<p>martin-dm/Getty Images</p>

With more than 4 in 10 nonelderly adults reporting that their families have lost jobs, work hours, or work-related income because of the coronavirus outbreak, many families in the US are experiencing unprecedented levels of financial distress. But these challenges are not evenly distributed across all generations.

In the Urban Institute’s March and April 2020 Health Reform Monitoring Survey, 57.4 percent of Gen Z adults (18-to-22-year-olds) reported their families experienced job-related losses, compared with 35.4 percent of working-age baby boomers (55-to-64-year-olds), 41.1 percent of Gen Xers (39-to-54-year-olds), and 41.4 percent of millennials (23-to-38-year-olds).

Young adults’ financial lives are different from those of older adults, affecting their financial worries and coping strategies during the pandemic. In 2018, only 24 percent of 18-to-22-year-olds said they were financially independent from their parents. But this age group is not just made up of college students supported by their parents; only around half of 18-to-24-year-olds are enrolled in or have completed college, and around 71 percent of 20-to-24-year-olds are in the labor force.

Before the pandemic, one-third of Gen Zers worried about covering everyday expenses, including transportation and food, and one-quarter worried about paying for their own or a family member’s education. The pandemic exacerbates these worries, as young workers who enter the job market during a recession may experience lasting disadvantages that limit their ability to establish financial security throughout adulthood.

How are young adults dealing with financial distress during the pandemic? What are their financial worries for the future? These new data can inform strategies policymakers can leverage to help young adults better mitigate financial stressors and shocks, now and in the future.

Worries about debt and bills could grow into financial distress and delinquency

Compared with working-age baby boomers, more Gen Z adults, millennials, and Gen Xers reported they were very or somewhat worried about their and their families’ ability to pay monthly bills, debts, and medical costs in the next month.

About one-third of Gen Z adults, millennials, and Gen Xers were worried about their families’ ability to repay their debts next month. As pandemic-related hardships persist, challenges with debt repayment may escalate into delinquency, which can affect long-term financial security.

Though the youngest adults are less likely to have expensive medical costs and only slightly less likely to have health insurance coverage than adults overall, more than one-quarter of Gen Z adults, millennials, and Gen Xers reported being worried about their or their families’ ability to afford medical costs in the next month.

If this leads to delinquent medical debt, it could keep younger adults from meeting long-term financial goals, such as saving for retirement or a home purchase, or could constrain their ability to weather future crises.

For example, adults whose families had problems paying medical bills in the past year resorted to financial coping more readily during the pandemic. Forty-six percent of adults whose families struggled with medical bills drew down their savings during the pandemic, compared with 12.5 percent of adults whose families did not have problems paying medical bills, and 33.5 percent did not pay the full amount of their utility bills (compared with 5.9 percent of adults whose families did not have problems paying medical bills).

As Gen Z adults continue to experience pandemic-related job losses, they may also lose access to employer-provided health care, which may increase their medical costs and likelihood of incurring past-due medical debt.

