<p>Photo via Shutterstock.</p>

Recently released data show that graduate student borrowing decreased from 2011–12 to 2015–16, with more students earning advanced degrees without debt and fewer taking on large amounts of debt. But the aggregate debt figures conceal areas of concern.

Graduate students borrow more than undergraduate students. Among 2015–16 bachelor’s degree recipients, only 11 percent borrowed $50,000 or more, compared with 21 percent of master’s, 36 percent of research doctoral, and 65 percent of professional degree recipients. Average annual borrowing is about three times as high for graduate students as for undergraduates—$18,400 per full-time equivalent graduate student versus $5,400 per undergraduate in 2016–17.

Despite these large loan amounts, both the share of graduate students borrowing and the size of their loans declined between 2011–12 and 2015–16. In 2007–08, 42 percent of master’s degree recipients did not borrow at all for their graduate study, while 14 percent borrowed $50,000 or more (in 2016 dollars).

Four years later, only 35 percent avoided debt, and 20 percent borrowed $50,000 or more. That seems to have been a peak, however. In 2015–16, 38 percent of master’s degree recipients graduated without debt, and 21 percent borrowed $50,000 or more.

The share of professional degree recipients graduating without debt rose from 13 to 21 percent between 2011–12 and 2015–16, and the share borrowing $100,000 or more (in 2016 dollars) fell from 58 to 50 percent. The share of professional degree recipients who had received Pell grants in college was slightly higher in 2015–16 (28 percent) than in 2011–12 (26 percent), so the explanation does not appear to be fewer students from low-income backgrounds.

Among the 5 percent of advanced degree recipients who earned research doctoral degrees in 2015–16, however, 42 percent graduated without debt, a decline of 4 percentage points over four years, and 20 percent borrowed $100,000 or more, up from 16 percent in 2011–12.

Despite the overall drop in borrowing, some groups of graduate students deserve attention. Sixteen percent of master’s degree recipients who earned their degrees in the for-profit sector borrowed $75,000 or more, compared with 5 percent of those from public universities and 12 percent from private nonprofit universities. A quarter of for-profit students earned their master’s degrees without borrowing, compared with 37 percent overall. Fifteen percent of research doctoral degrees came from the for-profit sector, where half the students borrowed $100,000 or more, compared with less than 20 percent of those in the private nonprofit and public sectors.

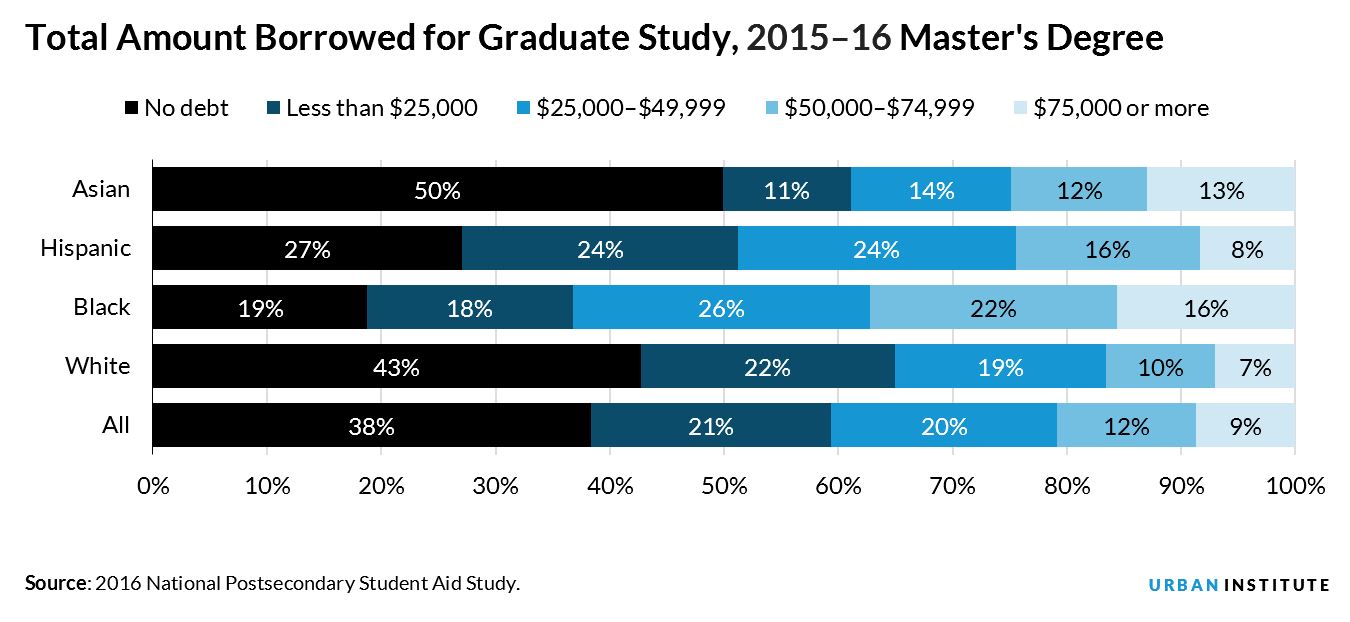

Differences by race and ethnicity are stark.

Black graduates are less likely than others to avoid debt and more likely to borrow large amounts. For example, 38 percent of black graduates borrowed $50,000 or more for graduate study versus 24 percent of Hispanic graduates and 21 percent of all master’s degree recipients.

These data raise questions for policymakers considering reforms to federal graduate student loan programs. Though the overall decrease in debt can be seen as a positive, it’s important to understand why different groups take on more debt than others, why different types of institutions vary so widely in how much debt their graduates accrue, and what the long-term implication of graduate student borrowing are for both students and taxpayers.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.