-sale inventory is the increasing costs of single-family construction, which can weigh on housing affordability. On a per completion basis, total average spending per unit in 2018 was $344,701—70 percent more than its 2009 recession-era low of $202,528.

In contrast, consumer inflation has increased 17 percent over the same period. And single-family homes dominate the owner-occupied stock, accounting for 94 percent of the owner-occupied housing stock, 88 percent the existing home inventory, and 85 percent of the total single- and multifamily for-sale housing completions in 2018.

Labor cost, availability, and productivity is a key contributor to the high cost of construction.

A number of issues have combined to make single-family construction more expensive, from higher materials prices to onerous permit fees. A recurring survey by NAHB indicates that builders, most of whom focus on single-family production, have identified labor conditions as a key barrier to construction.

Even as the total number of payroll jobs overall has eclipsed its peak level from before the Great Recession, payroll employment within the single-family residential construction industry continues to lag. The total number of jobs nationwide, 152.3 million, is 10 percent more than its prerecession peak of 138.3 million. In contrast, single-family residential construction employment is 39.9 percent below its peak level of 635,800, set in 2006.

What explains these challenges?

Difficulty filling job openings

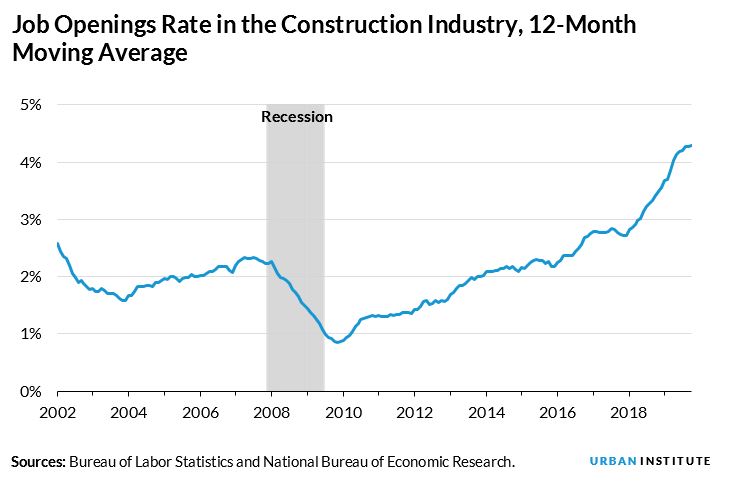

The construction industry appears willing to hire. The job openings rate across the sector (job openings relative to total employment), sits at 4 percent. There is a heavy seasonal factor, but the 12-month moving average of construction job openings is the highest it has been since December 2000, when the Bureau of Labor Statistics began tracking this data.

And the problem may get worse before it gets better. Historically, foreign-born workers have been disproportionately represented in the construction industry. The 2018 Bureau of Labor Statistics numbers indicate that 30.9 percent of workers in construction and extraction are foreign born, versus 17.4 percent of the overall labor force.

Changes in immigration policy have sharply reduced the new supply of foreign workers. Moreover, survey results of millennials ages 25–34 suggest younger people are relatively less drawn to the industry, posing concerns about its future.

Stagnant labor productivity

Average labor productivity—the ratio of total output per the total number of hours worked–has stagnated, even as the average productivity continues to increase across all nonfarm businesses nationwide. In other words, in the nonfarm business sector overall, the average worker produces more per hour of work then in the residential construction sector specifically.

Increasing labor costs

Average weekly earnings growth across employees in the single-family construction industry has outstripped that of the private sector overall. Since 2011, average weekly earnings in the single-family residential construction industry increased by 36 percent, compared with a 24 percent increase across the private sector. Average weekly earnings of residential specialty contractors increased by 25 percent over the same period.

How can we overcome these labor challenges?

The labor challenges facing the single-family construction industry have increased in recent years. Two policies could reduce this barrier to homebuilding in support of more affordable homeownership:

Encourage partnerships between community college programs and builders.

Developing local programs that partner with community colleges creates a skilled pipeline for the residential construction industry. Community colleges have the potential to provide low-cost, high-quality education and training to students while targeting skill and networking development to ensure employment following graduation.

Boost factory-built production.

Factory-built construction would reduce the need for workers, as machines replace part of the workforce, while increasing the productivity of those employed (in both productivity per hour and the number of hours, as factory construction is not weather dependent). Partly in response to these cost savings, manufactured housing costs $50 per square foot, less than half of the $111 per square foot for a site-built home.

But the share of modular and panelized single-family construction declined in 2018 to 3.3 percent, an indication that this segment of residential construction faces significant hurdles.

One possibility is that local variation in building codes combined with the limits and costs of customization hinder economies of scale in production. Although use of some factory-produced components like trusses has become widespread, survey results indicate that newer, more innovative types of construction technology, such as 3D printing and robots, have not yet significantly penetrated the residential market.

The lagged recovery in single-family construction represents a key barrier to growth in homeownership, and the cost and availability of labor directly affects the recovery in single-family construction. A concerted effort across all levels of government to safely reduce the myriad barriers to construction can help to fundamentally “bend the supply curve.”

A more in-depth look at today’s housing stock and production trends is available in our recently released Housing Supply Chartbook.

The authors of this post were updated to remove Nathan Dietz on 1/22/2020.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.