Photo by Drew Angerer/Getty Images.

Making public college tuition “free” is a popular Democratic campaign proposal, but free college might have a smaller impact on student debt than many expect.

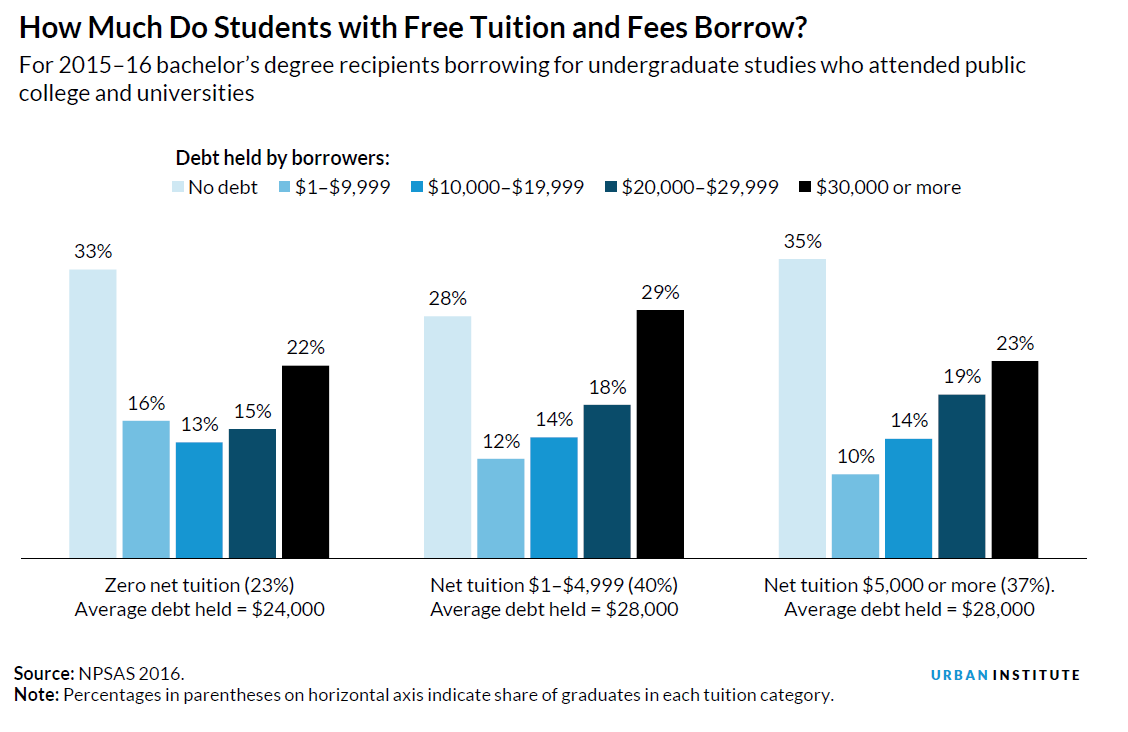

Almost one-quarter of students who earned bachelor’s degrees from public colleges and universities in 2015–16 attended for “free”—their full tuition and fee price was covered by grant aid—in their final year. (The share of public four-year college students paying zero tuition and fees is highest for first-year students and lowest for those in their final year.) Yet, two-thirds of these students graduated with debt.

The cost of college goes beyond tuition

Financing college involves more than tuition prices. Students must pay for books and supplies and cover their living expenses while they are in school. It is difficult to work full time and succeed in college, so students need other resources.

Whether they and their families have saved in advance, how much they can earn while they are in school, how long it takes them to complete their programs, their responsibilities to family members, and lifestyle choices all contribute to their need to borrow to supplement their budgets. (You can learn more on the Urban Institute’s college affordability website.)

Advocates might assume that if college is free, few students will rely on loans. But the data on college graduates suggest otherwise. Even among students who pay no tuition and fees, the majority rely on student loans.

