Photo by John Moore/Getty Images

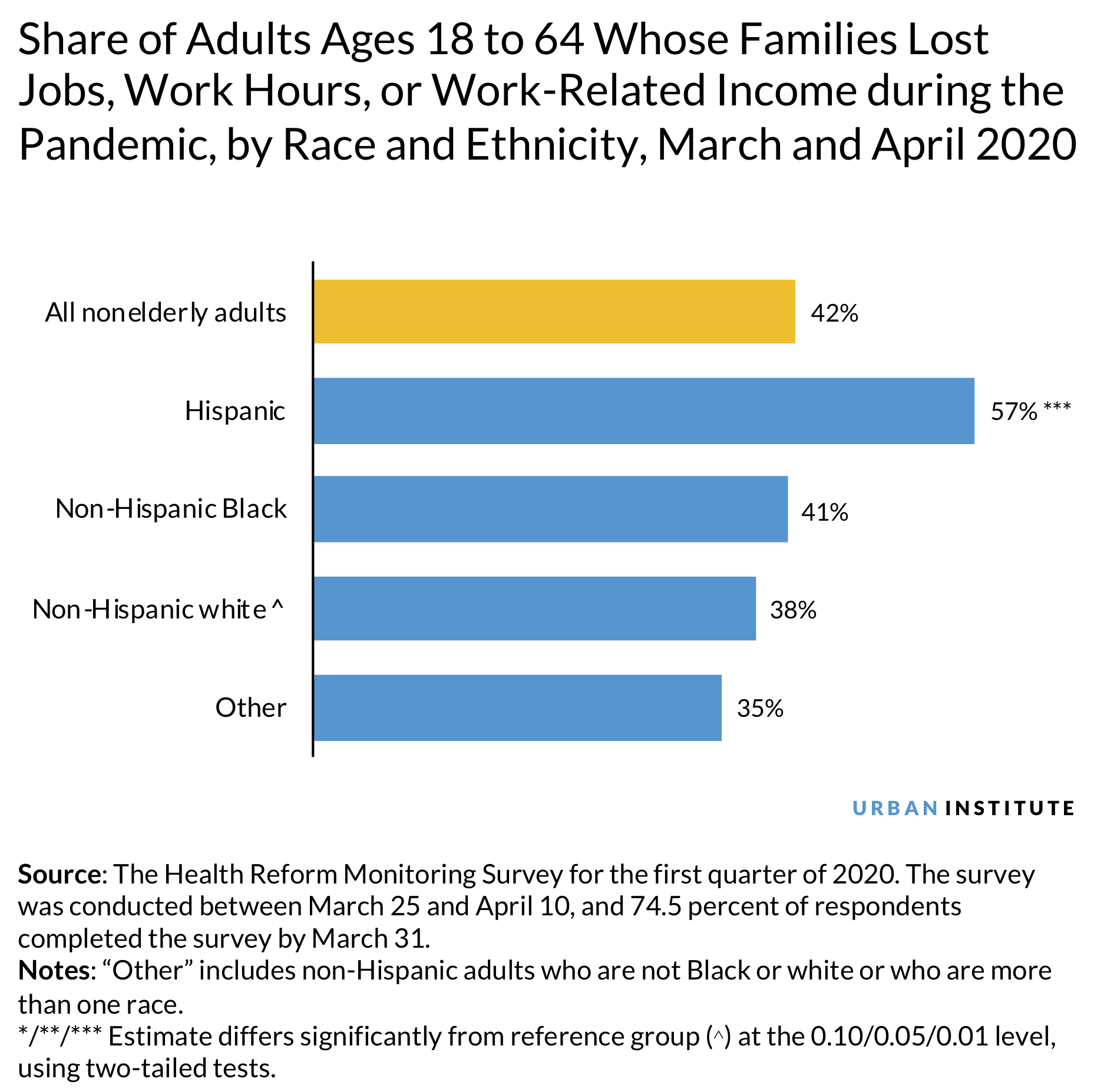

As tens of millions of Americans file for unemployment insurance, a new nationally representative survey found that, as of late March and early April, just over 4 in 10 nonelderly Black adults belong to families in which someone lost a job, was furloughed or had hours cut, or lost work-related income because of the coronavirus outbreak.

