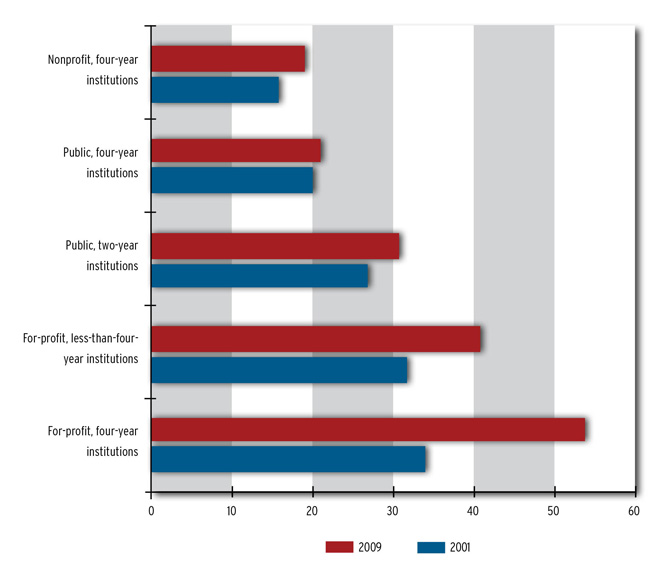

Over the past few months, high school seniors and their families across the United States have been making decisions about college—where to go and how to pay for it. So the release of a recent study on student debt is particularly timely. The study looks at students who took out loans and then dropped out of college. This is one of the worst outcomes possible; the borrowers are saddled with debt but lack the degree that would raise their earning potential, helping them pay off the loan. Dropping out is a bigger problem at for-profit institutions than at nonprofits, with over 50 percent of borrowers at four-year, for-profit institutions and over 40 percent of borrowers at two-year, for-profit institutions dropping out (figure 1).

Even students who graduate leave school more heavily indebted than in the past. In 2008, graduates who earned a bachelor’s degree borrowed 50 percent more, in inflation-adjusted dollars, than those who graduated in 1996. Graduates who earned an associate’s degree or undergraduate certificate borrowed more than twice as much as those who graduated in 1996.

Anyone who hears about growing student debt could well decide to pass on college, but is that the right decision? Probably not, because a college degree pays off for most students in the form of higher income and more career options. But the debt topic should prompt serious family discussion about how much various college options cost, how to pay for them, how much to work while in school, and how the student should manage his or her finances during and after college. In fact, figuring out how to finance an education can be an important teachable moment for young people, as going off to college is usually the first time many will be making independent decisions about living expenses and credit cards and learning how to balance work and studies.

Figuring out the cost of college is somewhat easier now, due to the Higher Education Opportunity Act of 2008. The Act requires all higher education institutions receiving financial aid to post a net price calculator on their websites. The calculator helps students and their families figure out the true cost of attending that institution for one year. But students (and sometimes their parents) are hampered by limited financial knowledge. Studies have shown that financial literacy is relatively low among both youth and adults—particularly among low-income and minority families, the very populations to whom for-profit schools market their programs (and student loan opportunities).

The federal government is promoting greater financial literacy through its Financial Literacy and Education Commission. But these efforts are only effective if families and educational institutions use available tools to help students make good decisions, keeping in mind not only their future debt burden, but also the long-term financial benefit of having a college degree.

Figure 1: Percent of Borrowers Who Dropped Out of Postsecondary Institutions, 2001 and 2009

Source: Mary Nguyen, “Degreeless in Debt: What Happens to Borrowers Who Drop Out” (Washington, DC: Education Sector, 2012)

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.