The Federal Home Loan Banks (FHLBanks) are government-sponsored enterprises (GSEs) that provide a reliable source of liquidity to financial institutions engaged in housing finance and community development. They were founded in 1932 to help revive the housing market after the Great Depression, and over the past 93 years, Congress has expanded FHLBank membership eligibility beyond savings institutions and insurance companies to commercial banks, credit unions, and community development financial institutions. Despite their long history and broad scope, the FHLBanks’ broader value to the financial system has received little evaluation.

In our new study, we find that the FHLBanks not only supply liquidity to members in need but also substantially enhance overall financial stability. Focusing on commercial and savings bank members—which together represented more than 80 percent of members between 2002 and 2024—we estimate that the FHLBank System generates $13.2 to $21.4 billion in annual economic value by reducing the risk of systemic crises. These benefits are two to three times larger than the Congressional Budget Office’s estimate of the benefit that the FHLBanks receive from their GSE status.

How FHLBanks provide a reliable source of liquidity during stressful times

The 11 FHLBanks provide funding through advances, or fully collateralized loans, to their member institutions. Because members are also cooperative owners, this funding channel is designed to serve their collective stability rather than short-term profit.

FHLBank members tend to rely more heavily on advances when they face liquidity constraints. This is visually clear and is confirmed by rigorous regression analyses. Advances surged during the 2007–08 financial crisis, again in 2020 at the start of the COVID-19 pandemic, and most sharply in 2023 during the regional banking turmoil following the failure of Silicon Valley Bank.

When depositors fled smaller regional banks for larger institutions, many smaller banks turned to their FHLBank for liquidity. That quick access to funding helped prevent further stress.

Source: Office of Finance, Federal Home Loan Banks Combined Financial Report for the Year Ended December 31, 2024 (Reston, VA: Federal Home Loan Banks, Office of Finance, 2025).

Notes: Q = quarter. Gray bars indicate the financial crisis, the outbreak of the COVID-19 pandemic, and the 2023 regional bank crisis. Savings banks include savings banks, savings associates, and savings and loan associations. Total outstanding advances of all financial institutions show similar time trends and can be found at “Government-Sponsored Enterprises; FHLB Advances; Asset, Level,” Federal Reserve Bank of St. Louis, last updated June 12, 2025, https://fred.stlouisfed.org/series/BOGZ1FL403069330Q.

The impact of FHLBank advance liquidity on bank risk taking has been debated. On one hand, access to additional liquidity should allow banks to reduce funding risk and, in turn, default risk. On the other hand, access to low-cost financing could encourage banks to increase risk taking as their financial situations deteriorate.

Our analysis shows that the FHLBanks’ stabilizing effects are stronger; FHLBank advances substantially reducing banks’ default risk.

We look at z-scores, a widely used measure of bank solvency risk, which compare a bank's capitalization and return levels with its risk (volatility of returns). A 1 percent increase in advances is associated with a significant 19-point increase in the z-score, indicating that FHLBank advances help banks reduce risk and become financially healthier.

Similarly, we show that FHLBank membership decreases the likelihood of bank failure by about 10 percent. The effect is strongest among higher-risk banks (those with low z-scores), which are more likely to draw on advances during stress. A few institutions still fail during crisis events, but most banks survive thanks, in part, to their access to FHLBank liquidity at a critical time.

These results are consistent with a recent Federal Reserve Bank of New York study. Using high-frequency interbank payment data to trace deposit flow, the study showed that 22 banks experienced bank runs during March 2023, and 2 of them failed. The banks that did not fail borrowed new funds and raised deposit rates, they did not selling liquid assets. Virtually all the banks that survived this run relied on the borrowing from the FHLBank System as a source of funding.

FHLBanks strengthen the whole financial system

The FHLBanks’ impact goes beyond helping individual institutions. We used a measure called the Conditional Tail Financial Risk Indicator (CATFIN) index to track systemic risk across the entire banking sector. Higher value indicates greater risks.

