Amid the partisan rancor surrounding the release of President Obama’s 10-year budget this week, one issue stood out as a promising area of consensus from lawmakers across the aisle: the need to act now to enable the Federal Housing Administration to protect taxpayers from risk.

At Thursday’s House Financial Services Subcommittee on Housing and Insurance hearing on the future of the FHA, Democrat and Republican committee members heard from Urban Institute President Sarah Rosen Wartell and other expert witnesses. The message? Act swiftly on legislative proposals that would help FHA more nimbly and effectively mitigate losses from insured loans, and deal with complicated, more contentious questions about the agency’s mission when reform is more feasible.

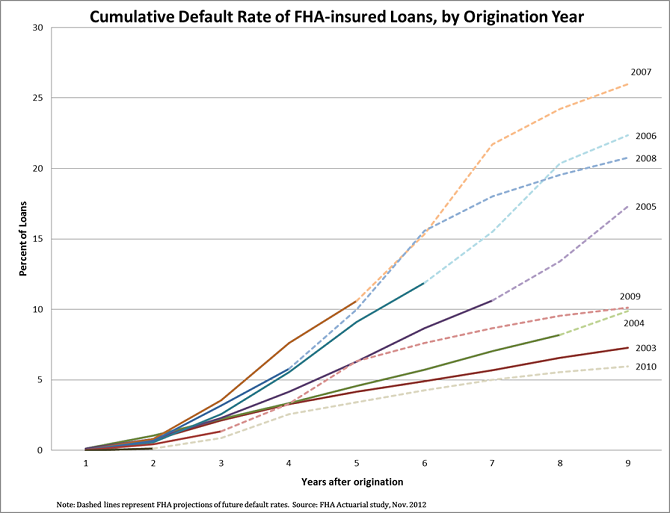

By insuring mortgages, FHA provides access to credit for borrowers underserved by the private market. The agency experienced significant losses from loans that originated in the midst of the crisis. While its financial situation is improving, an actuarial review released in November showed that its fund was underwater by over $16 billion, raising concerns about its solvency.

The FHA Fund has experienced losses that resulted primarily from loans originated in the years immediately preceding the housing market crash. Default rates for loans originated after 2008 are significantly lower.

While some have suggested that FHA must revise its mission to be sustainable in the long term, the panel of witnesses at the hearing, including industry representatives and research experts, agreed that some steps can be taken immediately to improve the agency’s financial condition. However, some witnesses emphasized that the current attention on FHA presents an important opportunity to improve the housing finance system and national housing policy, and urged policymakers to assess changes to FHA within the broader context of GSE to whatever extent possible.

Wartell suggested increasing FHA’s authority and resources to assess and mitigate risk through expanded emergency powers and greater use of early warning indicators. She also stressed the need for pilot programs to test the costs and benefits of risksharing with private mortgage insurers. Risksharing could reduce FHA’s and the taxpayer’s exposure while allowing FHA to continue serving as a critical countercyclical force—a backstop for the housing market—in times of crisis.

Not only did these proposals enjoy support from the committee members and witnesses, but some of them have been voted on by Congress before with widespread support from both parties. The FHA Emergency Solvency Act of 2012, which passed the House 402–7 but died in the Senate, would have hastened FHA’s ability to stop irresponsible underwriting from lenders and restored the agency’s fiscal solvency. The hearing’s expert witnesses agreed that the legislation must be revisited.

Most important, Wartell insisted, lawmakers must not hold off needed improvements to FHA while waiting to resolve broader questions about where the agency fits in the bigger picture of U.S. housing finance policy.

Future reforms of Fannie Mae and Freddie Mac, which are both currently in conservatorship of the Federal Housing Finance Agency, will almost certainly affect the role and scope of FHA. And those reforms will offer an opportunity to streamline the U.S. housing finance system, currently a fractured collection of agencies and policies.

While these are indeed important questions to debate moving forward, Wartell told the committee not to hold off on improvements to FHA now.

“If you choose to delay these measures while Congress debates broader mission questions and the system as a whole, the FHA Fund will continue to absorb available losses,” she said. “There is no reason to wait to protect taxpayers from those preventable costs.” Note: this post has been edited to account for nuances in the range of opinions presented at the panel discussion.

Photo by Flickr user, Cameron Rogers, used under a Creative Commons license. (CC BY-NC-SA 2.0)

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.