Although the employment-related losses closely followed the national average (40.7 percent of Black adults compared with 41.5 percent of adults nationally), underlying structural factors, such as occupational segregation and less relative wealth, suggest families of color will face disproportionately greater challenges as the COVID-19 crisis continues.

(Note: while the data source cited uses the term Hispanic, I’ve chosen to use Latino in the text to be more inclusive of the way this group self-identifies.)

Many Black and Latino workers hold risky and low-paying jobs

Before the crisis hit, many Black and Latino workers held jobs done outside the home. Only 35.4 percent of Black adults and 25.2 percent of Latino adults reported they can do part of their work remotely, compared with 43.4 percent of white adults. Though reporting somewhat higher averages, these estimates largely correspond with earlier US Bureau of Labor Statistics (BLS) data on racial and ethnic differences in the ability to work from home.

Differences in who can telework could indicate who’s at higher risk of losing a job, hours, or income. But despite multiple sources showing Black and Latino adults are less able to work from home compared with white adults, families of nonelderly Black adults experienced only minimally higher rates of job loss.

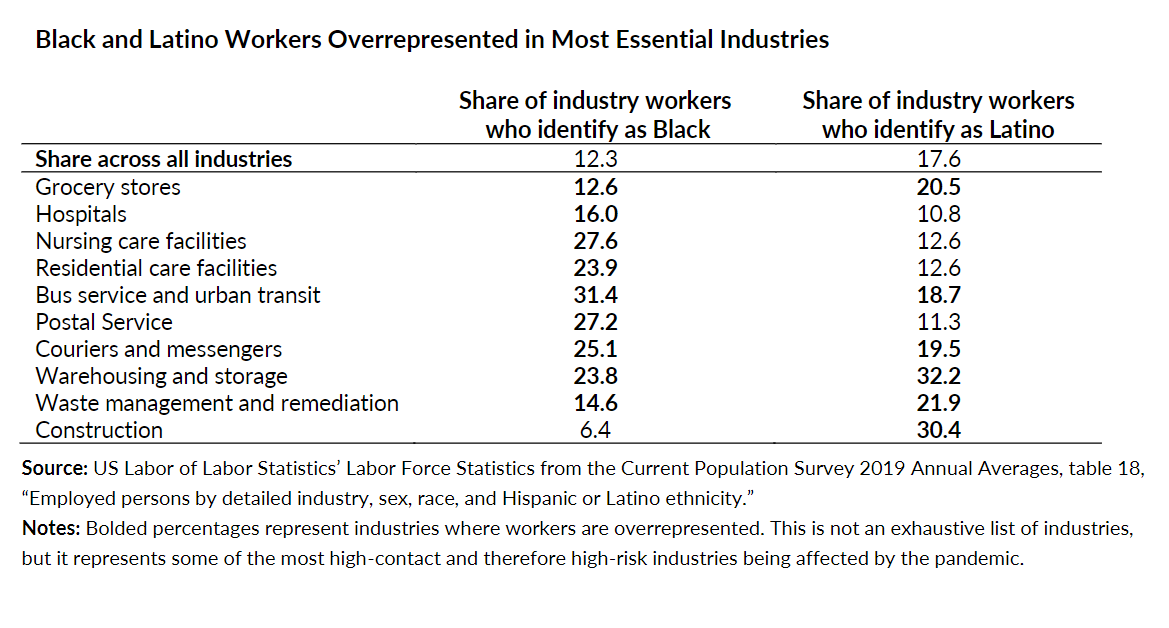

Black workers in particular are disproportionately employed in many of the jobs considered “essential,” suggesting Black workers may experience less drastic job losses than would be expected.

The frightening trade-off for many of these still-employed workers is that despite still earning income, they are at higher risk of contracting the coronavirus through increased exposure to other people and potentially contaminated surfaces. People working in nursing homes and the sanitation industry and as bus drivers and shipping and logistics employees are indeed getting exposed to and catching the coronavirus.