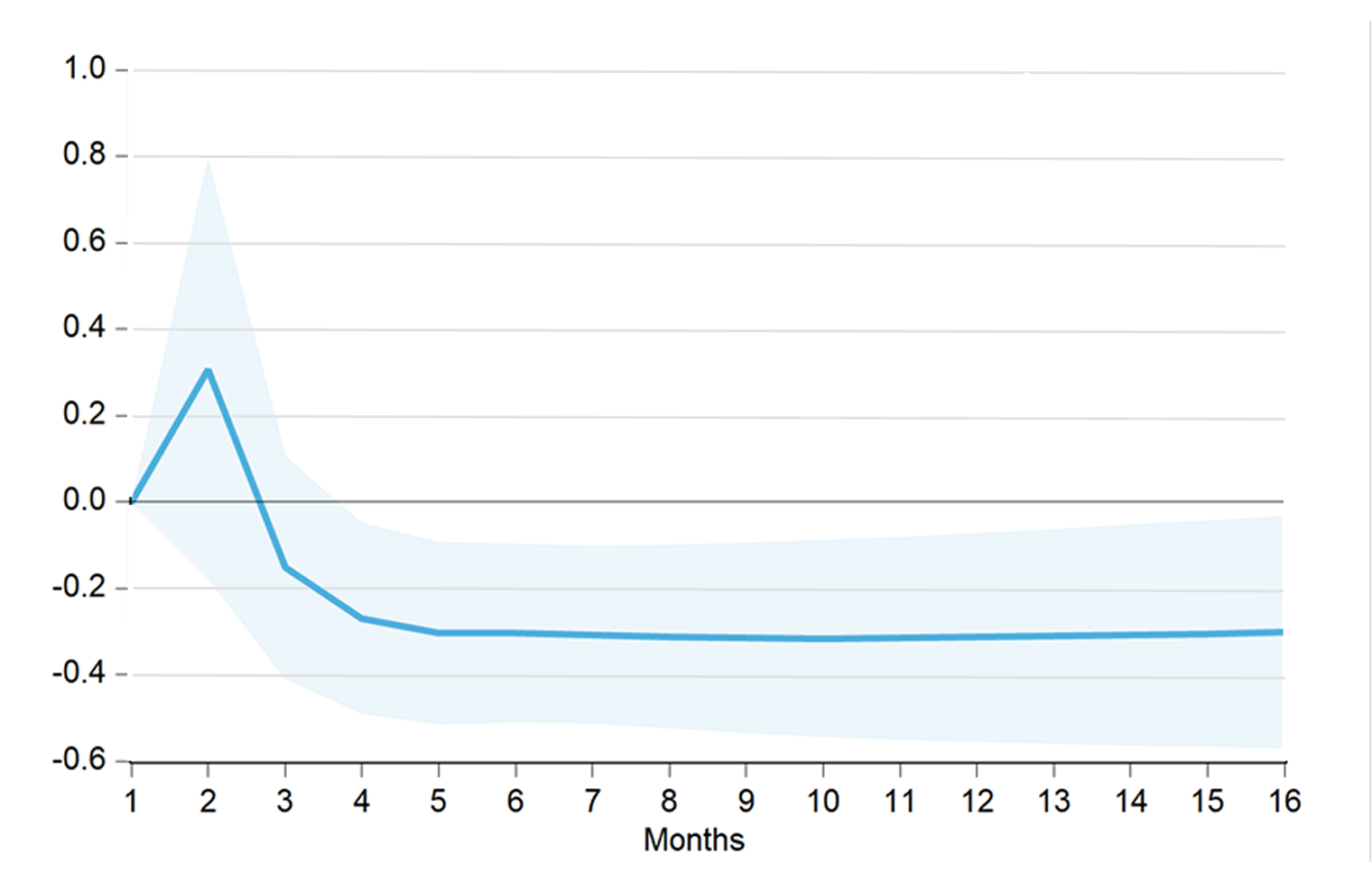

Using the impulse response function, we examine how the CATFIN index responds to a positive aggregate FHLBank advance shock, holding other factors constant. We find that the response in the first two months is positive but insignificant, as the stress in the system is the catalyst for banks increasing advance usage. The coefficient is near zero in month three but turns significantly negative in month four and stays negative for the next 12 months, indicating that a positive advance shock permanently reduces the CATFIN index, thus lowering systemic instability.

FHLBank Advances Reduce Systemic Financial Risk

Impulse response to a 1 percent increase in FHLBank advances on the CATFIN index

Source: See the CATFIN data at “Data and Working Papers,” Turan G. Bali, accessed September 5, 2025, https://sites.google.com/a/georgetown.edu/turan-bali/data-working-papers. The FHLBank advance data come from the Federal Reserve Bank of St. Louis FRED (Federal Reserve Economic Data): https://fred.stlouisfed.org/.

Notes: CATFIN = Conditional Tail Financial Risk Indicator; ppt = percentage point. Shaded areas are 95 percent confidence intervals.

Implications for financial stability

The Federal Housing Finance Agency’s 2023 report on the FHLBank System generated significant discussion about the FHLBanks’ value proposition. Our research suggests that the FHLBanks continue to play a vital role in stabilizing the financial system. By providing liquidity when markets tighten, advances help individual institutions avoid default, lower overall bank failure rates, and reduce aggregate-level systemic risk.

Overall, the $13.2 to $21.4 billion in annual economic benefits generated by the FHLBank System in promoting financial stability far exceed the value received from its GSE status, underscoring the FHLBanks’ enduring importance to the US financial architecture.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.