Gen Z may be especially vulnerable to future hardships as the pandemic continues

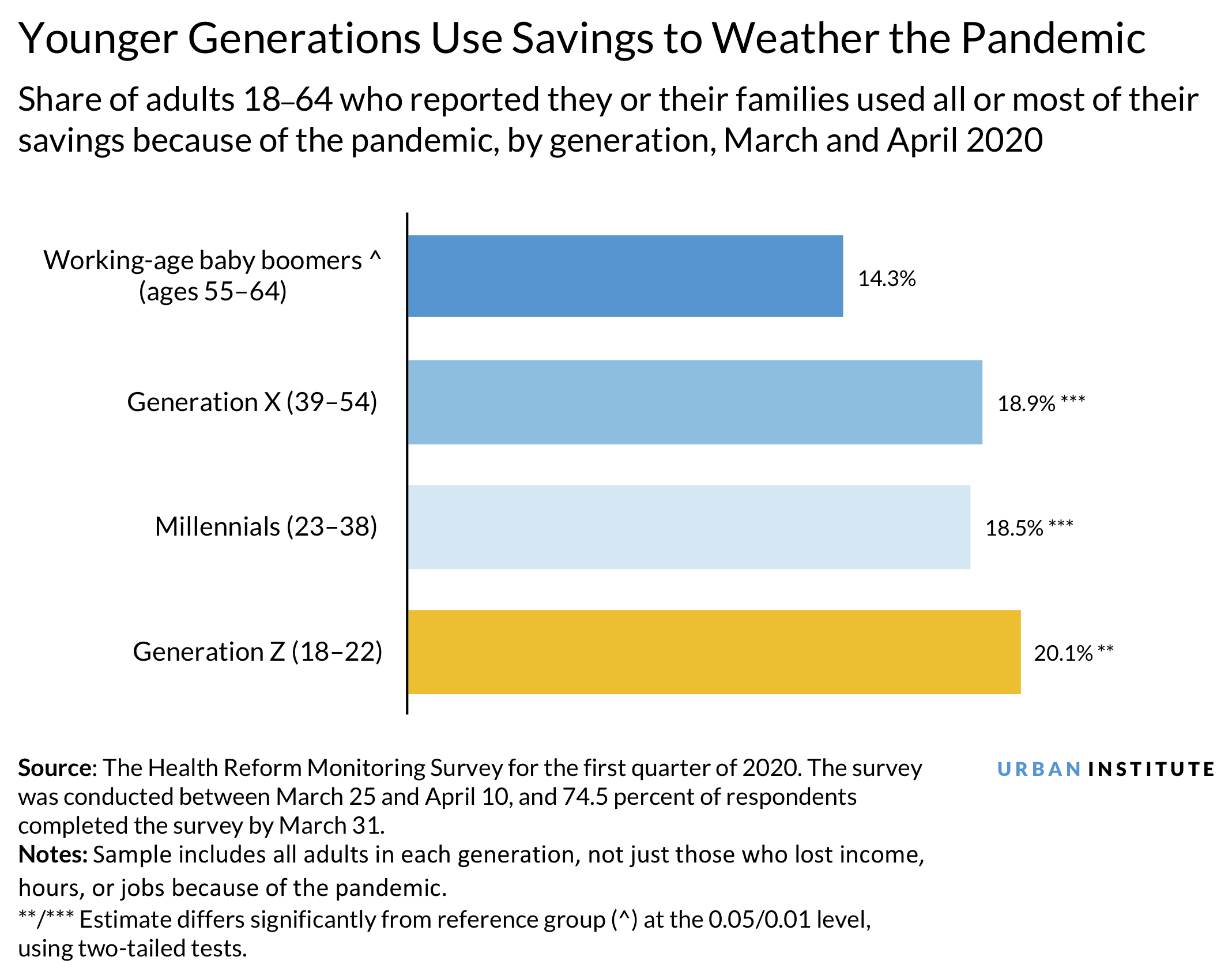

Savings can help families weather financial shocks, but Gen Z adults, millennials, and Gen Xers were more likely than working-age baby boomers to report that they or their families used all or most of their savings during the pandemic. With less time to accumulate, younger generations may have lower levels of savings, which could easily be depleted during a crisis. This may affect their future financial security, as lower levels of savings may limit their ability to weather future shocks.

Gen Z adults (66.5 percent) are less likely than millennials (74.9 percent), Gen Xers (74.7 percent), and working-age baby boomers (78.4 percent) to be very or somewhat confident they could come up with $400 for an unexpected expense. This suggests Gen Z could be more vulnerable to missed housing or utility payments during income disruptions.

Seventy-seven percent of Gen Z adults rent their homes, compared with 35 percent of all adults. Almost 60 percent of young adult renters are housing cost-burdened (PDF) and spend more than 30 percent of their incomes on housing and utility costs. This is reflected in Gen Z’s financial worries; more than one-third of Gen Z adults reported being worried about their families’ ability to meet monthly bills in the next month, compared with roughly one-quarter of working-age baby boomers.

Without savings to buffer against shocks and with limited access to other forms of credit, Gen Z may turn to predatory lenders, borrow from family and friends, or decrease spending on essentials to meet other needs. Although only 8 percent of Gen Z (compared with 13 percent of millennials and Gen X) have taken out payday loans in the past two years, nearly 38 percent have considered it. Ongoing costs, including transportation or rent, are the primary reason consumers turn to payday lenders (PDF).

What policies could support Gen Z’s financial stability during the pandemic?

- Congress could issue more relief payments and make dependent adults eligible. Dependents ages 17 to 24 (like many college students) were excluded from relief in the Coronavirus Aid, Relief, and Economic Security Act. The Health and Economic Recovery Omnibus Emergency Solutions Act, recently passed by the US House of Representatives, makes these young adults eligible. Small amounts of relief can make a big difference, as families with even small cash buffers are less likely to miss housing payments and experience other hardships.

- Financial institutions could offer affordable short-term credit to young adults with little to no credit history. About half of credit-active Gen Z adults have a prime credit score to secure affordable loans. Banks and credit unions could consider offering loans with alternative underwriting strategies, low fees, and flexible repayment plans.

- States could continue providing relief on utility bills. Data show that many young people are worried about meeting their monthly household bills. About half of states have stopped utility shutoffs, giving customers flexibility to prioritize their financial obligations. States could also ease late fees and prohibit negative credit reporting (PDF) for utility nonpayment.

- States could bolster their unemployment insurance systems with short-time compensation programs. These programs replace wages for workers who have lost hours but remain employed, which could be especially helpful for young workers just building employment relationships and who might face long-term consequences from full unemployment.

- Congress could pass legislation that stabilizes health care for young adults. These data reemphasize the relationship between medical debt and access to health insurance. To reduce young workers’ reliance on unsteady employment for coverage and to reduce out-of-pocket costs, Congress could enhance Marketplace subsidies and increase the federal matching rate for Medicaid. Longer-term options span from tweaks to the Affordable Care Act to single-payer reform.

Though the youngest adults are less likely to be fully financially independent than older adults, many will need more support to recover from this recession and start adulthood on solid footing.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.