Preliminary state data strongly suggest Black people are contracting the coronavirus and dying from COVID-19 and related complications at highly disproportionate rates. Although racial and ethnic demographic information is absent from many of the reported cases, the early data are deeply worrisome and reflective of the ongoing impacts of structural racism.

That workers of color end up in different kinds of jobs is not random. Occupational segregation has been a consistent feature of the labor market for decades because of differences in education, place of residence, segregated job-search and referral networks, and persistent discrimination in hiring.

These jobs are indeed essential, but many pay relatively low wages. That these jobs are held primarily by people of color and especially by Black workers is not surprising, but it is concerning. The pay and protection of essential workers should be a primary concern for policymakers and employers in the coming months, as the economy recovers and we rebuild our safety net.

Black and Latino families are generally more financially vulnerable, and unemployment makes it worse

Black and Latino adults also report higher rates of family financial insecurity and hardship. More than 45 percent of Black and Latino adults said that in the past month, their families experienced material hardship, such as food insecurity or the inability to fully pay their mortgage, rent, or utilities—almost double the share of white adults and their families.

Larger shares of Black and Latino adults also reported their families had to delay major purchases, cut back spending on food, and reduce saving or increase credit card debt, regardless of whether they had lost jobs, hours, or income.

The most recent data on wealth show Black and Latino households already hold much less wealth than white families—10 percent and 12 percent as much at the median, respectively.

