<p>Photo via Shutterstock.</p>

One of the most pronounced shifts in the housing market since the financial crisis has been the evolution of the single-family rental (SFR) market. Today, single-family rentals (one-unit, attached and detached) account for 35 percent of the country’s 44 million rental units, compared with 31 percent in 2006. More than half of renters live in structures with less than four units.

The Urban Institute’s Housing Finance Policy Center recently hosted a panel discussion with three single-family rental experts: Douglas Bendt from Investability, Sandeep Bordia from Amherst Capital Management, and Calvin Schnure from the National Association of Real Estate Investment Trusts (NAREIT). Their conversation illuminated five important facts everyone should know about this growing market:

1. Single-family rental is the fastest-growing segment of the housing market.

Growth in SFRs has outpaced growth of single-family owner and all multifamily housing in recent years. Data from NAREIT shows the SFR sector has seen growth every year since the crisis and has lingered around a 30 percent growth rate for the past three years, compared with less than a 15 percent growth rate for the multifamily market during that same period. The single-family owner market began to grow again in 2016, after declining for seven years.

The number of households in the US is continuously increasing, but with growth in owner-occupied units stagnating, almost all the housing demand in recent years has been filled by rental units.

2. Changing demographics and housing market conditions will continue to fuel the rental growth.

None of the three panelists think the growth in rental households will slow in the coming years. This segment’s growth is fueled by changing demographics and evolving household preferences.

Young people are waiting longer to get married and have children, which can make renting more economical. And while the age distribution of the US population suggests most millennials are reaching the age of household formation and demand for single-family homes, much of this demand is likely to be channeled into the rental market.

Housing market conditions also play a role in increasing the share of households that rent. Tight mortgage credit and ballooning student loan debt are barriers to homeownership that can push households into the rental market. The result of these constraints on homeownership is that we will see continued growth in rental demand for the foreseeable future.

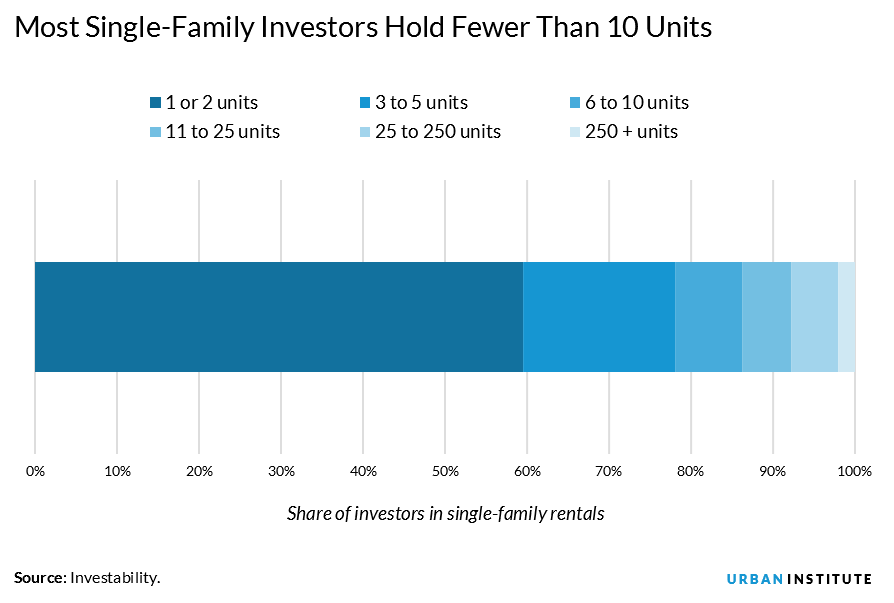

3. Institutional investors are tiny players in the single-family rental market.

Of the over 15 million SFR units, just over 200,000 are owned by institutional investors, or about 2 percent of the market. Compare that with the multifamily market, where institutional investors own more than 55 percent of units. Investability estimates that 45 percent of SFRs are owned by investors who own just one unit and that 87 percent of investors own 10 or fewer units.

The composition of the markets also varies significantly. In the multifamily space, the 50 largest investors each hold more than 23,000 units, averaging about 60,000 units each. In the single-family market, only three or four entities hold more than 20,000 units.

The largest single-family investors recently have been buying fewer homes than in prior years. Bordia shared data from Amherst Capital Management showing that the three largest holders of single-family properties, Blackstone, American Homes 4 Rent, and Colony Starwood, have all slowed their purchases in the past three years, while midsized investors are gaining ground.

4. The geographic focus of institutional investing in SFRs has shifted.

After the financial crisis, institutions invested heavily in single-family homes as the abundance of short sales and foreclosures made cheap properties readily available. In cities that saw the biggest booms (and subsequent busts), institutional investors accounted for a large share of home purchases. For example, in Phoenix between 2007 and 2010, the number of owner-occupied single-family homes fell by 30,000; institutional investors bought 20,000 of those homes and converted them to rentals.

As the housing market has recovered, the pattern of institutional investing in SFRs has evolved as well, according to data from Amherst Capital Management and Investability. Cities in the West and in Florida, which were huge hubs for institutional investment in the early postcrisis years, account for a smaller share of homes bought by institutional investors in 2016.

Meanwhile, cities in the South, such as Charlotte, Dallas, Houston, and Memphis, saw rising shares of institutional investment in 2016. But even where institutional investment is high, it’s still a tiny part of the total market.

5. Future growth of institutional investors in SFRs is still up in the air.

The years of easy growth are behind the single-family rental industry. The financial crisis created the perfect storm for institutional investors to quickly gain ground. But the experts see several obstacles to continued high growth.

Bordia explained that, with a plethora of cheap homes no longer available, future growth will depend on successful management and increased operational efficiencies.

According to Bendt, growth will also be a function of how well investors can expand into other markets, primarily smaller, low-cost cities where investors may move into different property types. Schnure pointed out that the cost of capital and availability of financing from Fannie Mae and Freddie Mac will affect industry expansion in the coming years. He also suggested potential for more growth in this sector as smaller players consolidate.

While the single-family rental market may continue to grow rapidly in the coming years, it remains unclear whether institutional investors will make an increasingly large mark on this space or continue as small, niche players.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.