Free college and borrowing across income brackets

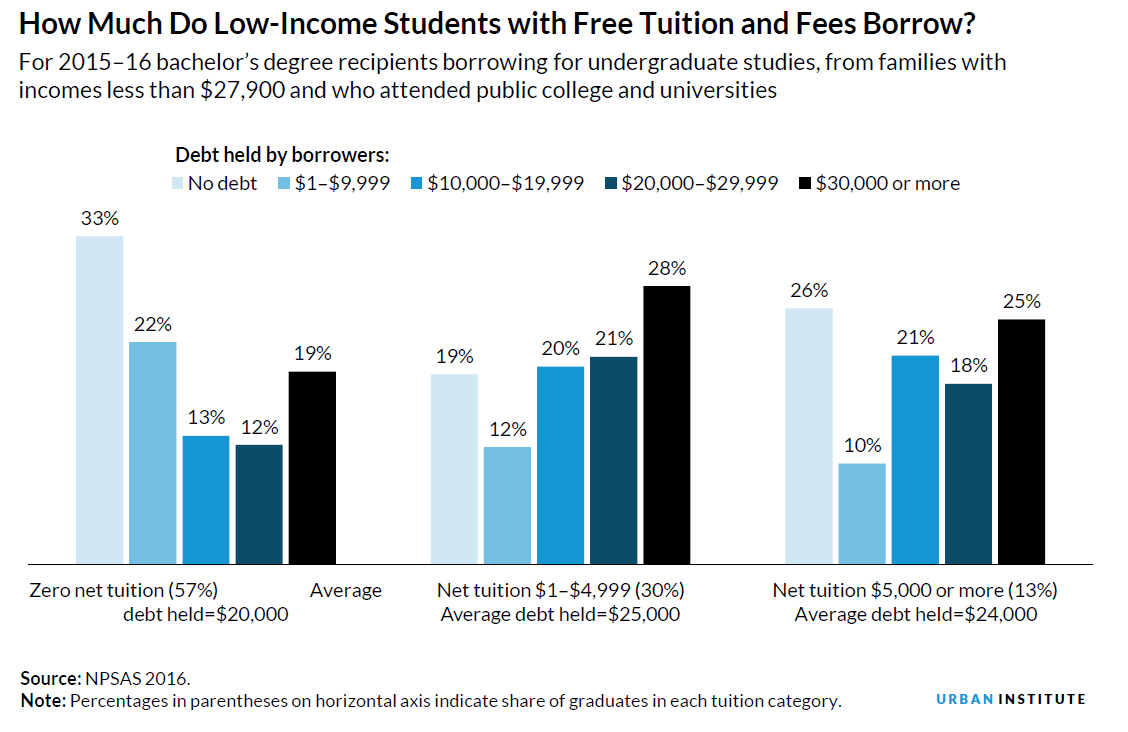

Students from low-income families are more likely than others to have free tuition. In 2015–16, the share of students whose tuition was covered by grant aid ranged from 57 percent of those from families with incomes below $27,900 to 8 percent of those from families with incomes of $113,500 or more.

Low-income students with zero net tuition borrow less than others. But among 2015–16 low-income public college bachelor’s degree recipients with this benefit, two-thirds graduated with debt, and almost 20 percent borrowed $30,000 or more.

Data for students from other income groups show similar patterns. In all income groups, students paying zero net tuition and fees are somewhat less likely to borrow and less likely to accumulate high levels of debt than those paying tuition, but most still borrow and a significant share borrow large amounts.

Older, independent students—including those whose tuition and fees are completely covered by grant aid—are more likely to borrow and to borrow at high levels than dependent students from any income group; differences by level of tuition paid are small.

Three-quarters of 2015–16 independent public college bachelor’s degree recipients had debt, about the same share as among those paying tuition. Independent students have higher federal loan limits than most dependent students. They are also more likely to be fully responsible for their own living expenses and frequently those of their families.

Lower tuition prices reduce financial pressures on students and are likely to diminish debt levels for some students. But zero tuition does not eliminate the financial barriers many students face.

Student loans aren’t going away

At all income levels and for all types of programs, students borrow to cover their living expenses while they are in college. Advocates for free tuition should recognize that if their goal is to ensure that most undergraduates graduate debt-free (a goal not everyone shares), they will need to develop a program more ambitious than free tuition.

In particular, free-tuition programs that just fill in the gaps between tuition prices and Pell grants do not increase the funding most low-income students receive and would not decrease their borrowing.

Larger shares of students from more affluent households would be affected by a free-tuition policy because few of them now enjoy this circumstance. Ensuring that low- and moderate-income students receive additional funding—beyond tuition prices—should be central to policies designed to reduce the financial barriers to college education.

And regardless of policies that lower tuition prices, or even reduce them to zero, many students will continue to rely on loans. Strengthening existing federal student loan programs should remain a high priority.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.