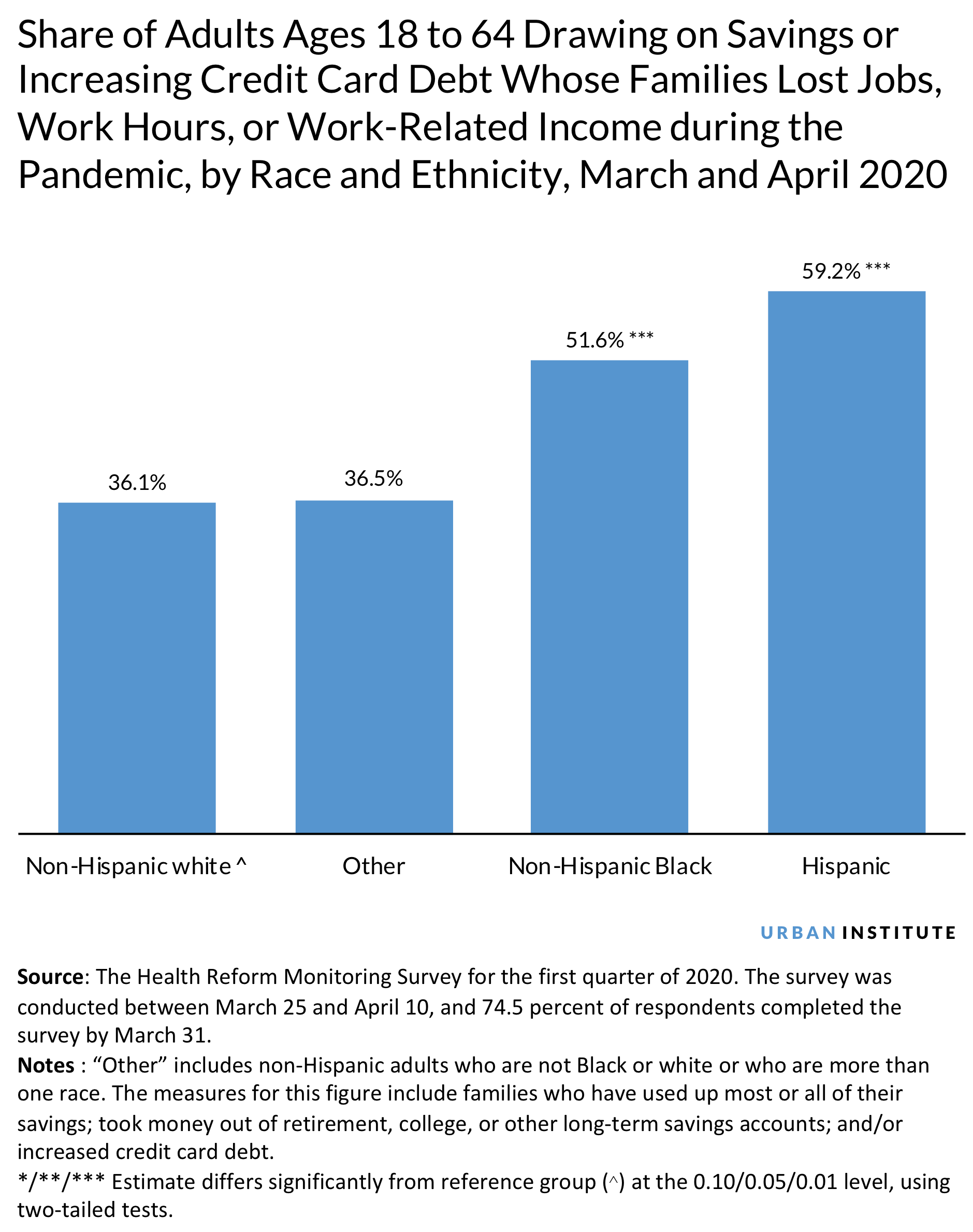

With fewer resources to draw upon, it’s unsurprising that so many Black and Latino families report drawing down savings or increasing credit card debt to weather the crisis. But this relative financial insecurity makes the situation especially challenging for families of color who may have lost work.

Among families who had reported a loss of a job, hours, or income, more than half of Black adults and nearly 60 percent of Latino adults reported that their families used up most of their savings, pulled funds out of long-term savings accounts, or increased their credit card debt. Families of color are in especially vulnerable positions upon losing a job. Even before the current crisis, more than 58 percent of Black and Latino families are estimated to be in liquid asset poverty, meaning they don’t have enough liquid savings to cover three months of expenses.

Although some states are beginning to reopen their economies, most projections suggest families may be out of work or on furlough for months to come, and the unemployment rate is estimated to still be above 10 percent by the end of the 2020.

Although unemployment insurance has been expanded, many families still struggle to access benefits because of technological and staffing challenges and overwhelming demand. Furthermore, the $600-a-week supplement is slated to end in July. Even if families can get access, most Black and Latino families who cannot resume work at their previous hours and pay will likely be unable to sustain themselves into the fall.

Black jobseekers typically have the highest unemployment rates of all racial and ethnic groups. Even when the Black unemployment rate decreased to a record low of 5.4 percent in August 2018, the white unemployment rate was still a full 2 percentage points lower. The COVID-19 crisis will almost certainly mark the highest Black unemployment rate since 1948, when the BLS began collecting unemployment data by race, and the time it takes to for the economy to recover could lead to widespread economic devastation among communities of color, exhausting their limited wealth and dramatically increasing debt that will take even longer to pay down.

What to do next

Families of color experience greater financial insecurity because of long histories of employment discrimination that hindered pay, housing discrimination that limited wealth building, and residential segregation that slowed mobility. To help them through the current crisis, immediate efforts to increase access to jobs and prevent unsustainable increases in debt will be particularly beneficial.

And given that Black families are suffering more acutely from COVID-19 related deaths, any efforts to support families who have experienced financial hardship would provide much needed and deserved support.

Policymakers could consider the following:

-

increasing protection and pay for essential workers

-

establishing a federal jobs program to get people back to work and prevent extended periods of unemployment for people of color

-

supporting efforts to stabilize renters, such as a universal voucher program for low-income renters; extend forbearance and repayment plans; and improve access to refinancing for homeowners

-

developing assistance programs for families who have lost loved ones from COVID-19 to help cover medical expenses, funeral expenses, and lost income from having to quarantine and care for sick family members

-

undertake bold promising solutions to improve financial well-being, overcome structural racism, and achieve quality jobs for all workers

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.