<p>Illustration by MHJ/Getty Images.</p>

In 2010, the Federal Housing Administration (FHA) introduced a program, later named the Distressed Asset Stabilization Program (DASP), which sells pools of severely delinquent loans to investors to reduce stress on its balance sheet and help borrowers otherwise headed into foreclosure. (Edward Golding formerly oversaw DASP as head of FHA.)

FHA has exhausted its options to avoid foreclosure on these loans, so in sending them to investors, who have still more options, FHA gives some of these borrowers another chance. In DASP’s first six years, 2010 to 2016, FHA sold 111,000 loans ($19 billion in unpaid principal balance) through the program, about 20 percent of FHA claims to lenders over the period.

Earlier this month, the Government Accountability Office published an evaluation of the program. It offered several helpful recommendations, particularly on how FHA can improve the program’s quality controls by

- using loan performance data criteria to time DASP sales to maximize their effectiveness,

- more rigorously monitoring investors’ compliance with FHA’s loan modification requirements, and

- ensuring servicers have exhausted all options available on FHA-insured loans before these loans are sold through the program.

How effective is DASP?

As to DASP’s overall effectiveness, GAO’s conclusions are unfortunately less helpful. GAO concludes that “in aggregate, sold defaulted loans were more likely to experience foreclosure than comparable unsold defaulted loans,” noting the probability of foreclosure 24 months after the loan servicing was transferred to the investor was 43 percent for sold loans through the program, versus 36 percent for unsold loans.

Though this figure appears bleak, and is indeed the subject of criticism in the report, it indicates the program’s success, not its weakness.

The figure compares the outcomes of delinquent borrowers who FHA could no longer help, and were thus put into DASP, with borrowers FHA could still help avoid foreclosure. Put differently, it shows the program changed the probability of foreclosure in that first group from close to 100 percent to 43 percent, only 7 percent higher than the group of borrowers FHA was still in a position to help on its own.

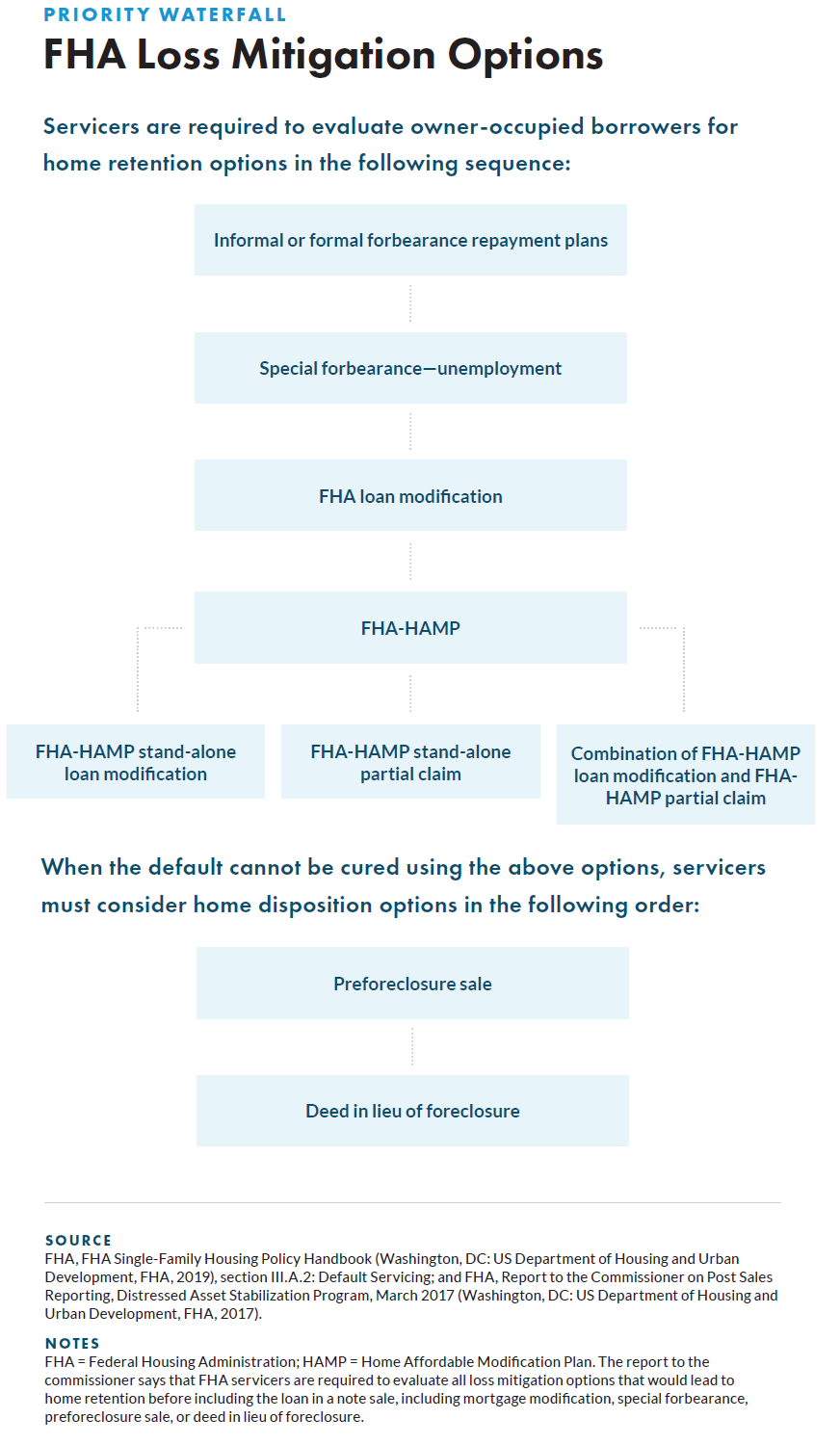

GAO matched the characteristics of the loans sold through DASP from 2013 to 2016 to those not sold, matching length of delinquency, occupancy status, location, servicer, estimated current loan-to-value ratio, and loan origination year. Most unsold loans in the report had not yet cycled through the FHA loss mitigation waterfall , however, leaving FHA with options to help them avoid foreclosure—unlike those sold through DASP, for which FHA had exhausted its loss mitigation and modification toolkit.

The graphic below shows the steps a loan must pass through before it can be sold through DASP. Selling loans that have not completed these steps would indeed call into question the effectiveness of the program, but GAO has indicated that only a tiny fraction of the loans, 2.67 percent, were ineligible for DASP at the time of sale, and no doubt some of these loans were ineligible for other reasons.

When understood this way, one would expect the loans sold through DASP to perform better than those that were not, because in only the former the loan owner still has tools to help these deeply distressed borrowers avoid foreclosure.

The investors who buy loans through the program can reduce a borrower’s payment by extending the loan term to 40 years or by cutting the interest rate to below a market rate of interest. They can forgive the principal on the loans, forbear more than 30 percent of the loan value, or offer more generous terms for deeds in lieu of foreclosure or short sales. None of these options is available to FHA given their statutory authority. Again, borrowers who participate in DASP are basically out of options with FHA.

That is not to say the program could not have been improved upon during GAO’s evaluation period. More needed to be done to ensure borrowers whose loans were sold through this program got the best shot possible and any foreclosures had minimal impact on the community.

The FHA made several changes along these lines in mid-2016, including a first look for nonprofits, a requirement that principal reduction be offered as the first modification option to qualified borrowers, stronger investor disclosures on borrower outcomes, and a requirement that investors not “walk away” from the most challenging loans, a strategy that leaves properties abandoned.

Because there has been only one auction in 2016 after these changes were implemented, the impact of these changes has not been extensively studied. GAO’s report shows the deals in that year performed better than those in previous years, with loans foreclosing at a lower rate over 24 months than those unsold. This is encouraging, but the study period is too brief to adequately assess the difference between the sales before and after the changes went into effect.

While these changes will improve the program, additional steps can and should be taken. As in a great many other areas, FHA could use better information systems and monitoring capability and more personnel and funding to manage the program. And in the meantime, FHA should be releasing much more loan-level data, including data on DASP, so that independent analysts can help them evaluate their programs. Indeed, periodic public reporting of outcomes would be valuable. A lesson from the Making Home Affordable program was that more public reporting provides a very useful accountability tool.

The bottom line, though, is that the GAO report does not show that DASP is fatally flawed. DASP is a powerful tool that has helped thousands of families avoid foreclosure and has reduced stress on the FHA’s insurance fund, making it easier for FHA to keep premiums low to ensure broad access to homeownership.

Though it has had its faults, the program has been improved over the years and can be improved more as we gather new evidence and insights, making it still more useful in the downturns to come.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.